Inflation is everywhere!

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

Inflation is everywhere!

Yesterday’s CPI was somewhat of a yawner (inflation coming in a little hotter than expected), so I didn’t expect much from the PPI. Well……….

That’s right: annualized Core PPI is at 12% and month-over-month, annualized, comes in at 16.8%. Hey, didn’t the administration say inflation had been conquered? I guess not.

(more…)This morning’s pre-market announcement of CPI data was being heralded as perhaps the most exciting event of the week. Well, maybe not. The CPI came out, and inflation is running much hotter than expected.

There is currently much hype in the media about a hawkish Fed because the media wrongheadedly anticipates rate hikes due to the “inflation” being caused by rising oil prices (directly and indirectly). Furthermore, CME traders, often little more than a wind sock indicating current sentiment as opposed to accurate forward forecasters, have completely backed off their previous view of rate cuts, and now increasingly favor a rate hike this year.

Perfect!

(more…)Sometimes I feel as though I write the same public article over and over. But that is because the changes since 2020, and especially 2022, have been profound from a standpoint of market management. In NFTRH we define and employ that management.

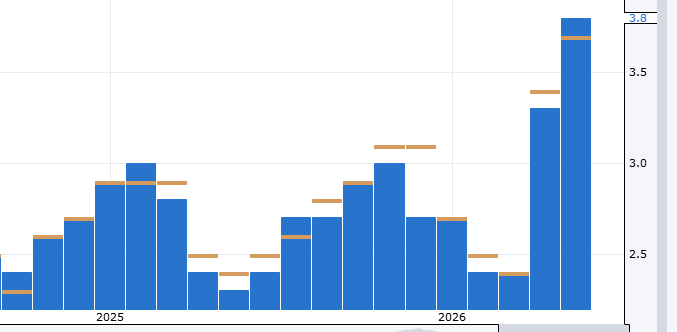

In line with our long-standing view that the now inflationary macro would undergo its first countertrend, an interim disinflationary trend, Treasury bonds from the shortest durations on up to the longer durations are on plan.

(more…)