In a recent post (“Crude Strategy“), I mentioned a hedged bet on the ProShares UltraShort Oil ETF (DUG):

One of Portfolio Armor‘s top ten names on Thursday was the ProShares UltraShort Oil & Gas ETF (DUG). The system picked it based on the same quantitative analysis of past returns and forward-looking options sentiment it applies to every stock and ETF, but if you want a story behind that pick, it’s pretty simple:

- You’re not doing a lot of driving now, because we’re all basically under house arrest due to certain people eating bat soup.

- The Saudis have opened up the spigots to punish the Russians for not sticking to OPEC quotas.

- Some analysts are calling for $5 per barrel oil, or even negative oil prices regionally.

The challenge here is that DUG is highly levered and can blow you up if you end up being wrong. A solution to that is to buy DUG and hedge it with an optimal, or least-expensive collar.

It occurred to me that we’ve been here before: Portfolio Armor picked DUG during another market decline, albeit one much less serious than this one. In that case, it ended being wrong about it. Let’s look at what the consequences of that were.

Betting Against Oil In Late 2018

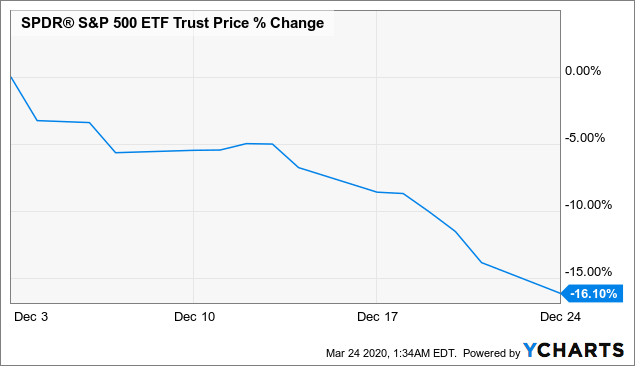

Readers may recall the market swoon of December 2018, but if you don’t the chart of the SPDR S&P 500 ETF (SPY) below may refresh your memory.

At the time, it wasn’t clear if we were heading into a bear market and a recession or not: we were at an inflection point where it looked like it could go either way.

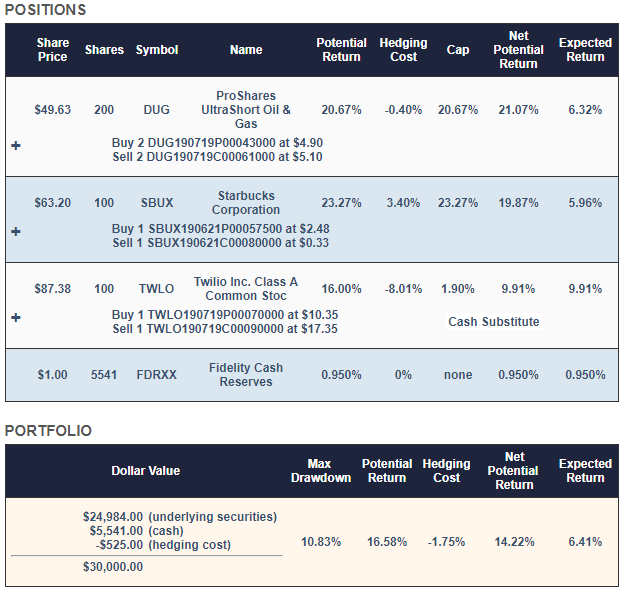

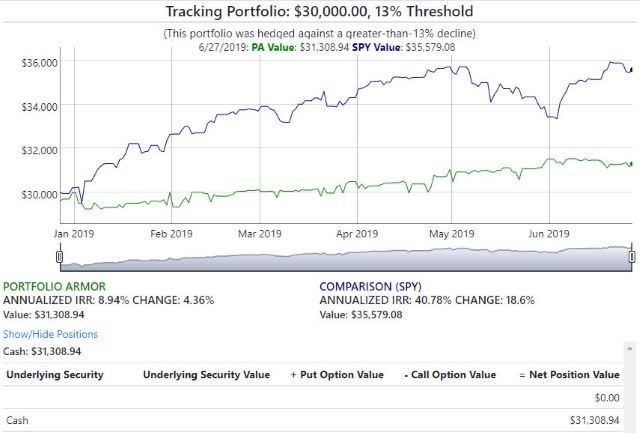

In that context, this is the hedged portfolio Portfolio Armor presented to an investor who indicated he had $30,000 to put to work but wanted to strictly limit his downside risk to a decline of no more than 13% over the next 6 months:

Because this portfolio had a lower dollar amount ($30,000 is the minimum size of Portfolio Armor’s hedged portfolios), it only included two primary securities: Starbucks (SBUX) and DUG. After initially allocating roughly equal dollar amounts to each, the site rounded down each dollar amount to get round lots to minimize hedging cost. Then it used Twilio (TWLO) – tightly hedged, with a collar capped at the then-current money market yield – to absorb most of the leftover cash from the rounding down process.

What Happened Next

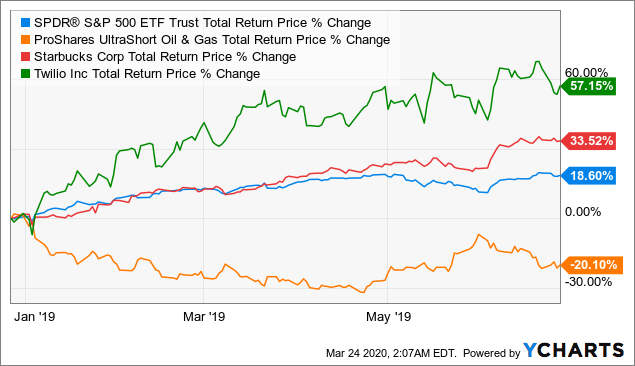

As it happened, we didn’t have a recession in 2019, and instead of slipping into a bear market, we had a v-shaped recovery in stocks, with SPY returning more than 18% over the next 6 months, while Proshares Ultrashort Oil ETF DUG dropped more than 20%.

So, Portfolio Armor was wrong on DUG. How’d that hedged portfolio from December 27th do over the next six months (the site’s hedged portfolios last 6 months each)? Not great, versus SPY, but it still posted a positive return, despite getting DUG wrong.

That hedged portfolio ended up returning 4.36% over 6 months, net of hedging and trading costs, despite getting DUG wrong.

Heads You Win, Tails You Don’t Lose Too Much (Or Even Get A Small Gain).

That’s the essence of the system’s approach: it picks names it estimates will do well over the next 6 months, and presents hedges so that, if it’s wrong, you don’t loose to much – or in the case of the portfolio above, make a small gain.