Considering the exceptionally expensive IPOs coming at us, such as SpaceX, OpenAI, and Anthropic, I was curious as to historical examples of hotly anticipated IPOs and their correlation with market tops.

The clearest historical examples are these:

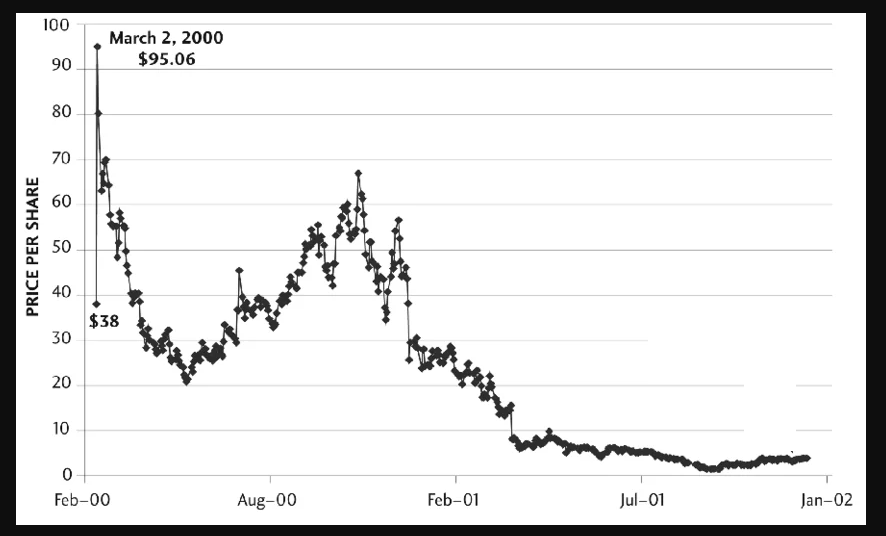

1. Palm / dot-com IPO wave — March 2000

This is probably the strongest example. Palm’s carve-out IPO from 3Com priced at $38 on March 2, 2000, opened at $150, traded as high as $165, and closed at $95.06 on its first day — a 150% first-day gain. Within the same month, the stock had already fallen more than 50% from its first-day close.

The mania was extreme enough that Palm’s first-day valuation created the famous “Palm–3Com stub” anomaly: Palm traded so richly that, arithmetically, the rest of 3Com was being valued at a large negative amount. Chicago Booth describes this as an extreme case of mispricing.

The timing was striking. The Nasdaq peaked on March 10, 2000, at about 5,048 and then fell roughly 77% by October 2002.The broader S&P 500 reached its dot-com-era intraday high on March 24, 2000.

Verdict: Very strong example. Palm did not “cause” the top, but it was almost perfectly timed as a public-market expression of dot-com excess.

2. Blackstone — June 2007

Blackstone’s IPO was a major late-cycle event for the private-equity/credit boom. It priced at the top of the range, raised $4.13 billion, and Reuters described it as the largest U.S. IPO since 2002 and a “watershed event” for the booming private-equity industry. Its debut was heavily demanded: Reuters reported the offering was about seven times oversubscribed.

The S&P 500 did not top immediately; it made its record close on October 9, 2007, and hit its intraday record on October 11. But Blackstone was very close to the peak of the leveraged finance/private-equity cycle. The New Yorker later noted that Blackstone’s stock peaked on its first trading day, while the credit crisis was already beginning to surface through the collapse of Bear Stearns hedge funds.

Verdict: Strong but less exact. It marked a top in the credit/private-equity cycle and came a few months before the broad equity-market peak.

3. Rivian / Coinbase / 2021 IPO-SPAC boom — 2021

This one is more of a cluster than a single bell-ringing IPO. Nasdaq described 2021 as a record year, with more than 1,000 new listings, $286 billion raised, an average first-day IPO “pop” of 34%, and roughly 80% of 2021 IPOs not yet profitable.

Coinbase’s April 2021 direct listing was not a traditional IPO, but it was a huge public-market validation moment for crypto: Reuters reported an $85.78 billion fully diluted valuation at the close and noted that the debut came amid a surge in cryptocurrency values. Rivian’s November 2021 IPO was even more tightly timed to the equity-market top: Reuters reported that Rivian raised about $12 billion, making it the biggest U.S. IPO since Alibaba, and that it briefly ranked ahead of GM and Ford despite having little revenue.

The Nasdaq made a record close of 16,057.44 on November 19, 2021, just nine days after Rivian’s IPO. By March 7, 2022, the Nasdaq had fallen more than 20% from that November record, confirming a bear market. The S&P 500 peaked later, on January 3, 2022, before falling 25% into October 2022.

Verdict: Strong for speculative-growth/tech sentiment; somewhat less clean for “the stock market in general” because the broad S&P top came several weeks after the Nasdaq top.

The practical lesson

A famous IPO by itself is not a reliable sell signal. Many major IPOs happen in bull markets that continue. The useful warning sign is broader: a flood of issuance, extreme oversubscription, large first-day pops, tolerance for unprofitable or barely revenue-generating businesses, and insiders or private sponsors selling into a euphoric public market.

That mechanism is consistent with IPO-market research: one influential model argues that issuers time IPOs to take advantage of optimistic valuations and investor sentiment, even when offer prices exceed fundamental value.