The problem with group think is that thinking is not allowed. It should really be called group acceptance. The larger the group the harder the tendency for someone to disagree. Right now the group is massive. The group think I am referring to is with the Fed, the Bernanke put and how the Fed will "just print more money and bail out the banks."

I have yet to read the Art Of War (have owned it for about 15 years now) but somewhere in there I am sure it talks about giving your enemy more credit and not simply labeling them as stupid or inferior. The Fed is a smart group of people, albeit lacking in practical real world business sense. The banks are benefitting for sure from playing the role of broker as the Fed expands its balance sheet. How else can the Fed buy treasuries though? We know they are monetizing the debt but at least by working through the primary dealers they can say they are not monetizing the debt.

There are three ways to grow nominal GDP

M (money supply) x V (velocity) = Q (output) x P (price inflation)

1 – Increase the money supply

2 – Increase the velocity of money

3 – Increase inflation

Let's use an example of a place called Fantasy Land (fitting for our current situation).

A farmer sells $50 in corn to a neighbor. The farmer then spends $30 to get their tractor fixed from another neighbor and spends $20 on a bottle of moonshine at the local "packy."

The GDP of this fine community is $100 assuming their is no inflation (hence the name Fantasy Land). Using the above formula we have:

Money Supply ($50) X Velocity (2, how many times the money was turned) = Inflation (0%) X Output ($100)

Getting back to Fantasy Land, excuse me the US economy, banks are not lending and people are not spending. There is NO demand, so there is no velocity. Money is not turning over. Small business surveys continually state that their top concern is not lack of credit, but rather lack of customers.

So the Fed must grow the monetary base (even though Banana Ben has said they are not creating money). Look at the two charts below of money supply and velocity. They have offset one another causing no real GDP growth, only nominal.

The Fed through QE is trying to make money so cheap it creates demand through inflation expectations (that car will be more expensive next month so I'll buy it today) and overall demand (I'll remodel that basement because Home Depot has zero interest rates for 18 months).

Problem is it's not working. Demand is not there. The Fed is hoping QE will raise stock prices, which obviously has worked and give people a sense of wealth, a desire to spend. It's also caused yield chasing and the use of massive leverage (leverage is now back to LEH levels which is truly astonishing).

Commodities have been a great trade and people have piled in. The result is rising input costs which cannot be passed along because there is no demand. As input costs rise margins are compressed. Expect higher layoffs as firms do all they can to manage the bottom line. Bernanke's efforts seems to be choking any demand left in the economy.

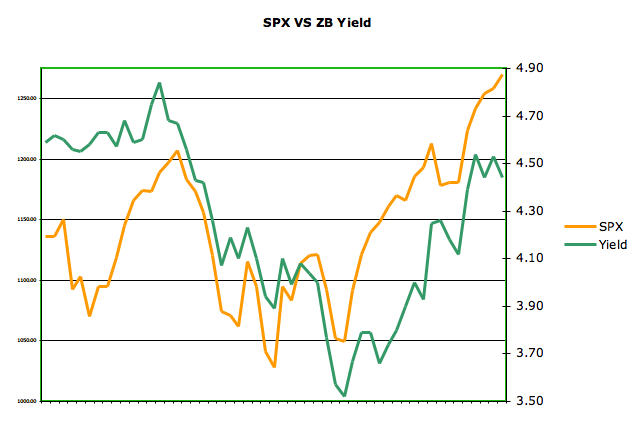

Input costs have risen, treasury yields have risen, gas at the pump has risen and now the USD has begun to catch a bid. The market looks forward to QE3 but honestly Banana Ben may not have the opportunity to see that happen. The debt ceiling will be reached in less than 8 weeks and in a recent survey 70% of Americans do not want it raised. Sure Congress can do what they want, they have done so for years. But, the last election has taught many that if they want to keep their jobs they better listen. The bond market may be telling them the credit card is stopped. We see what's happening in the municipal bond market.

A former Atlanta Fed President has publicly called out the Fed, their QE and their solvency. Dallas Fed President Fischer has also publicly cast his no vote for further QE beyond June.

Just recently two regional Fed manufacturing surveys were revised downward. QE is not working other than wealth effect which is not driving demand. Bernanke is not a dumb man. He lacks business sense for sure but at some point the Bernanke put will expire. To think the Fed will always be there is a clear sign group think is wrong again.

Submitted by Runedge. If you would like to follow my blog please visit - Ultra Trading