The last time I remember the real estate market in my area being so frenetic wasn’t in 2007, at the peak of the housing bubble, but more like 1999, as the Internet bubble was still swelling. There was a lack of housing supply, and realtors would be pestering homeowners constantly about whether or not they wanted to sell their house. Some shrewd ones took the offer and got out (one friend of mine accepted the obscene amount paid for his house and went to Southern California to start a winery). (more…)

Slope of Hope Blog Posts

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

Long-Term Double-Top on Real Estate

Palo Alto Real Estate

A good friend of mine who, among other things, sells real estate in my little town, mentioned to me in an email this morning that prices had gone “stratospheric.” I’d like to offer you a sample of what he means in a full-color, full-page ad I tore out from this morning’s Palo Alto Daily Post.

I present to you what you can get for $2 million in Palo Alto (truth to tell, it’ll probably go for a meaningful amount over the asking price):

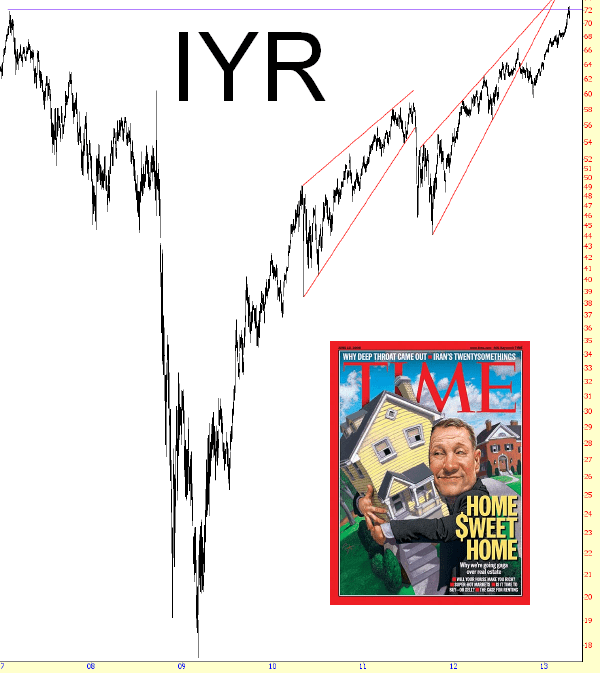

IYR: Looking in the (Bearish) Mirror

Is the Fed's plan to boost real estate values about to go awry…?

(Visit Panzner Insights for more on markets, economics, and geopolitics.)

Consider Another Asset Class: Apartments

Stock markets go up and they go down, and what fun we all have trying to make money along the way. But for those seriously concerned about sheltering their wealth against the coming storm of central bank destruction of fiat value, I propose you might consider investing in apartments as a way to diversify your holdings.

I avoided apartments for years: who wants to deal with fixing someone’s plugged toilet in the middle of the night? But the reality is that with enough starting capital you can turn all those headaches over to managers who will do all the hard work and send you a monthly report on how much money you are making. You just need to enter the game at a price-point high enough to give you economy of scale. This means a place big enough to support paying both on-site and off-site management, unless you are prepared to handle some of that work yourself.

Consider the numbers:

A $500,000 down payment on a carefully selected $2,000,000 apartment complex should return 8 to 10% cash-on-cash return each year. On top of this income, the tenants are paying down the mortgage to the tune of another $30,000 each year. That’s an additional 6% return on investment, for a total return of around 15% annually. (If $500,000 is too much for you, there are also syndicators of apartment buildings who will sell a share of a project, so that the initial cost is more affordable to the normal investor, allowing you in for $50,000 or $100,000.)

On top of that, most of that money is tax-free, due to the depreciation taken on the structure, approximately 3% per year. When you sell the property, there is depreciation recapture to deal with, taking back some, but not all of this advantage, but if you roll the proceeds over into another qualifying property you can keep from paying taxes on this income virtually till you die.

And then there is the protection from the inflation most of us feel will be coming this way at some point; historically, rents have tracked inflation almost exactly, and if your rents go up, your income goes up, the value of the property goes up, and the value of the money you owe on the mortgage goes down. Any increase in value is treated as capital gains, and these profits, too, can be rolled into another property at sale. In my opinion, multifamily is a much better inflation hedge than gold, which may go up in value, but a good portion of that increase will be confiscated by the government as a tax on a “collectible.” With gold as your hedge, you won’t lose as much as everyone else, but you will still lose.

In summary, a careful investment in apartments (and there is a lot of junk out there to be avoided, so be prepared for a lot of work to find the right property) can yield an after-tax return – over ten years – of 150% to 200% in a low inflation environment, and double that in a high inflation environment. How can you match that in the stock market, even if you manage to hit the golden 8% annual return financial advisors used to talk about? Is that even possible any more with bond yields dead on the floor?

I do think that there is a brief window of opportunity here, though, with mortgage rates under 5% (I am presently quoted a rate of 4% for a seven year term/ 30 year amortization on a $2,000,000 loan.) Locking in borrowing now on an income-producing property could be a way to save your future financial life.

And now, back to watching the stock market….

Yours truly,

House of Cards