Some mixed messages come out of this week's CFTC Commitment of Traders Report. Below are six charts with my best estimate of what the data is telling us. The three key takeaways are

- Commercial traders appear positioned for further bond weakness

- Commercial traders are reducing net short positions implying copper weakness

- Retail traders are positioned for further USD weakness, implying USD strength

Bonds

Looking purely at the relationship to 30 year yield and the SPX, this chart implies that further bond weakness (lower price higher yield) would be a positive for the SPX. This cannot be taken purely at face value though. There are many implications to a weakening bond market beyond this chart. Still, the data below would imply continued equity strength.

Bonds – Commercial Net

Commercial positions continue to move towards a more net long in the face of 30 year weakness. At face value this chart would imply further bond weakness to come. It's important to note though that commercial positions are approaching a 52 week high.

USD – Commercial Net

This is a tough one to read. The commercial trader position is net long and matches that of the prior 52 week high. It is very possible their net long position grows but considering this position relative to the prior 52 weeks, it is quite possible they begin getting more short which would imply USD strength. The USD has bounced off key support which would further argue for a reversal to a more short commercial net position.

USD – Commercial VS Retail Net

This next chart is that of the non reporting positions versus commercial positions. Non reporting (retail) are relatively short versus prior times in the year so there is fuel for a short squeeze in the USD. Hard to make any definitive call though.

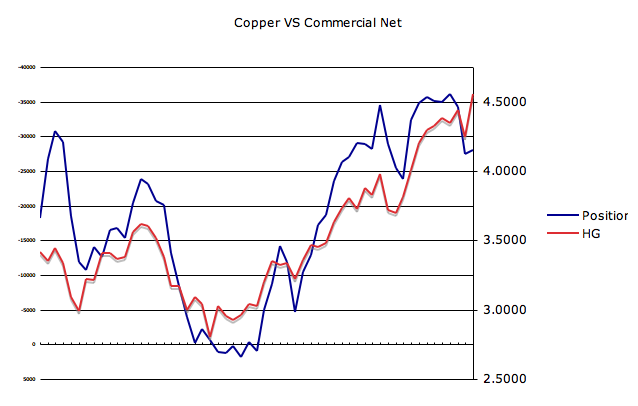

Copper – Commercial Net

This is a rather interesting chart. Copper caught a nice bid the past week yet the commercial traders are not buying it (literally). They appear to be getting more net long (this chart is inverted for comparison sake) which would imply pending copper weakness.

Copper – SPX VS Commercial

Nothing too definitive can be drawn here other than a word of caution for the SPX as commercial positions appear to becoming more net long (chart is inverted for comparison sake).

Submitted by Ultra Trading. If you would like to read more, please visit my blog - Ultra Trading

{kind=link}