The stock market has been lurching forward with surprising force. For armchair economists, one looks about and can only head scratch about the anomalous behavior of the market v. 'reality.' While the market is a discounting mechanism, I will go to my grave believing that it is as perfect at discounting as a teenage boy is at restraint.

Marc Faber's cogent observation that economic reality and the market's perception of economic reality are two different things was an important "AHA" experience for me.

Another important quote that I found in going through my blog archives was one given to me by a fellow blogger from Bill Cara's site. It was attributed to George Soros, though I've never verified that:

“Economic history is a never-ending series of episodes based on falsehoods and lies, not truths. It represents the path to big money. The object is to recognize the trend whose premise is false, ride that trend, and step off before it is discredited."

G. C. Selden writes in his book, Psychology of the Stock Market, the following:

The main point of their argument is that the state of mind of a man short of the market is radically different from the state of mind of one who is long. Their whole study, in such a conversation, is the mental attitude of those interested in the market. If a majority of the volatile class of in-and-out traders are long, many of them will hasten to sell on any sign of weakness and a decline will result. If the majority are short, they will buy on any development of strength and an advance may be expected."

And that leads me to this:

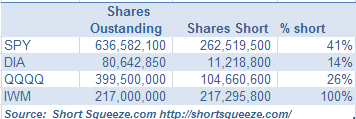

Is it possible that 100% of the IWM is really short? Forty percent of the SPY? If these numbers are true, is it any wonder then that we have these surges of buying on moderate strength? To my amateur eye, these high levels of short interest preclude a major correction until they are reduced. However, I do find these numbers a bit troublesome, as I'm having a difficult time corroborating any by the SPY (FINVIZ reports 44%). I cannot find numbers for the others. The numbers (should one be able to find credible numbers) bear watching.

(Editor's Note: I've never used shortsqueeze, but I find these figures in the table above very, very suspicious. I could be wrong, but I think it's impossible the entire float of IWM is short. Looking at this link, which is specific to IWM, this site cites a high price of IWM of $512.70, which is grossly wrong. So it could well be that the site is just packed with absolutely crap data; this is no reflection on Leisa, but I'd appreciate hearing comments about shortsqueeze.com and if it's worthwhile or not – – Tim).