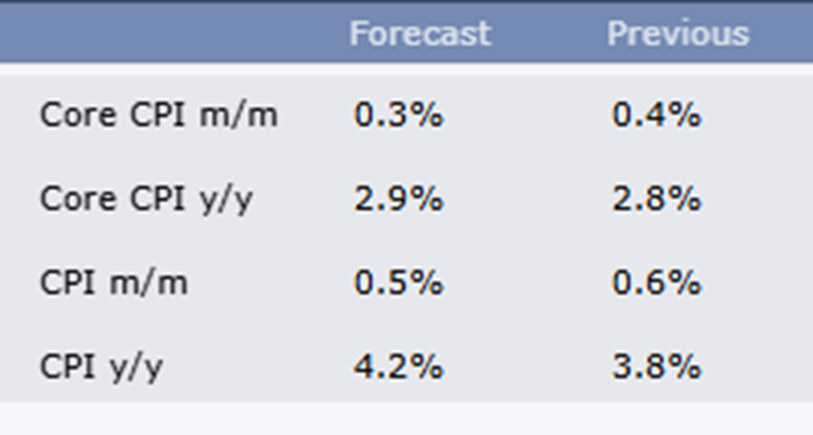

This morning, the United States government released the inflation numbers from a department controlled by an exceptionally unpopular administration during a time in which high prices are the primary concern. I’m sure you are eager to see just how the predicted numbers (right column) compared to the officially computed, straight-from-the-paid-staff numbers.

Drum roll, please, maestro!

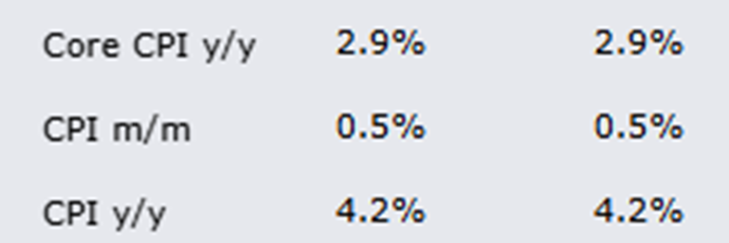

W00t! They nailed it! Way to go, fellas! Inflation is well and truly conquered.

(more…)