It is certainly a more pleasant feeling right now, pre-market, examining a sea of very modestly red quotes and preparing for the day instead of bracing myself for one of the biggest rallies in history. Believe it or not, Iran isn’t the only thing affecting the markets, and there is still other data to examine. Two important items came out this morning.

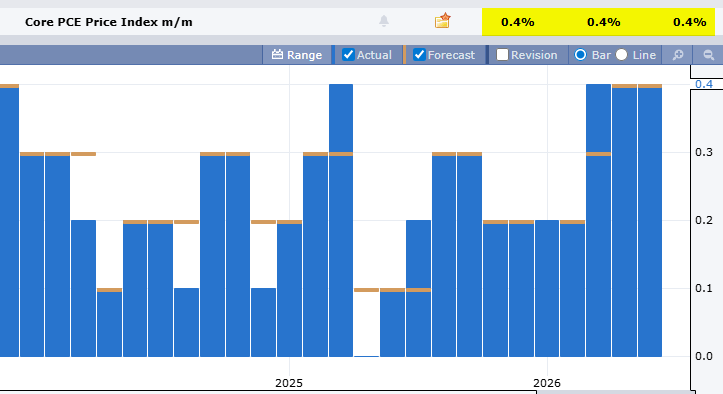

The first is the Core PCE, which, as we are told, is the favorite inflation indicator of the Fed. It continues to clock in at 0.4% per month. Using my array of mathematical calculations, that comes in at 4.8% annually, which seems on the high side.

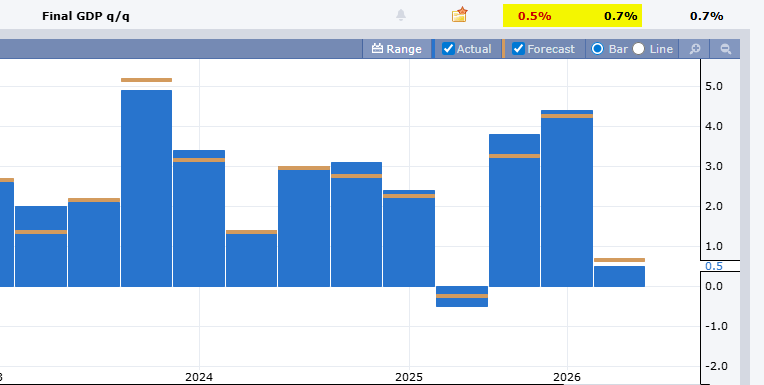

Our economy, the “hottest on Earth” I believe we were assured, produced its final GDP at a whisper-thin 0.5% for the quarter. Again, using the power of math, we can conclude an annualized rate of 2%.

So, let’s see, a stagnant economy yet with inflation. Someone should come up with a portmanteau as a shorthand way to describe that situation!

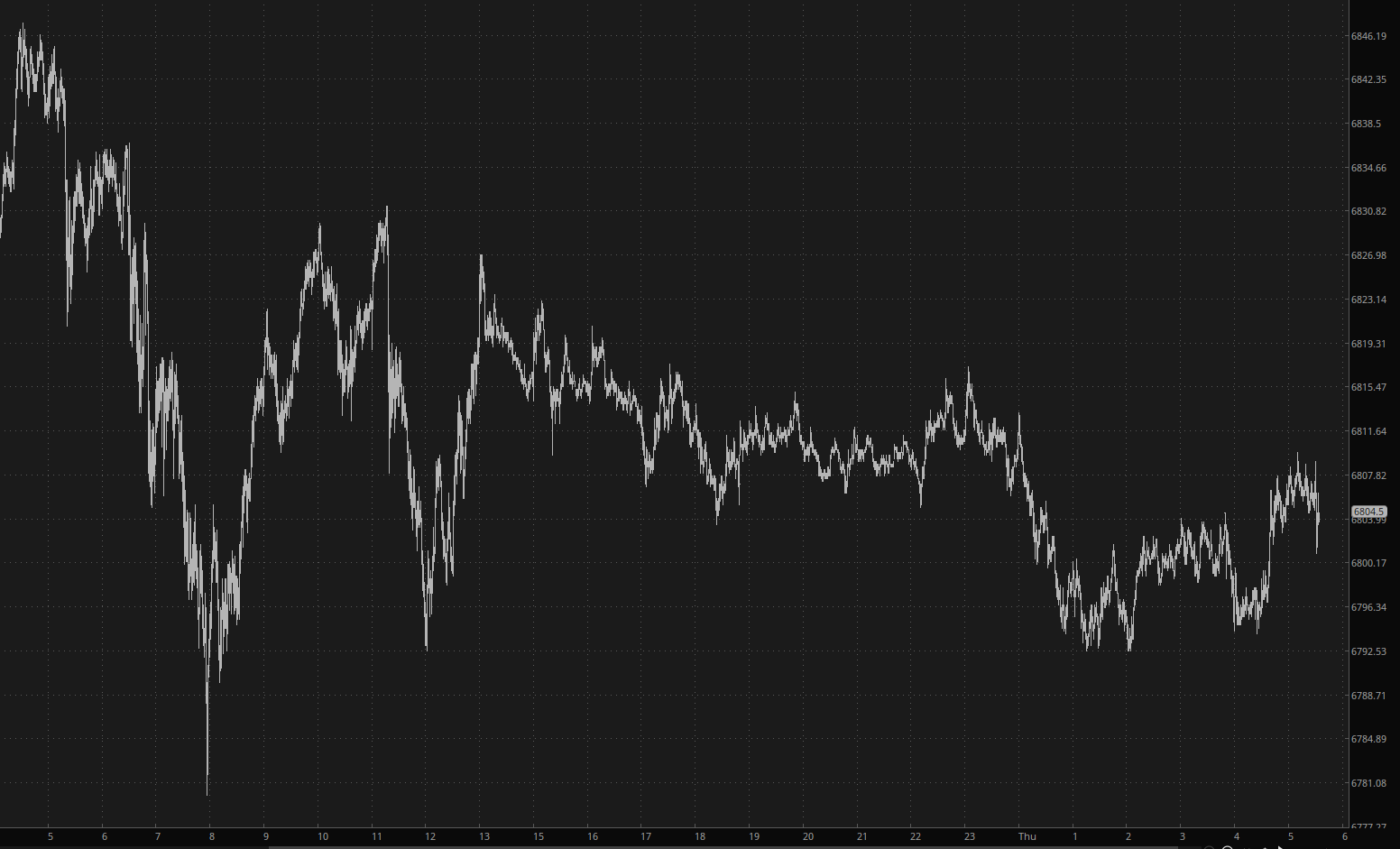

The equity futures have been ever-so-slowly burning off a little of the huge gains from yesterday, as the world continues to digest what is, let’s face it, Iran bringing Trump to heel, in spite of all the propaganda spewing forth to convince you otherwise. The notion that this thing is “over” is, I believe, wrongheaded.

The overwhelming majority of the ceasefire gains are still intact, with equity futures down pre-market only fractionally.

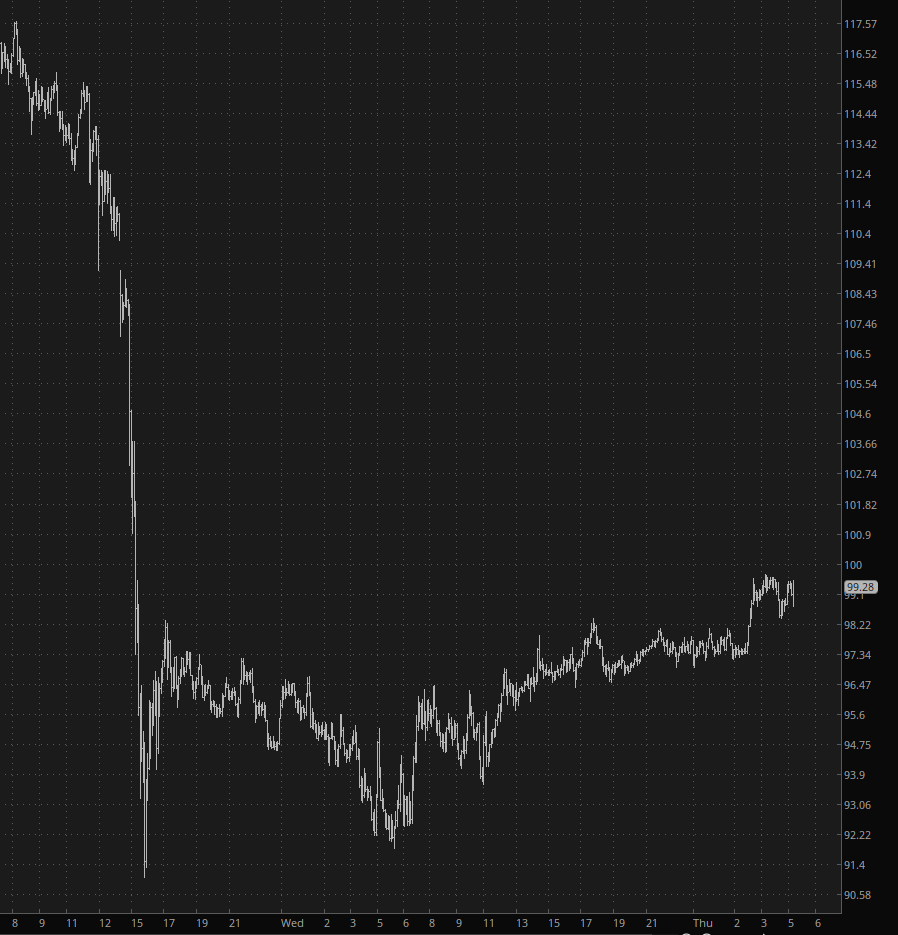

Interestingly, crude oil has steadied itself and is up over 10% from its nadir. That’s a fairly impressive move in such a short time, and we’re still just pennies away from the psychologically important triple-digit price level.

Finally, I continue to monitor Bitcoin very closely. At yesterday’s very strong opening bell, I committed the entirety of a portfolio to BITI (inverse bitcoin) which is sporting a pipsqueak profit so far. Obviously, I’m hoping for better things.

As I enter this new trading day, I am more heavily committed on my equity short accounts (90%) although still exceptionally cautious in my options account (26%).