Users: Hunk of Junk: Reporate7.1.png

Reporate7.1.png

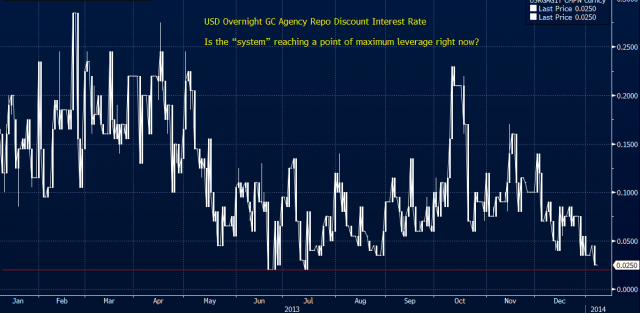

The US overnight Repo rate (General Collateral) has declined to 2.5 bp – very close to its lowest level during the last 12 months and since QE 3 was announced in September 2013.

The implication, once again, is signs of emerging stress in shadow banking, namely an emerging shortage of collateral in the repo market

The contention is twofold:

i) An unspoken reason for tapering was to ease collateral shortages in repos

ii) Shadow banking conduits, like repos, have been a factor in propelling the S&P to all-time highs, i.e. via the collateralisation of QE-created excess deposits

The current situation raises a couple of questions:

i) Will $10bn of initial tapering be sufficient to avert problems in the systemically critical repo market? Interesting that on 20 December 2013 the FRBNY increased the maximum allotment of REVERSE REPOS from $1bn per counterparty per day to $3bn per counterparty per day !!!

ii) Is the “system” reaching a point of maximum leverage right now? And...making a big mental lea

he has stated to others: "It’ll be clear in the Minutes on Wednesday.” 1/7/14