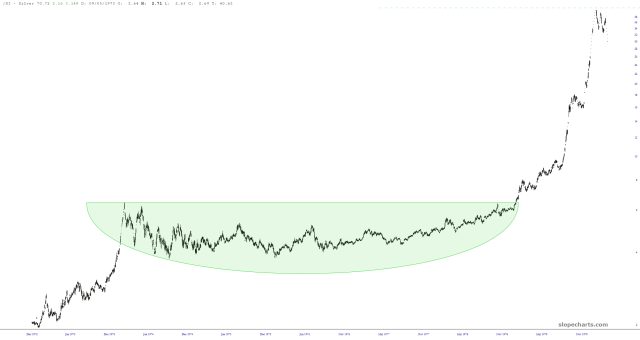

In my book Panic, Prosperity, and Progress, I dedicated a chapter to the famous Hunt brothers silver squeeze of 1979. I won’t recount it here (buy the book instead!) but suffice it to say that their attempt to corner the market pushed silver from about $6.40 to over $40 in the span of a year. In the end, their attempt would fail, and it would bankrupt one of the richest men in the world.