(I posted this on my blog in November. It might be more than Slopers may want to slog through, but it might be worth a cursory view).

I've become recently intrigued with an institution that I rarely

hear anything about: The Federal Home Loan Bank (FHLB). With the

implosion the credit markets involving all things related to home

financing, this agency came under the purview of the FHFA along with

Fannie and Freddie. My objective is not to go into any exhaustive

analysis or even cultivate an opinion. Rather, I'm just reminding you

of this banking system that we does not get much press–and to hit a

few high points. I've no special knowledge on any of this, and

everything that I present here is from 'stuff' easily found on the

internet.

Here's an overview from their website that you can find here. The emphasis added is mine.

The

Federal Housing Finance Agency (FHFA) was created on July 30, 2008,

when the President signed into law the Housing and Economic Recovery

Act of 2008. The Act created a world-class, empowered regulator with

all of the authorities necessary to oversee vital components of our

country’s secondary mortgage markets – Fannie Mae, Freddie Mac, and the

Federal Home Loan Banks. In addition, this law combined the staffs of

the Office of Federal Housing Enterprise Oversight (OFHEO), the Federal

Housing Finance Board (FHFB), and the GSE mission office at the

Department of Housing and Urban Development (HUD). With a very

turbulent market facing our nation, the strengthening of the regulatory

and supervisory oversight of the 14 housing-related GSEs is imperative.

The establishment of FHFA will promote a stronger, safer U.S. housing

finance system. As of June 2008, the

combined debt and obligations of these GSEs totaled $6.6 trillion,

exceeding the total publicly held debt of the USA by $1.3 trillion. The

GSEs also purchased or guaranteed 84% of new mortgages. Considering

the impact of these GSEs on the U.S. economy and mortgage market, it is

critical that we intensify our focus on oversight of Fannie Mae,

Freddie Mac, and the Federal Home Loan Banks.

I thought the

highlighted text to be an eye-popping fact. There are two other GSE's:

Farmer Mac (AGM) and the Farm Credit Administration–both serving

agriculture. Readers may remember the lonely trade that I did not

take–shorting AGM. Here's the post. Let it serve as a reminder that there are many jewels of ideas for trading that are not in mainstream media.

The FHLB is a collection of 12 banks (with links to their websites):

Boston | New York | Pittsburgh | Atlanta | Cincinnati |Indianapolis | Chicago

Des Moines | Dallas | Topeka | San Franciso | Seattle

Each

of the above are wholesale banks serving as a cooperative within the

geographic areas that they serve. As a cooperative, they have members

FHLBank

members include thrift institutions, commercial banks, credit unions,

and insurance companies. A financial institution joins the FHLBank

district that serves the state where the institution's home office or

principal place of business is located.

From website.

which purchase stock from the FHLB that serves that geographic area of the member.

The

FHLB system allows member banks access to affordable financing for

their lending operations. The member banks, in exchange for these

loans, pledge collateral. Accordingly, the FHLB debt issuances are

supported by collateral. The quality of this collateral is

derivative–meaning that the value is ultimately derived from: (1)

credit quality of the end borrowers and (2) valuation of the

collateral. You see where I'm going with this, right?

The table below is taken from the July 2009 Report on Federal Home Loan Bank Collateral for Advances and Interagency Guidance on Nontraditional Mortgage Products This table shows the concentration of Subprime and Non-traditional Mortgage Collateral.

(Click image to view)

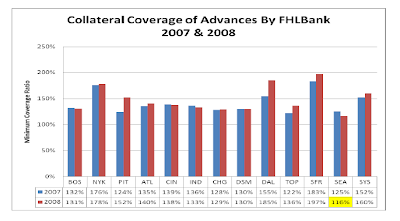

The next table shows the loan to collateral ratio

(Click image to view)

Source: July 2009 Report on Federal Home Loan Bank Collateral for Advances and Interagency Guidance on Nontraditional Mortgage Products

Source: July 2009 Report on Federal Home Loan Bank Collateral for Advances and Interagency Guidance on Nontraditional Mortgage Products

The

highlighted data point is FHLB-Seattle which was recently cited by the

FHFA as being under capitalized. The last column is the system wide

coverage ratio of 160% which increased from 152% in 2007. Also it is

important to note that each FHLB is jointly and severally liable for

the obligations of the others.

The collateral offered may also

include mortgage backed securities that the member banks might hold. It

is a reminder of the cyclical nature of of this 'stuff'. Fannie Mae,

Freddie Mac and Ginnie Mae securities that many conservative

institutions bought due to their perceived safety. It is important to

note that ONLY Ginnie Mae Securities are backed by the full faith and

credit of the United States. Freddie and Fannie are 'wards of the

state' as the are in conservatorship. But the domino effect of an

implosion is evident as these balance sheet holdings served as

collateral and supported capital of the institutions that held them.

For any of you who read financial statements, the next graphic Taken from

First Federal of Northern Michigan Bancorp, Inc.

press release shows where you see the stock purchased from FHLB as well as the advances.

(Click image to view)

If

any of this whetted your appetite to learn more, I'd encourage you to

seek out the following resources and perhaps appropriate counseling!