Originally published on TheTechTrader.com.

Slope of Hope Blog Posts

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

June Macro Update (by GoatMug)

I normally post my monthly fundamental updates on www.goatmug.blogspot.com but wanted to make sure that I shared these charts and thoughts as we push into the beginning of summer. As many know, I have suggested that summer would bring a significant correction as the grips of the deflationary forces embedded in the system really take hold. As central bankers attempt to remove stimuli or the efforts lose effectiveness, deflation will prevail. As things have played out, we seem from many fundamental points to be just coming out of the worst of things. Unfortunately what we are seeing is that the rate of change of improvement is falling and indicating that we might be headed directly toward that double dip recession many of us have trying to identify.

OIL SPILL – RECESSION WARNING FOR THE GULF COAST ECONOMY

Before plowing into the charts I wanted to make a comment about the oil spill fiasco. There is no doubt in my mind that BP royally fouled things up. Their mistake cost people their lives and has begun to damage our coastlines and fisheries. The economic survival of many along the Gulf Coast are in jeopardy as the disaster's impact is felt throughout the region. Fishermen, hotel owners, and restaurant owners have been hit the hardest and significant regions have not even had oil landfall yet.

In an effort to attempt to look like it is managing the situation, the government has mandated there will be a 6 month halt of exploratory drilling in the deep water of the Gulf of Mexico. Already, Chevron and Exxon have stopped two projects. The administration's steps to curb deep water offshore drilling and exploration projects will have the effect of doing what the 2008 recession could not do; sink the Texas economy. Houston and other Texas cities have survived the downturn much better than most. The impact of shuttering exploration won't just hurt the largest firms, but all of the small firms that consult and serve the majors. Ultimately we will again see the largest attack on small businesses that seem to always bear the brunt of the Obama administration's reactionary steps.

RAIL TRAFFIC- http://railfax.transmatch.com/

The last two weeks have begun to show a slowing of the growth and improvement in rail shipping tonnage. I like to examine rail tonnage because we can get a feel for where the economy might be headed. Year over year comparisons are now quite easy but it is the weekly rate of change I'm watching. Remember, it was the rate of change that was lauded in the "bull market recovery", let's keep watching the rate of change in the retest.

COMMERCIAL AND RESIDENTIAL BUILDING INDICATORS - (RAIL TONNAGE)

I like that Railfax breaks out these components (lumber and crushed stone) because they are the inputs for commercial and residential building. We have seen an increase in building permits for both types of construction, and the move up in crushed stone shipping does back this story up. Lumber doesn't tell the same story though, and therefore we need to continue to watch this. It is important to note too that lumber prices really took off earlier in the year and have corrected significantly.

LUMBER PRICING / LUMBER ETF – (CUT)

What is causing the softness in the lumber market? Lumber futures have fallen around 23% since April. Is softening demand for construction putting a damper on lumber and their rail shipments? Does a permit mean a real project?

http://futures.tradingcharts.com/chart/LU/W

I normally would put up a chart of the tonnage of one or two of the individual rail carriers, but none of them are showing out performance from each other or from recent weeks. Of course year over year comps are easy, but the recent moves up have stalled. This data has helped me make several low risk trades when combined with chart reading to find good entry points. I'm not seeing anything compelling from the fundamental perspective that makes me want to jump in.

FOOD STAMPS – SNAP PROGRAM 6.1.2010

The government just released it's SNAP details or the number of folks participating nationally in the food stamps program. The release adds the data for the month of March. There has been turn in food stamp recipients, in fact more than 40,150,000 of your friends are getting their milk, cheese, eggs, and other groceries courtesy of your tax dollars. The average family takes in $290 a month in assistance.

HOME SALES DATA – RELEASED TODAY FOR APRIL

The National Association of Realtors' index of pending home sales jumped 6% in April, beating estimates for growth of 5%. The jump in contracts is thought to be due to home buyers locking in the tax-payer give-away of money for home buyers as the tax scam expired April 30. Any guess we'll have a decline in sales over the next few months once this round of stimulus closes the contract process in June?

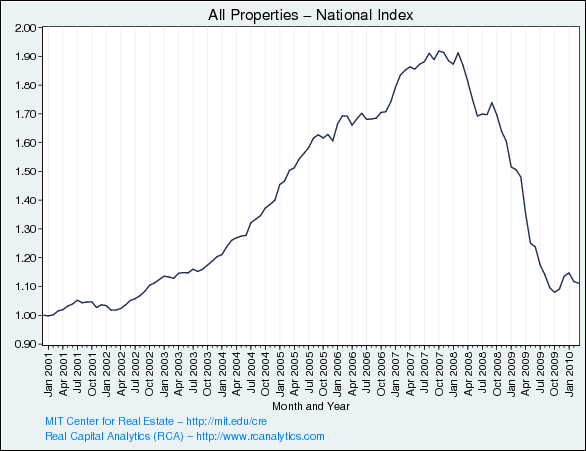

MIT CENTER FOR REAL ESTATE - MOODY'S / REAL COMMERCIAL PROPERTY PRICE INDEX

http://web.mit.edu/cre/research/credl/rca.html

Commercial property prices had a move up, but have resumed their drop. The strong dollar has put a stop to all of those foreign buyers rushing in to buy properties. Financing is also a bit tough to come buy as terms for deals include as much as 30% to 40% down. Deal mechanics don't look so good when leverage isn't so leveraged.

ECRI LEADING INDEX – GROWTH RATES – http://www.businesscycle.com/resources/

Weekly leading indicies from ECRI show a sharp decline in growth rates. As I've stated many times, the ECRI (WLI data) and the Bloomberg Financial Conditions Index are really subject to monetary liquidity measures and now stock market moves. How many times have I stated that the Fed realized several years ago that the stock market WAS the economy? Notice the acceleration of the decline of the growth in the last two weeks?

WLI DATA VS S&P 500 – http://www.businesscycle.com/resources/

I've graphed the WLI data here versus the S&P 500.

LONG TERM ROLLING 6 MONTH AVERAGE ECRI WLI DATA VS S&P 500

Here is a smoothed long-term version of the same data. WLI peaks indicate a recession. Before we jump to the conclusion that WLI levels around this 130 area indicate that markets will head south, be careful. The WLI stayed in this area and above for close to 5 years in the period from 2003 to 2008.

FINANCIAL CONDITIONS INDEX – BLOOMBERG – http://www.bloomberg.com/apps/quote?ticker=BFCIUS:IND

The Bloomberg Financial Conditions Index is another data point I watch. Levels above 0 show that the economy is in an expansion phase while points below 0 indicate we are in recession. May's reversal seems to tell us that we may have had a brief exit from recession but someone ordered a double dip of pain.

1 WEEK LIBOR – STILL TRADING AT 33 BPS ( http://www.homefinance.nl/ )

Does yesterday's 200 point gain make everything all better? Not according to 1 Week Libor. Bank stress levels remain high as compared to last month. We've seen a few days of little change as Europe and the ECB is attempting to stabilize the situation. LIBOR is the rate that banks lend to each other. In the absence of a rate hike, upward moves in LIBOR suggest there is anxiety in the financial system or liquidity issues.

USD - BLOOMBERG – http://www.bloomberg.com/apps/quote?ticker=DXY%3AIND

USD has continued its move higher and it took a breather today. I will write more in coming weeks about the real problems that the strong dollar, weak euro, and strong yuan are going to create for global trade and recovery. China is really going to suffer as the declining euro pressures Chinese manufacturers to cut their margins even more. China will absolutely not allow the yuan to appreciate no matter what they say publicly.

BALTIC DRY GOODS SHIPPING INDEX – http://www.bloomberg.com/apps/quote?ticker=BDIY%3AIND

Spot shipping rates continue to form higher highs and higher lows since the end of 2009. Despite the moves up in the index, shipping companies stock prices don't look as good. LEVERAGE KILLS.

COPPOCK INDICATOR – LONG TERM TURN INDICATOR – NOT GOOD FOR SHORT TERM

I have been playing around with indicators for quite a while and have looked at the Coppock Indicator for months. In truth, I had almost forgotten about it altogether and said that it was a poor indicator because it typically signals a turn well after a significant move. The indicator is really a 14 month average of index prices. As a turn approaches the rate of change slows. If the DOW closes lower than 10,000 in June, the indicator would have signaled a turn (yes I know the market has fallen 15%!). Obviously there can be false signals, but I include this in here just because it has highlighted areas to watch as price momentum turns for extended periods.

SHILLER DATA – P/E RATIOS vs LONG TERM INTEREST RATES – http://www.irrationalexuberance.com/

I wanted to include these two charts from the Irrational Exuberance website from Robert Shiller at Yale. Of importance here in the first chart is that P/E's start to rise when interest rates are declining. While we could have a crisis of confidence in debt and equity markets (really?) that might spur dropping long bond interest rates, we seem to be about as low as one might expect with some invisible hand intervening. What I'm getting at here is that we will not have much of a catalyst for rising P/E ratios in our current state because we've already had the boost from a drop in long bond rates. This "juice" came in the form of low rates in 2001 resulting from the 9/11 attacks and the subsequent Fed policy injections from the sub-prime meltdown.

SHILLER DATA – P/E RATIOS TO S&P 500

With that same context, we see that we have had a surge in P/E ratios and are back above the long term average. While we could see a move higher, from a fundamental perspective I don't know where we'll obtain the higher E's. Perhaps the higher P's will come courtesy of the FED's balance sheet?

WRAP UP –

I usually end the monthly post with a trading strategy to start the month off right. As you can tell from my comments I believe we are heading down through the end of the year. We've had a significant correction and are due for a move higher to attempt to retrace the loss of 12% from the highs. I've been posting that I would use that as a way to exit positions and get short. I think retail sales will be greater than expected and also the employment picture will show more upside surprises this week. These will be catalysts for a bounce. In my opinion the bounce may not last long though as now even good news is being met with selling which is a fundamental change from the last 14 months. Can you blame them either? Who wants to risk holding stocks over the weekend on the chance of a Greek or other sovereign default.

The fundamental data all tells me that the stimulative effects from the Fed and government are waning and the result is a decline in the growth rate or even drops in the actual reported metrics. A double dip of pain is in our future. CPI data releases are showing that inflation is muted, therefore all commodity related long trades need to be exited. I personally will avoid gold and silver until I see gold back at the $1050 range. I'd be negative on oil too, but with the geopolitical tensions in Korea and Iran, I will simply stay away from the trade.

A Heartbreaking Chart of Staggering Genius

At the risk of making a total ass of myself – – – which is endemic to doing this blog, I suppose – – I offer the following update to my world-famous WAG, originally posted on April 25th:

Whenever we see any weakness in the market, some Slopers have declared my WAG dead. Pish-posh! The WAG is alive and well.

What got me thinking about this was this post from my good friend Serge, the mercenary dictator of ETF Corner. He emailed me this particular image from the post which, on its surface, projects that the /ES will get back to about 1170 before turning down again. He has confirmed privately with me that we are right about at that dotted line now.

With the utmost respect to my Parisian friend, instead of being between "7" and "8", I think we're between "9" and "10". Observe my own labeling, lovingly crafted in the fine calligraphy you've all grown to respect and adore (as always, click on it to see a bigger version):

I've done two big things different than Serge. ONE, I've put in my own labeling, and TWO – – importantly – – I've taken into account the "X" factor. To explain:

"8" should have been a rocket launch to 1131, and "9" should have been an ease back to the neckline. Instead, "8" was completely limp-wristed, and "9" fell 21.25 points farther than it should have.

When I initially did this drawing, I used this absolute delta to project a target for "10" at 1150, but subsequent to this drawing, I used a percentage instead, and I came up with a target of 1143 instead. This just happens to correspond beautifully with the January high.

It also conforms with the entire WAG scenario beautifully, in addition to the Light That Guides Us All, which is my 1937-1942 analog.

The ideal scenario would be for us to shoot to 1143 (plus or minus a few points), stall, and then start falling. I think Serge's analog with China is brilliant, but with these two important modifications, I think the top before 2010's big plunge is much closer than he postulated.

Just In Case

Tomorrow morning, if the market reacts bullishly to the jobs report, I'd really prefer not to be caught with my pants around my ankles. It would make technical sense for the /ES to bust above 1107 and hit the target of 1140 (which we've all been anticipating for what seems like forever). I am long SPY with a position that represents a 1:4 long:short ratio in my portfolio, but it beats the heck out of 0:4 in case we have a rally.

Engage!

I don't do this very much anymore, but as a treat (or exploding cigar) for Slopers, here are the stocks I just shorted along with their stop prices. Current portfolio: 184 shorts; 0 longs. May the Great Ursa in the sky smile upon me tomorrow at 5:30 a.m. PST.

ACL………148.48

ADBE………35.41

AIV………22.06

ALV………53.32

AM………24.91

ARCC………14.10

BEXP………19.53

BPO………15.69

CBE………50.66

CEG………37.37

CHK………24.95

CHS………12.57

CLB………145.75

CMC………16.36

CMI………73.47

CNQ………37.26

CNQR………44.58

CNX………37.68

COG………37.45

CPHD………18.96

CYH………41.58

DLR………60.78

DVN………66.88

EIX………33.98

EQT………43.32

FST………30.04

HK………20.82

HP………43.53

IBM………132.00

INFY………59.98

JLL………81.28

KEG………10.96

KO………54.21

LINE………26.03

LTD………28.03

MED………34.60

MF………8.10

MIC………15.15

MON………52.55

MTB………81.87

NBR………21.41

NFLX………119.51

NG………7.46

PAL………3.71

PAY………21.61

PRAA………72.22

REXX………11.22

RSG………30.43

RTP………48.88

SAN………65.89

SSRI………18.66

SU………33.37

SWK………61.34

VCI………36.75

VLTR………25.01

VOD………20.65

WAT………71.70

WLL………89.13

WLT………78.52

XTEX………10.33