I don't have a PhD in Economics, and perhaps if I did, some of the oddities of modern economic policies, as practised by central bankers nowadays, wouldn't seems as strange.

One of those oddities is the strong superficial similarity between the policies of spendthrift governments printing money to cover deficits, in the manner that led to hyperinflationary meltdowns in Weimar Germany and Zimbabwe, and modern quantitative easing, where governments run large deficits to boost growth, selling bonds to cover the deficit, while for unrelated reasons their central banks create large quantities of money to buy bonds and thereby boost liquidity.

Equally the layman might think that if a policy isn't working, then it might be worth considering alternatives, while the PhD economist's trained mind and keen vision can see that initial failures are due to not pursuing the strategy vigorously enough, and that redoubling the effort will be sure to yield results.

I've also had it explained to me on more than one occasion that a sovereign government issuing debt in its own currency is always a good credit risk with little risk of default, for the reason that if their debt load becomes too great, they can simply issue more of their own currency to inflate their way out of trouble. I've suggested in the past that to the holders of their bonds, this might seem rather like a murderer making a distinction between shooting his victims in the head and strangling them, but again it seems my lack of economic training blinds me to the obvious distinction here.

I mention these today because there have been serious proposals made that the current Euro crisis could be resolved simply by allowing the ECB to create trillions of new money to buy debt issued by the PIIGS, and thereby eliminating the problem of the lack of demand for these sovereign bonds. An engagingly simple solution, but for the problem that like me, most of the German voters also don't have PhDs in economics, and so are therfore concerned by the apparent similarity between this policy, and the hyperinflationary policies that wiped out the middle class in Germany after WWI and indirectly led to Hitler coming to power a few years later.

In the absence of this magic bullet solution, the Euro zone clearly has a serious problem here with dodgy sovereign debt, and recent efforts to kick this problem further down the road don't appear to be working so far. What do the charts suggest here? Well the EURUSD chart doesn't look encouraging at all, with the obvious H&S that I pointed out yesterday morning having broken down and targeting the 1.275 to 1.28 area. Upside looks limited and downside looks very considerable and the assumption has to be sell the rips on EURUSD at the moment:

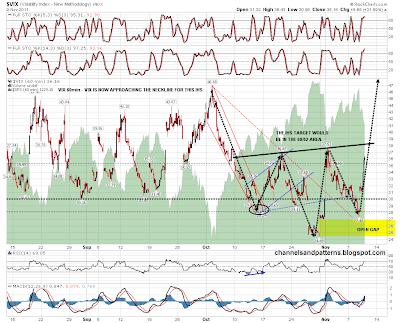

On Vix I've been posting the possible IHS forming there every day this week, and I was struck last night how closely the Vix move yesterday had tracked the arrow I put on the chart suggesting the possible path the Vix might take if the IHS were to complete and play out. If this IHS does complete and play out then the target is the 50/51 area, which would suggests that the October low might well be taken out. In the short term though the Vix on the daily chart reached the upper bollinger band yesterday, so we might well see it pull back today:

On ES the rising channel obviously broke yesterday, and the key resistance levels for any bounce today are now the daily 20 SMA (and middle bollinger band) at 1238.33 and the retest of broken channel support in the 1247-50 area.Worth noting as well is that there was a huge daily bearish engulfing candlestick on ES yesterday that suggests more downside and I've marked the initial downside targets on the chart:

What are other markets doing. Oil isn't highly correlated with equities at the moment but there is a correlation and the uptrend looks entirely intact there. After yesterday's initial drop oil even made a new high, and there's nothing happening on the bear side there until the rising channel breaks:

Copper and most other commodities excluding oil have only recovered weakly since the October low on SPX, and at the low yesterday have of those modest gains had been erased. Dr Copper is not therefore looking bullish here:

30yr Treasuries (ZB) broke up yesterday, but only to make a double top which has an ominous look for equity bears. I'll be watching what happens next closely:

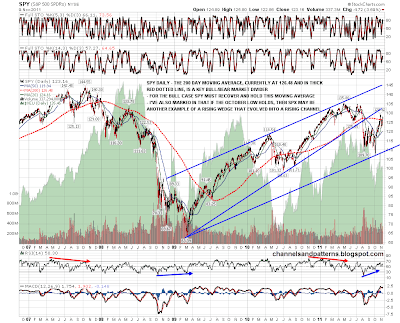

Last chart of the day is the 5 year SPY daily chart, showing the 200 SMA prominently . This moving average is a key dividing line between bull and bear markets and if the bear market is over then SPY needs to recover above this level and hold it. The drop yesterday was the second failure after a break up through this resistance level. If this level is recovered, and the 13/34 weekly EMAs cross back up, then technically it would be extremely likely that this year's bear market will be over:

Yesterday was a trend day, and the 38th largest one-day drop in history I read somewhere. I also read that 58% of the days following such drops closed up, and you'd normally see some consolidation after a trend day. Yesterday's range on ES was 1223.50 to 1249, and I'm expecting an inside day trading within that range today. That upper level fits with a retest of broken rising channel support on ES so I'd expect to see some stiff resistance there. A break above 1250 would look cautiously bullish and suggest that yesterday might just have been a flash in the pan, though the Euro crisis hasn't gone away, and I'm skeptical about any powerful moves up in the near future as a result.

Meanwhile the EURUSD and Vix charts suggest apocalypse soon on equities if the Euro crisis is not resolved quickly. Watch this space.