[edit] Post veers at little at the end, may require a couple reads…

[edit2] Attn: Subscribers, material dovetails with market analysis in #318

[edit3] Charts are quite large; click for full size

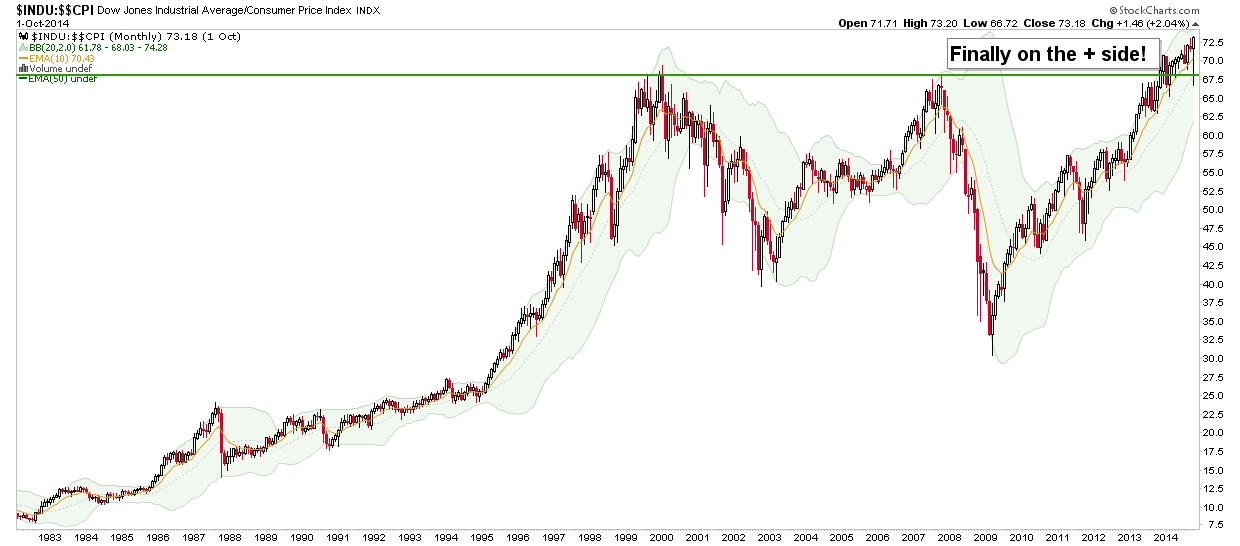

MarketWatch announces that the US stock market is back to the ‘real’ highs of the last secular bull market, prior to the dot.com/tech bubble blow out. Here is the Dow adjusted for CPI, finally paying back investors after a 14 year debit in ‘real’ terms.

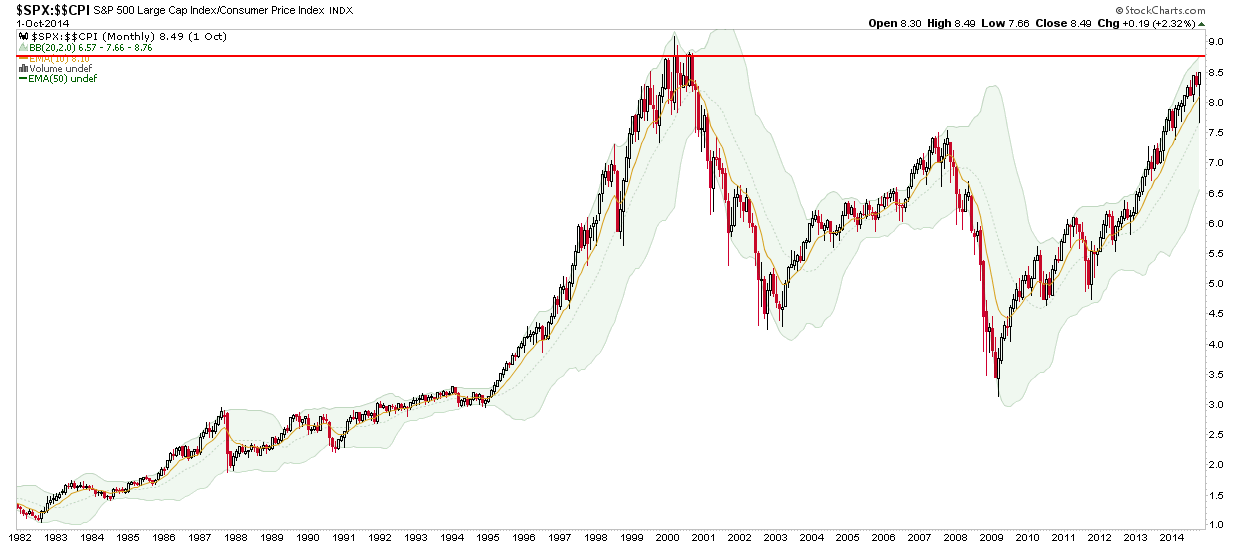

SPX-CPI is almost to break even.

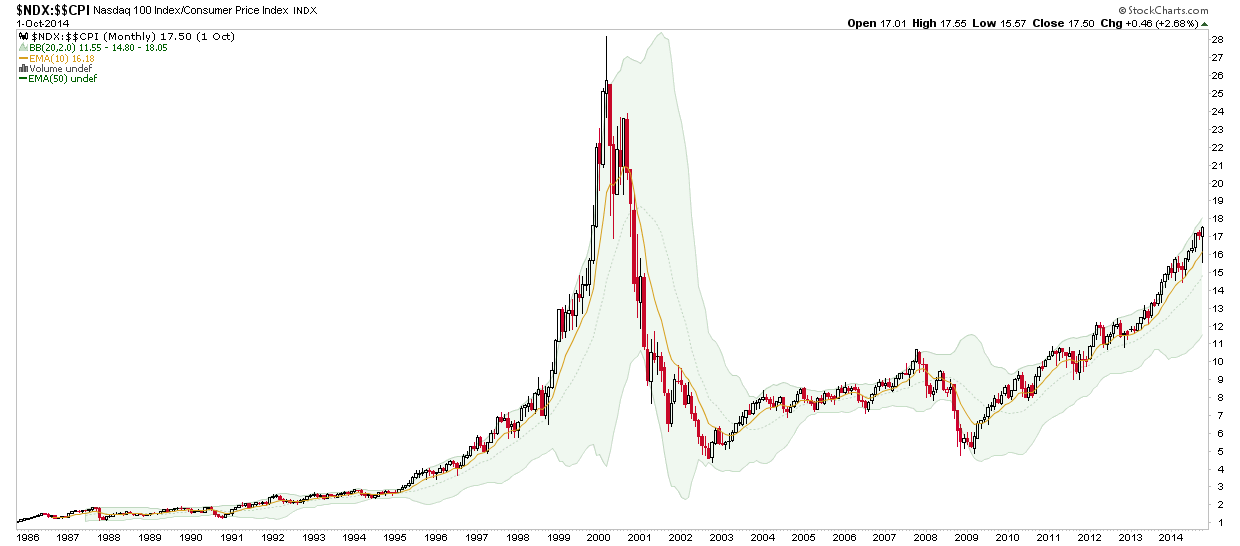

NDX has a way to go…

As adjusted for the official measure of inflation’s effects, the stock market cannot be stated to be in a secular bull market yet. Further, as measured in what I would call a more realistic ‘real’ market, Dow (the best performing of the above over the last 14 years) vs. Gold is merely in a counter bear market rebound, as strange as that seems.

Of course the chart is the chart and despite what we think may be ‘real’, the rebound in Dow vs. Gold has not even made a 38% retrace of its entire bear market yet. It’s a ratio and maybe it need not act like a stock or a nominal market. But then again, may it will. Maybe it is destined to make such a retrace, either by a stock market blow off or a final plunge in the ‘real’ money anchor.

So gold bugs might want to at least consider that the excellent contrary play setting up may get more contrary still and even more excellent before current trends reverse.

As noted above, it’s a ratio and need not pull a 38% retrace, but at the very least people really should tune out the easy analysis talking about how Indian buying and whatever other cartoons are promoted will be bullish for gold. We are in a cyclical phase where gold is risk ‘OFF’ and it appears that only a counter cyclical risk ‘OFF’ phase is going to put gold on its next bull market.

However, the greater point of this post is that on the big picture, big deal, stocks are finally at parity with CPI after 14 years. They remain in a bear market vs. gold because gold’s ‘value’ is as insurance against various threats, not just inflation.

If our thesis that the current stock bull is simply the ‘successful’ result of inflation, its ratio to gold perhaps reflects how much future liability has been painted into the picture by modern policy making.

Subscribe to NFTRH Premium for your 25-35 page weekly report, interim updates (including Key ETF charts) and NFTRH+ chart and trade ideas or the free eLetter for an introduction to our work. Or simply keep up to date with plenty of public content at NFTRH.com and Biiwii.com.