Further to my last weekly market update, this week's update will look

at:

- 6 Major Indices

- 9 Major Sectors

- Index/Volatility Ratio Charts

- 30-Year Bonds

- U.S. $

6 Major Indices

Inasmuch as today (Friday) was a Quadruple Options

Expiration, I'm showing the following chartgrid, where each candle

represents a 1-month options expiration period. You can see that the

current candle, which closed today, basically, bounced at/near the mid-Bollinger

Band. Price is stuck within a sideways range and is at/near major resistance.

We may see some retracement on the next candle, which begins on Monday,

before these indices either attempt to break out of and hold above this range

to, potentially, rally to their upper Bollinger Band, or retreat to lower

levels, such as their lower Bollinger/50 sma confluence major support levels.

You will note that the Dow Transports is already at its upper Bollinger Band and

the Russell 2000 is just below.

I'd watch the Russell 200 for either

leadership in a push upwards or a pullback.

The following

Year-to-date Weekly chartgrid shows the extent of this week's

gains, as does the following 1-Week percentage gained/lost

graph.

The largest gains were made in the Dow Transports and

Russell 2000 Indices.

9 Major Sectors

The first chartgrid also depicts a 1-month

options expiration period, with the current candle closing today. You

can see that all sectors retraced some or all of the prior period's pullback.

They are all in either longer or shorter-term sideways ranges, and are also

at/near major resistance, with Consumer Discretionary, Consumer Staples,

Healthcare, and Technology leading in overall gains from the 2009 lows.

We may also see some retracement on the next candle, which begins on

Monday, before these indices either attempt to break out of and hold above this

range to, potentially, rally to their upper Bollinger Band, or retreat to lower

levels, such as their lower Bollinger/50 sma confluence major support levels.

I'd watch the Consumer Discretionary and Staples, Healthcare, and

Technology Sectors for either continued leadership in a push upwards or a

pullback.

The following

Year-to-date Weekly chartgrid shows the extent of this week's

gains/losses, as does the following 1-Week percentage gained/lost

graph.

The largest gains were made in the Financials Sector,

while Consumer Staples lost some ground.

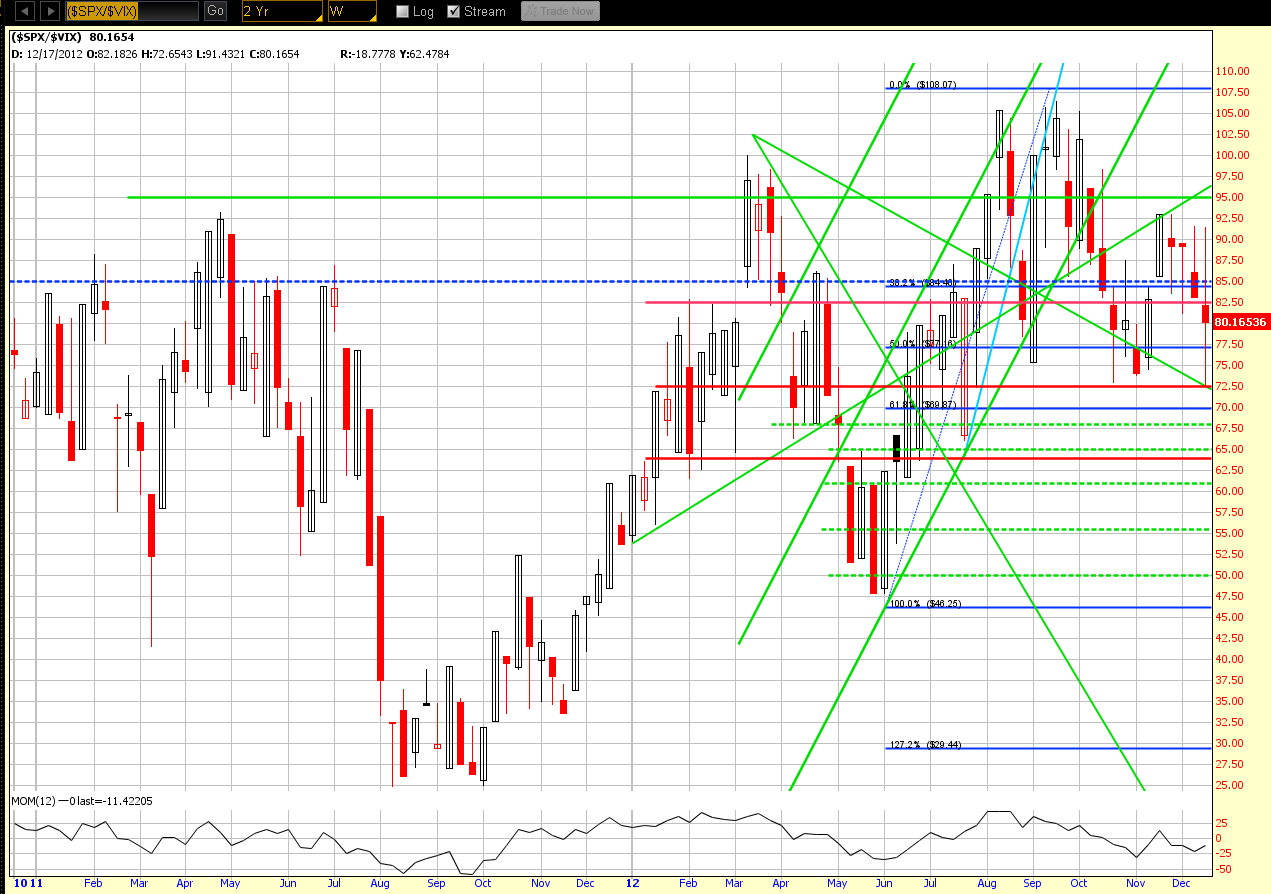

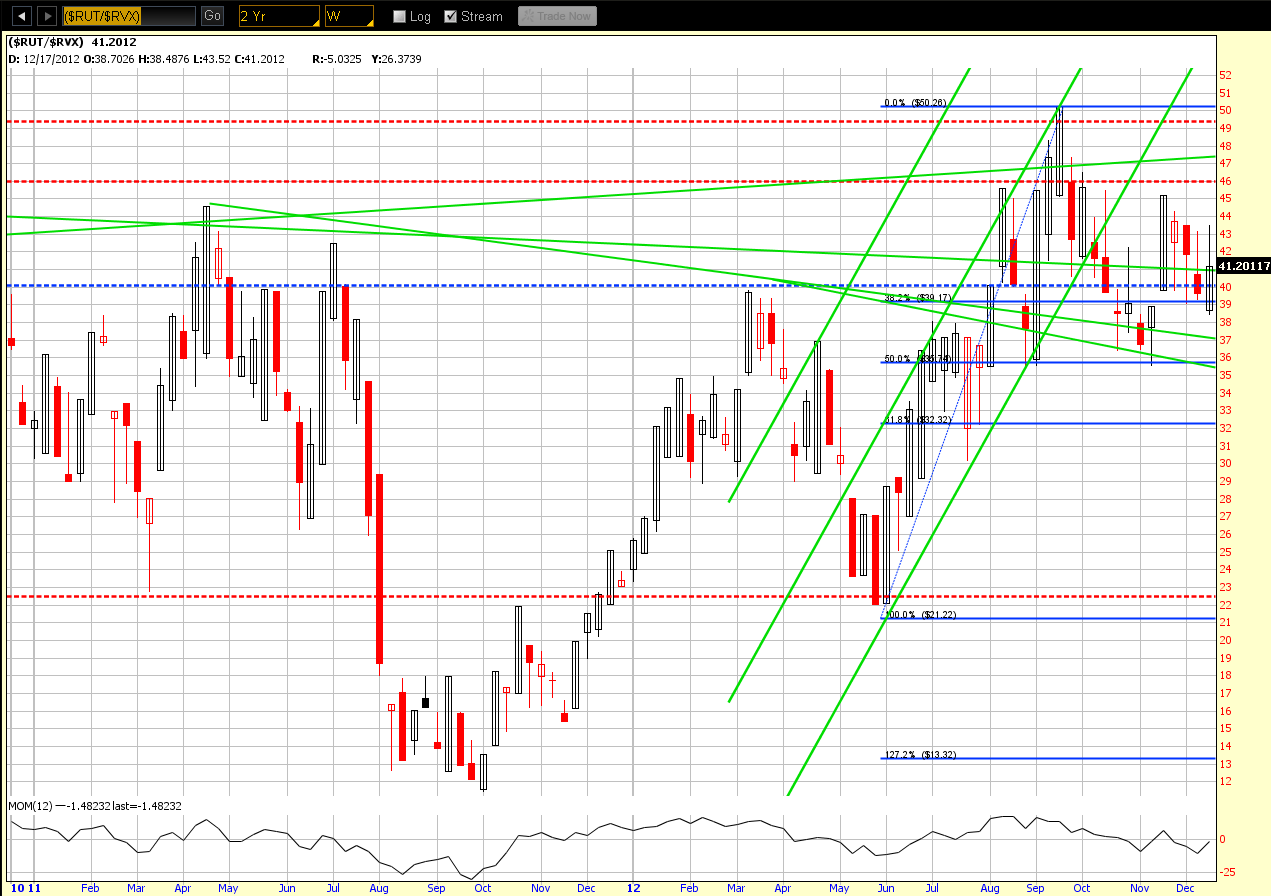

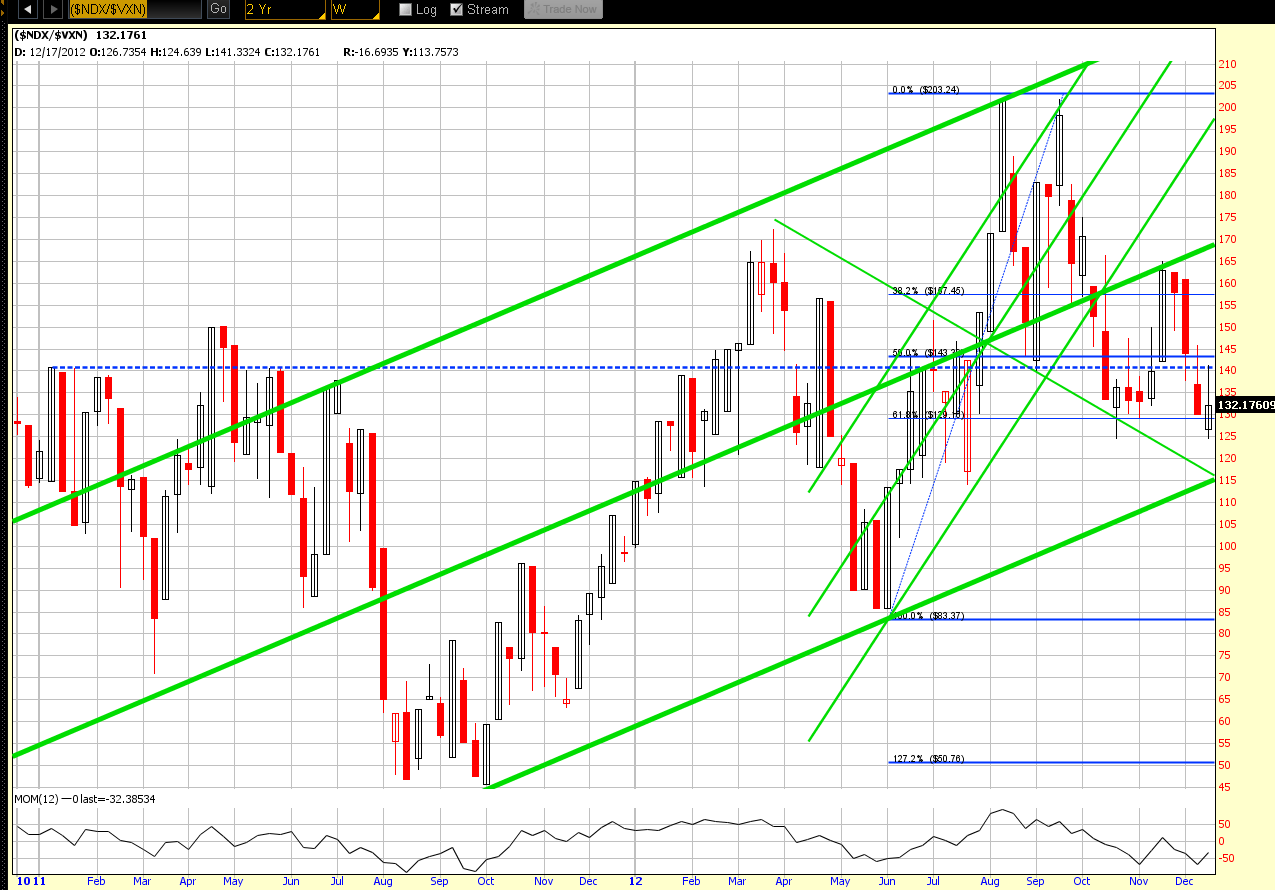

Index/Volatility Ratio Charts

Normally I'd show Daily charts, but

have opted to show the following 2-Year Weekly ratio

charts comparing the SPX, RUT, and NDX to their respective Volatility

Indices.

You can see that each one closed roughly in the middle of its

weekly candle, after a week of what was particularly high volatility for the

SPX…basically indicating indecision and lack of commitment in either direction

in these markets. The SPX:VIX and NDX:VXN ratio pairs closed below major

resistance (broken horizontal blue line), while the RUT:RVX ratio pair closed

just above.

With volumes expected to be lower overall next week during

the Christmas holidays, we could actually see an increase in volatility with

large moves and little follow-through…probably something we'll continue to see

until a deal is (presumably) reached before the end of the year on the "Fiscal

Cliff" issue.

30-Year Bonds

The Weekly chart below of 30-Year

Bonds shows that price also finished near the middle of this week's candle and

is back in the middle of a longer-term sideways trading range from mid-May…so,

there is no indication of panic selling in these bonds, yet.

U.S. $

The Weekly chart below of the U.S. $ shows

that price finished near the top of this week's candle and at the Volume Profile

POC (point of control) for the past 5 years. It's been in a 2-point trading

range since mid-September, and remains the risk-on/risk-off trade, along with

30-Year Bonds.

In

summary, we may continue to see volatile intraday/overnight swings with

little follow-through on lower volumes, until the "Fiscal Cliff" issue is

settled and until the end of the year, as fund managers re-organize their

portfolios for the 2012 year-end and Q4. At the moment, equity markets still

appear to be hedged in Bonds and the U.S. $ as they trade near major resistance

levels…this will likely continue until a convincing and sustained breakout

occurs in equities. As well, I continue to watch the Fed monetary stimulus program "canaries" and the 1.3250ish resistance level on the EUR/USD forex pair as

possible indicators of equity weakness that may become a cause for concern by

bulls…at the moment, they are signalling caution, as I discussed in those two

articles this week.

Merry Christmas and have a safe and Happy Holiday

week. Good luck to anyone trading next week!