Slope of Hope Blog Posts

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

About Yesterday

Exporting Deflation

Three topics were dominating the news this morning: the Gates divorce, inflation, and the trade deficit.

I’ve got nothing to say about the Gates divorce, except that it’s shocking and saddening. I had always assumed their being a couple was eternal, but who knows what happened behind the scenes. I’ve got no chart for it.

As for the data news stories, I looked at our Economic Database for some charts. When I was growing up, inflation is all people thought about. Over the past thirty years, it had faded from the national conversation. Let’s just say I think it’s coming back in style and will be here for a long time to come.

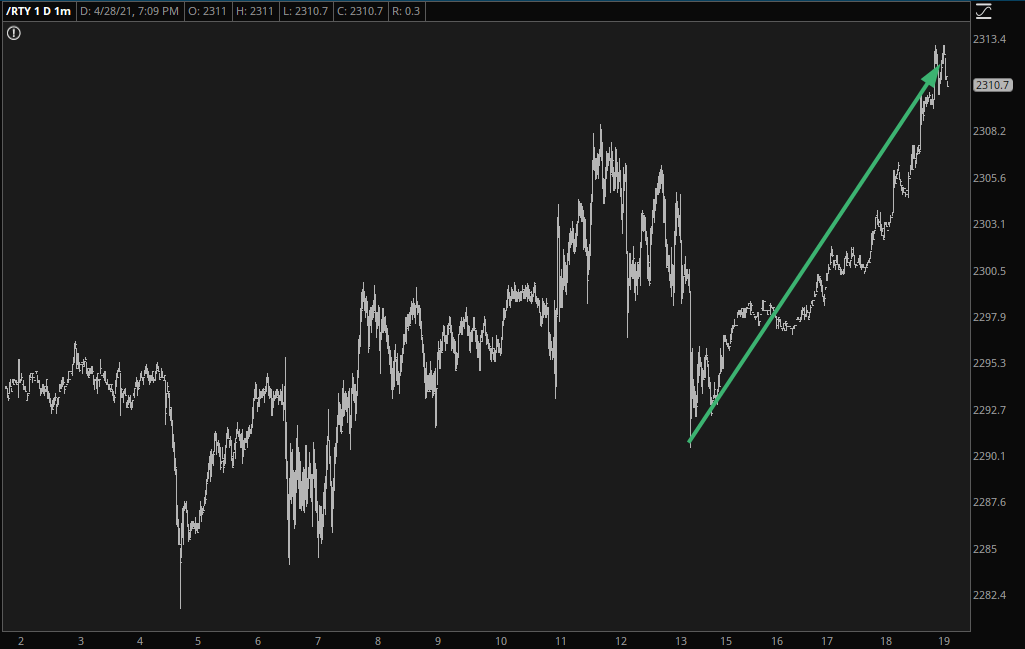

Stock of the Union

Well, it seems that the markets sure do like what the President is saying during his SOTU – – or at least are embracing the fact that asset inflation is going to continue to run wild. Here we see the small caps (/RTY) roaring higher:

An Inflationary Slingshot

Cost-push inflation could break out (and a note on gold)

Before beginning the post a little context is in order. We (NFTRH) anticipated the current pause in long-term Treasury yields (one indicator of inflation) because pro-inflation sentiment became over-done in March and was due for a cool down; so said a contrarian view. This post discussing the likelihood of more inflation to come is not written by a one-way bias booster. It’s important for credibility to make these distinctions from the herds running with the daily news cycle.

The short-term contrary sentiment situation against the inflation view began with the Bond King’s media-touted short of long-term Treasuries (i.e. expectation of higher yields), per one of our best macro tools…

(more…)