Slope of Hope Blog Posts

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

Dressed for Duress

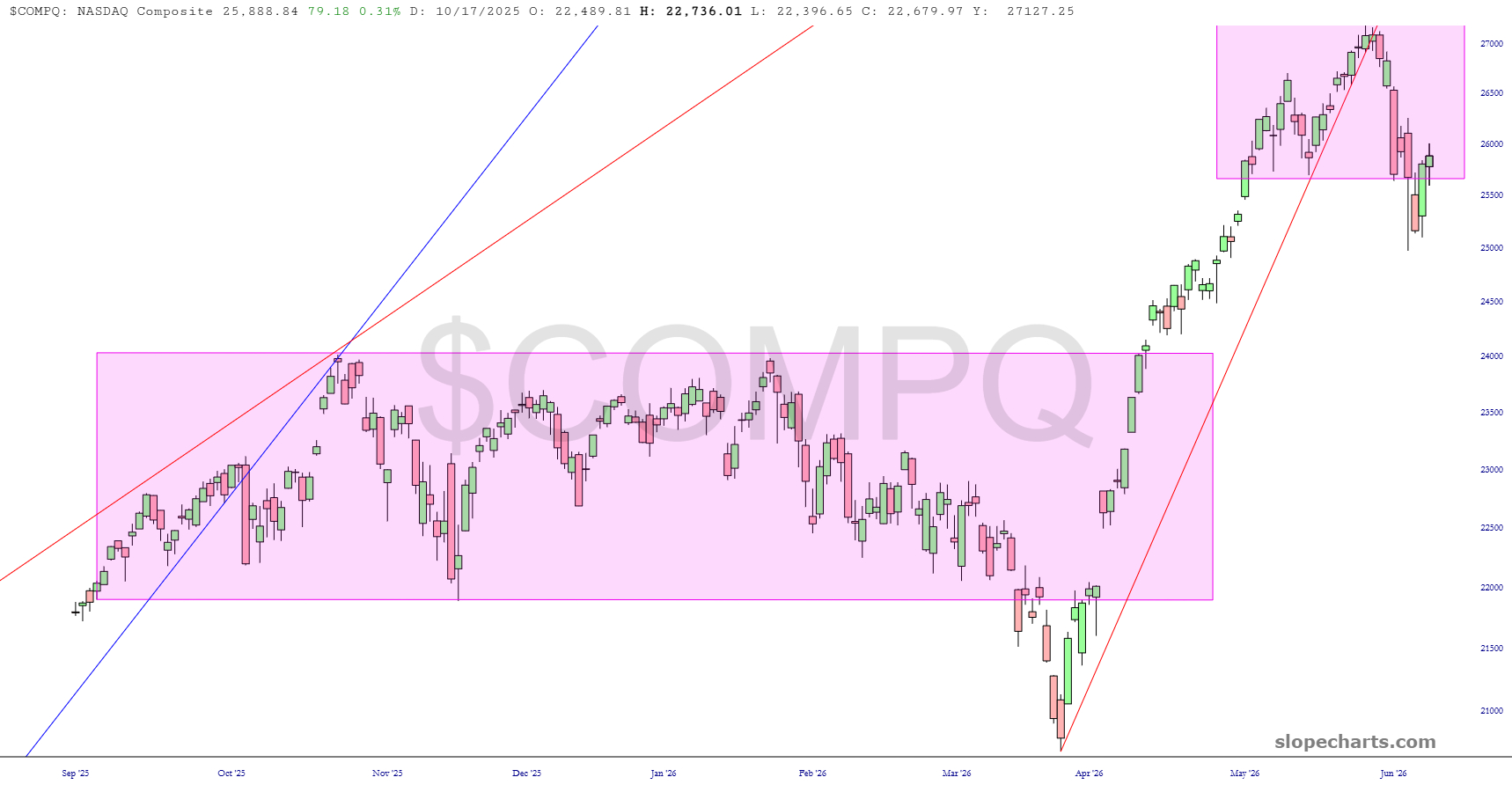

Not to put too fine a point on it, but the index charts below are just BEGGING for a smackdown. Getting past the SPCX IPO clears the field. The main wild card now is the Iran war. The best news for the bears would be for the damned thing to get settled. In any case, take a good, hard look at these:

Another Inflection Point Here

In my post on Wednesday I was looking at the H&S patterns that had broken down on SPX, QQQ and DIA and saying that, for a variety of reasons I explained then, I didn’t think any of those H&S patterns were likely to reach their targets, and would likely instead fail into retests of their all time highs. Since then we have seen the start of rally I expected and equity indices have reached another inflection point where they can either break up towards retests of the all time highs, or fail down into those H&S targets.

On DIA the H&S failed this morning on the break back over the H&S right shoulder, and that now has a target at a retest of the all time high, but the big dogs here are SPX and QQQ, so I’ll mainly be looking at those today.

(more…)Golden Triangle

Precious metals rallied strong yesterday based on the news that we beat Iran for the 39th time in the past couple of months. We are very close to a price gap, which, given the huge right triangle top, could be a good entry point for new shorts.

Itty Bitty Bit

I’ll just say again, the bearish-on-Bitcoin fund BITI is looking like a potentially amazing inverted head and shoulders bullish bottom.