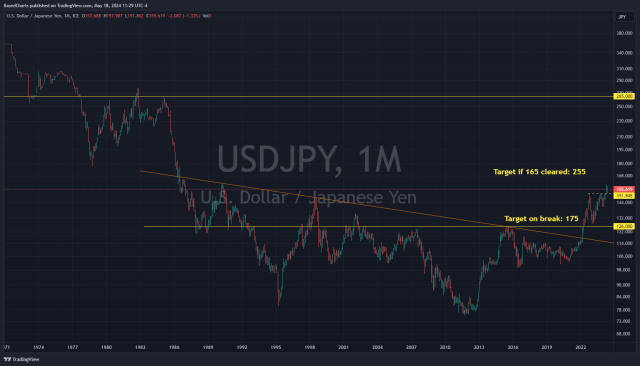

Japan isn’t a normal situation though, where recession would likely be bad for stocks. Japan is a potential monetary disaster in the making. Their currency sports a huge bullish base that has already broken out, and the target off both the large base and the consolidation from 2022-2024 is 175.

Beyond 165 a larger base is complete. The rapid descent in USDJPY on the left side of the chart was caused by the 1985 Plaza Accord. Given Japan’s monetary follies the past three decades, a rapid ascent for USDJPY is well within the realm of possibility.

If Japan chooses to inflate into a recession, perhaps they suffer a forex catastrophe. In that case, the Nikkei becomes a hideout for Japanese investors. WisdomTree Japan Hedged (DXJ) had a portfolio tilted in favor of firms that would benefit from a weaker yen, plus hedges out the currency risk. It’s the go-to fund for a currency devaluation that lifts stocks.

More context.

Nikkei in USD

SPX to Nikkei

SPX_NI225

SPY/EWJ has less history, but shows the same pattern.

Ratio charts between the S&P 500 and foreign markets generally present a similar picture: U.S. markets are overvalued or trading at relative prices that are near or beyond prior peaks. Longer-term, a long period of outperformance by foreign markets is likely (pick your markets carefully though.)

Aside from the ratios, Japanese stocks aren’t overvalued as they were in 1989. The forward P/E ratio is 15.3 versus 21 for the USA. Japan has embarked on a wave of shareholder-friendly reforms too. It isn’t the cheapest country out there. China, many emerging markets and some in Southern Europe have lower price multiples. Still, if the context is the U.S. market is among the most overvalued, then most other markets should outperform on a relative basis moving forward.