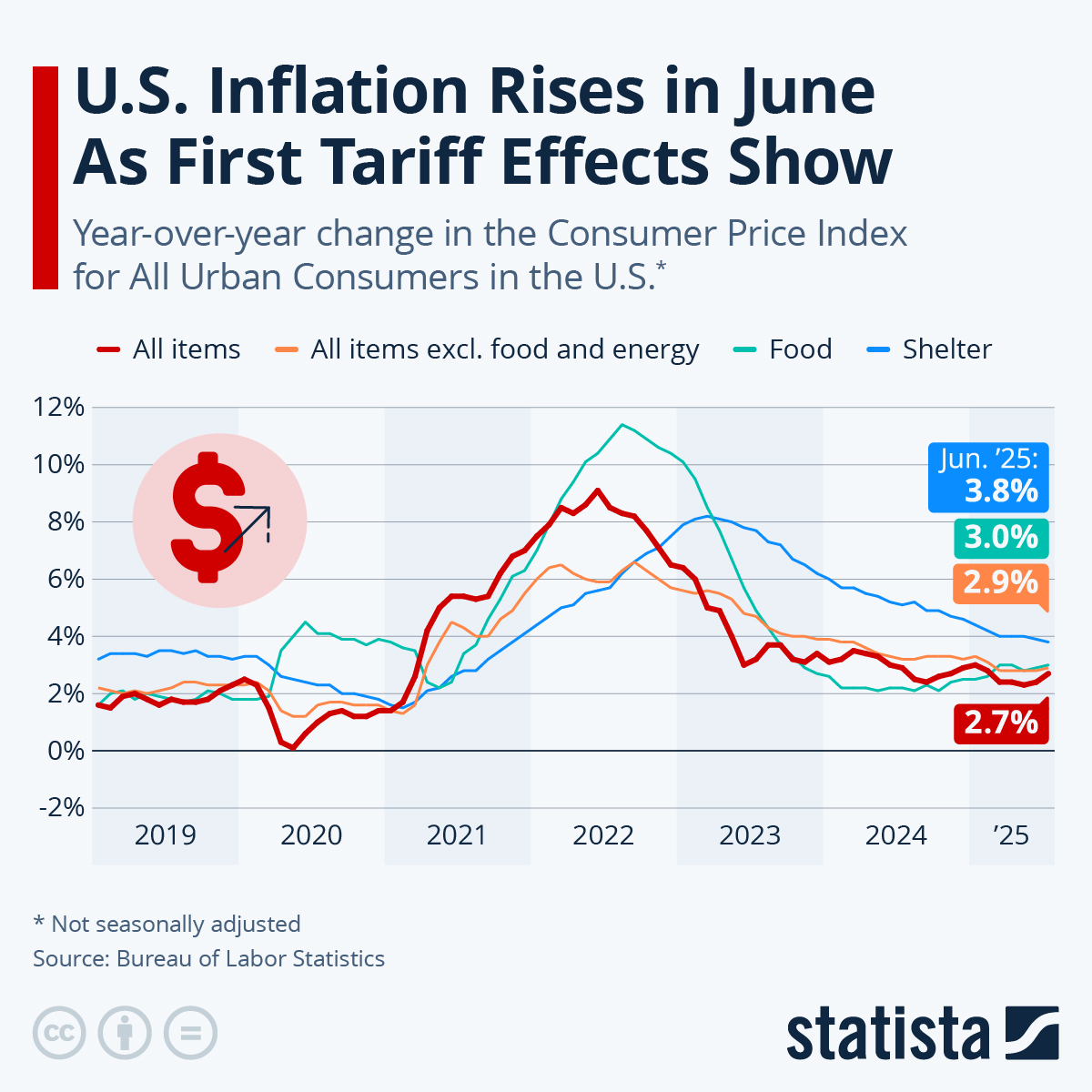

Good morning, everyone. The CPI is out, and, just like the PPI, it came in hotter than expected. I still think it’s a total joke that this “hot” CPI is 3.7% annually. Are you KIDDING me? I sincerely think it’s 3.7 a MONTH. Again, I’m serious. I spending a couple hundred thousand bucks on stuff a year. I know what things cost. And I’m a cheap sumbitch, so I’m sensitive to it. INFLATION ISN’T 3.7%!!!!!!! Good Lord!

In any case, the equities have softened up, at least for the moment.