BlackRock’s coziness with China isn’t going unnoticed amid its increased push in favor of (environmental, social, and corporate governance (ESG) issues. China isn’t exactly known for supporting ESG issues, and BlackRock is being criticized as favoring Chinese companies that lack regulatory oversight over their better regulated U.S. peers. Meanwhile, U.S. lawmakers are criticizing the firm’s involvement in coronavirus-relief measures for its focus on China.

(more…)Slope of Hope Blog Posts

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

CBDCs May Undermine USD Hegemony

The past week saw Goldman Sachs and JPMorgan, two traditional finance investment banks, discuss cryptos, their identities as an asset class, and CBDC’s potential threat to the U.S. dollar. Dr. Marc J.J. Fleury, CEO of fintech firm Two Prime, discusses the following topics this week, with full commentary below.

- GS: Crypto is not a real asset —In a recent investor call, Goldman Sachs spoke about how bitcoin and other coins were unsuitable for investment, with BTC’s run likened to that of the Tulip mania back in the 1600s. When it seems so obvious that crypto is here to stay, what do they still not understand?

- JPM: CBDCs may undermine the hegemony of the USD — In a report last week, JPMorgan asserted that “there is no country with more to lose from the disruptive potential of digital currency than the United States.” How realistic is it for a digital currency like bitcoin to become the world’s new reserve currency? What conditions should be met for this to occur? How will the global monetary system look if the scenario is impossible?

Tesla Inc (TSLA) Is A Busted Growth Story

Tesla Is A Busted Growth Story

We remain short Tesla Inc. (TSLA), which I still consider to be the biggest single stock bubble in this whole bubble market. The core points of our Tesla short thesis are:

- Tesla has no “moat” of any kind; i.e., nothing meaningfully proprietary in terms of electric car technology, while existing automakers—unlike Tesla—have a decades-long “experience moat” of knowing how to mass-produce, distribute and service high-quality cars consistently and profitably, as well as the ability to subsidize losses on electric cars with profits from their conventional cars.

- In 2020 Tesla will again lose money, as it has every year in its 17-year existence.

- Tesla is now a “busted growth story”; revenue growth is flatlining while unit demand for its cars is only being maintained via price cutting.

- Elon Musk is a securities fraud-committing pathological liar.

Broker and Broker

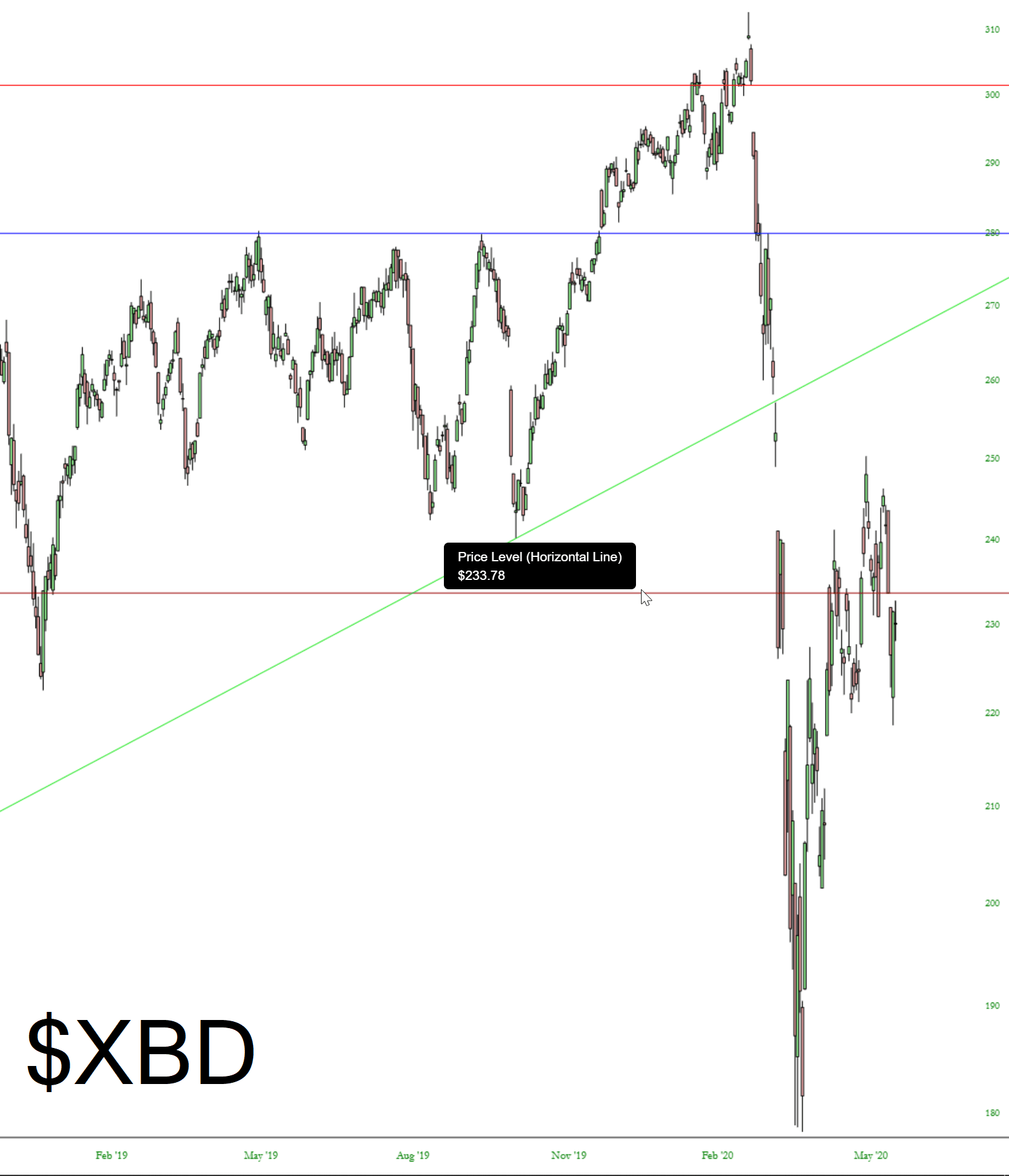

One of the principal reasons for the strength in the small caps yesterday and today is that banks have been recovering. Here are three SlopeCharts that speak to that strength, with particular emphasis on the price gaps. Please click on any given chart for a better view and to clearly read the value of the price gap. Here’s the Broker/Dealer Index:

Insurance Sector: Who’s Zoomin’ Who

Should the insurance sector be left for dead, or is there any semblance of value beneath the multi-layered COVID-19 ruble?

No sectors were immune from the March 2020 left-tail quickening that brought global equities to their knees in a snap reaction to the “Chinese virus” (POTUS’s term), COVID-19’s seemingly inevitable global roll-out, still underway.

(more…)