One way to play for both a gain or loss in a stock is to buy a straddle. This involves buying a call and a put at the same time wherein a certain degree of gain or loss in a stock will result in profit, and if there is no or small movement in the stock’s price, there is a small loss that will increase with time. In addition the straddle does better in rising volatility, such as prior to earnings, and worse in pre-existing high volatility which is dropping.

Another strategy that can take advantage of a potential directional opinion, is to obtain a straddle with a mix of stock and options. One can use synthetics to achieve this.

Moreover – A long stock position is equivalent to a long call and short put of the same strike. A short stock position is equivalent to a short call and long put of the same strike.

If one has a short and two 30-40 delta calls, this is equivalent to owning both a put and a call, skewed to the downside. One advantage of this strategy is that if the calls are less expensive than the puts (due to option price skew), there is an advantage. Also there is no theta decay or volatility influence on shorting the stock (only the calls will be affected by time decay and volatility).

Overall the short (-100 delta) and the calls (+70 delta) are skewed to the downside (-30 delta), and so any drop in the stock will result in profit. Small gains will result in a small loss, getting worse with time, and large gains will be fully hedged, resulting in significant gains. A stop loss for the short is not needed with the strategy.

This would be an ideal strategy when one believes there is a good chance for a drop in the stock’s price in the near future. It also is a decent strategy pre-earnings, due to rising volatility offsetting theta decay. It is not a good strategy for slowly uptrending stocks, or for high volatility conditions.

Let’s take a look at some examples for some Tim’s recent shorts.

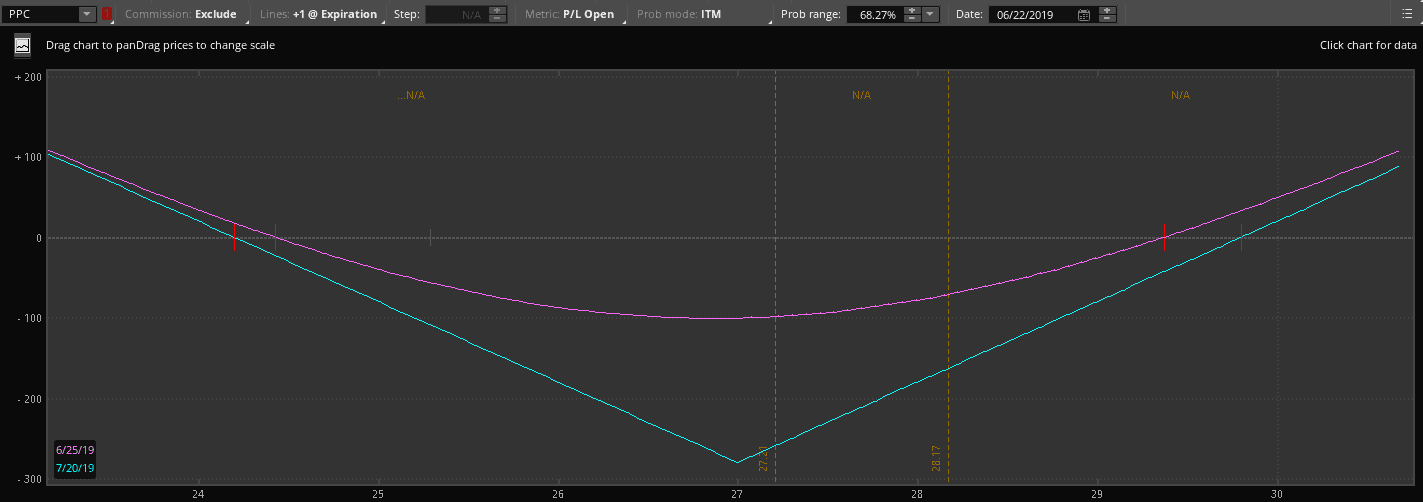

First let’s take a look at PPC (Pilgrim’s Pride)

A straddle bought with expiry in 3 months (20 SEP 2019), at the $25 strike, and is a small loser between the $23 and $26 price points. But let’s look at a different trade.

Let’s short 100 shares of PPC, and then buy two 19 JUL 2019 calls, at 40 cents each ($40). The breakeven is $24.43 on the downside. Upside breakeven is $29.38. This trade is specifically a bearish one.

However, if there is a significant gap up in the stock, the losses will be capped at $277 (vs unlimited theoretical losses). This only adds $80 to the trade cost, which is marginal. Again this trade is NOT a nondirectional trade – if you believe PPC is going to go up it would not be appropriate.

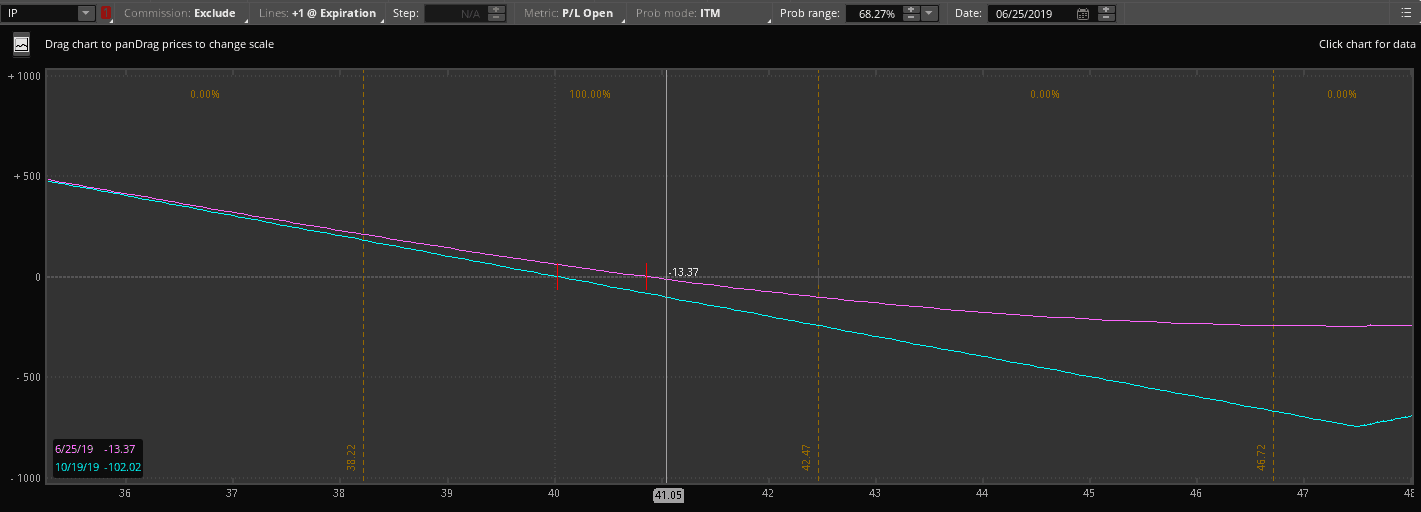

One more – let’s look at International Paper (IP)

Here we can short the stock, and also buy two 47.5 calls expiring 18 OCT 2019. These will hedge a massive gain, and cost $154 from our short that will give a credit of $4,250.

The best times to use this strategy are when calls are cheaper than puts, volatility is relatively low OR is persistently rising, and when there is a strong bias to the downside based on charting or other factors. No strategy is perfect or appropriate for all conditions.