Color, Mania, and Hedging Gold

Below are some thoughts on hedging gold, but before that, a quick aside, prompted by a chapter I read today in The Slope of Hope Bathroom Reader. On p.28 ("Color and Mania in the Valley), Tim mentions the mobile app Color, the creators of which received an astonishing $41 million in venture financing, as an example of the recent bubble in tech. As it happens, one of my daily clicks is the iOS app tracker AppShopper.com, which provides hourly rankings of Apple iOS apps. (Editor's Note – thanks for the book mention, Dave!)

I have the top-200 grossing finance app rankings bookmarked (on which I was pleasantly surprised on Thursday to see Portfolio Armor break into the top-5 for the first time), but after reading the Mania chapter in the Slope Bathroom Reader, I looked up Color out of curiosity. Appshopper classifies it as a social networking app, so I checked looked for it on AppShopper's top-200 grossing ranking of social networking apps (Color is a free app, but free apps still appear in the top-200 grossing rankings, if they generate enough revenue from in-app sales or other sources). Last I checked, it wasn't anywhere on the list.

Now to gold.

Not too late for gold longs to hedge

After suffering its largest two-day drop in dollar terms in 30 years, and one of its 10 largest corrections in percentage terms in 30 years on Tuesday and Wednesday, gold ticked up 0.49% on Thursday. The SPDR Gold Trust ETF (GLD) ticked up a similar percentage, 0.42%. It's more expensive to hedge gold via optimal puts on GLD now than it was earlier this summer, as the second bullet point below shows, but there are reasons why gold longs may still want to hedge.

Let's consider why gold longs should consider hedging here, and then run through a quick step by step example of hedging via optimal puts on GLD.

Why Gold Investors Should Consider Hedging

Earlier this month, the FT's Lex Column ("Gold: pinpointing the peak") noted a reason why gold might have some more room to run, but also a warning of why the peak may be near.

Room To Run?

Lex noted that despite its current, nominal highs, adjusted for inflation, gold is still 30% below its 1980 peak.

A Warning

Despite the potential room for gold to run, Lex pointed raised this red flag:

One classic warning of a peak – a rush of what professionals call dumb money – is already evident. Look at iShares’ gold trust IAU, which holds 12m ounces. It has seen a disproportionate rise in small buyers. The number of accounts with fewer than 1,000 shares (100 ounces) has trebled in the past year while large ones have barely budged.

[…]

The rush for the exits, whenever it comes, will be lively.

Being Hedged Means Not Having To Rush For The Exits

If you own gold, and you're hedged, you can find out how much more room gold has to run, confident that your downside in the face of a major correction will be limited.

1980 vs. 2008

If you're hedged when the next correction in gold hits, you'll have the breathing room to consider whether that correction is analogous to 1980's crash from gold's generational peak or to 2008's sharp, though temporary, correction.

Remember that in 2008 gold fell to a low of $712.50 per ounce, after having peaked at over $1,011 per ounce earlier in the year. A gold investor who had been hedged could have, if he were still bullish on gold at that point, sold his hedges and used the proceeds to increase his position in gold.

A Step By Step Example Of Hedging With Optimal puts

Below we've demonstrated a way to hedge GLD, using optimal puts. First a quick reminder about what optimal puts means in this context.

About optimal puts

Optimal puts are the ones that will give you the level of protection you want at the lowest possible cost. As University of Maine finance professor Dr. Robert Strong, CFA has noted, picking the most economical puts can be a complicated task. With Portfolio Armor (available on the web and as an Apple iOS app), you just enter the symbol of the stock or ETF you're looking to hedge, the number of shares you own, and the maximum decline you're willing to risk (your threshold). Then the app uses an algorithm developed by a finance PhD to sort through and analyze all of the available puts for your position, scanning for the optimal ones.

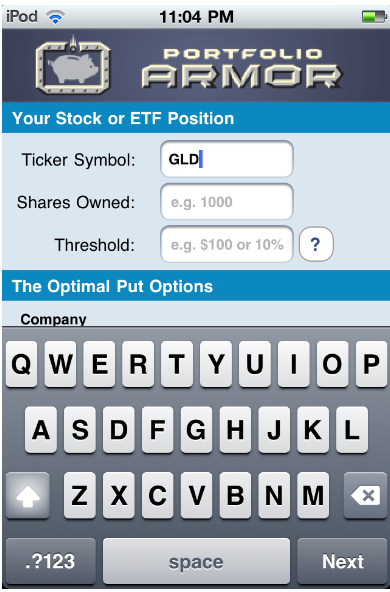

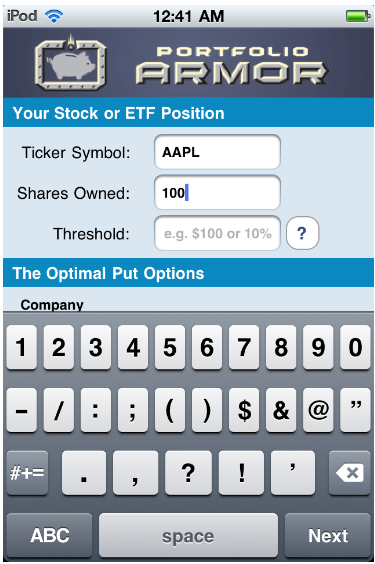

Step 1: Enter a ticker symbol

In this case, we're hedging GLD, so we've entered it in the "Ticker Symbol" field below:

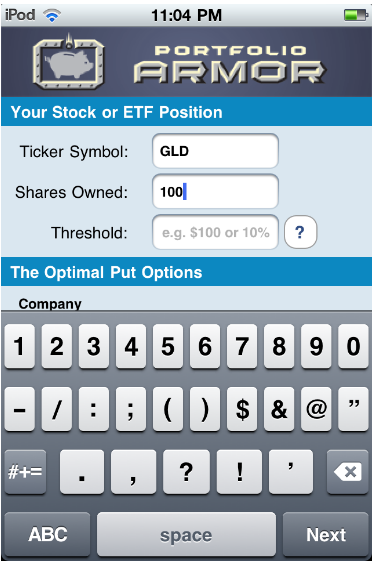

Step 2: Enter a number of shares

For simplicity's sake, we've entered 100 in the "shares owned" field below, but you could also enter an odd number, e.g., 931 (in fact, if you were using GLD as a proxy for your physical gold holdings here, that's probably what you'd end up with, as you'd divide the current dollar value of your physical gold by the most recent share price of GLD to get your number of shares).

In that case, Portfolio Armor would round down the number of shares of GLD you entered to the nearest hundred (since one put option contract represents the right to sell one hundred shares of the underlying security), and then present you with 9 of the put option contracts that would slightly over-hedge the 900 shares of GLD they cover, so that the total value of the 931 shares of GLD would be protected against the decline threshold you select.

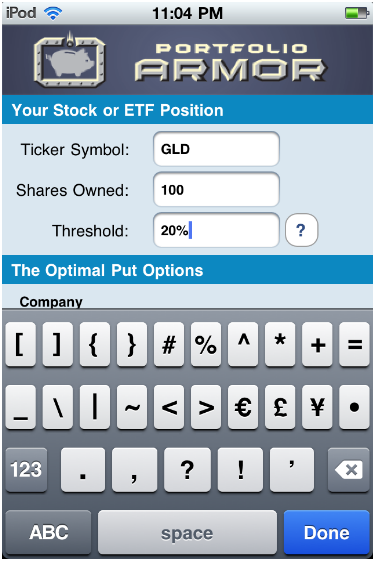

Step 3: Enter a decline threshold

You can enter any percentage you like for a threshold when using Portfolio Armor (the higher the percentage though, the greater the chance you will find optimal puts for your position). The idea for a 20% threshold comes, as I've mentioned before, from a comment fund manager John Hussman made in a market commentary in October 2008:

An intolerable loss, in my view, is one that requires a heroic recovery simply to break even … a short-term loss of 20%, particularly after the market has become severely depressed, should not be at all intolerable to long-term investors because such losses are generally reversed in the first few months of an advance (or even a powerful bear market rally).

Essentially, 20% is a large enough threshold that it reduces the cost of hedging but not so large that it precludes a recovery. So we've entered 20% in the Threshold field in the screen cap below.

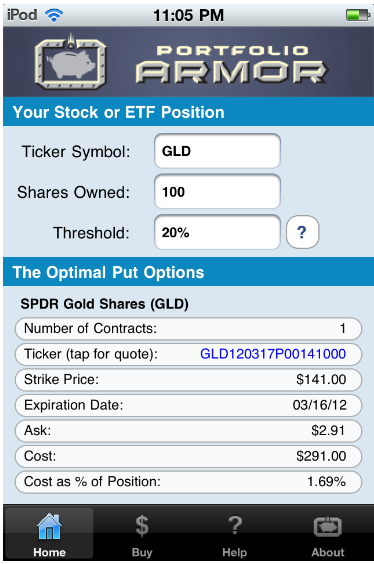

Step 4: Tap the "Done" button

A moment after tapping the blue button, you'd see the screen cap below, which shows the optimal put option contract to buy to hedge 100 shares of GLD against a >20% drop between now and March 16th, 2012. Two notes about these optimal put options and their cost:

Two notes about these optimal put options and their cost:

- To be conservative, Portfolio Armor calculated the cost based on the ask price of the optimal puts. In practice an investor can often purchase puts for a lower price, i.e., some price between the bid and the ask.

- As volatility has climbed, so have hedging costs. The VIX S&P 500 volatility index closed at 39.76 on Thursday. On May 5th, when the VIX was at 18.20, the cost of hedging GLD against a >20% decline over roughly the same length of time was only 0.85%, as we noted in this post at the time. As the screen shot below shows, as of Thursday, the cost as a percentage of position was 1.69%.

Disclosure: I am long puts on GLD — not as a hedge, as I don't own any gold or GLD, but as a speculative bearish bet against gold.

{kind=link}