A model cosplaying as a fairy character from a video game for Nvidia at an electronics convention.

A Top Name In July

In mid-July, we wrote that Nvidia (NVDA) had hit our top ten names again, after periodically being a top name of ours going back to 2016. We titled that article, “In Case We’re Wrong About Nvidia“, because we included a hedge that would protect readers if we were wrong about it.

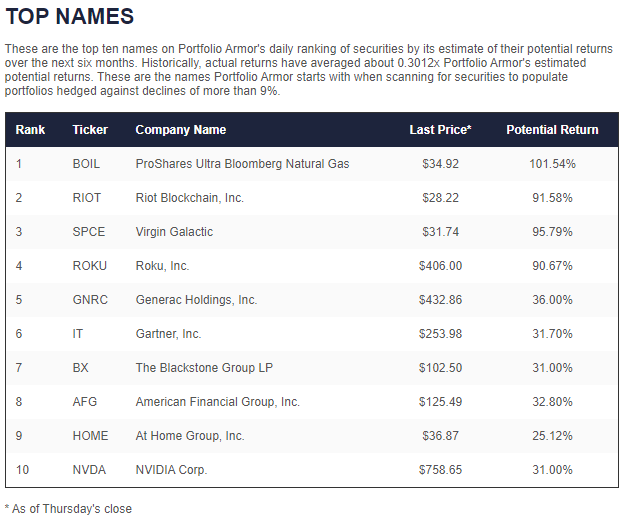

Screen capture via Portfolio Armor on 7/14/2021, one of a number of times Nvidia appeared in our top ten.

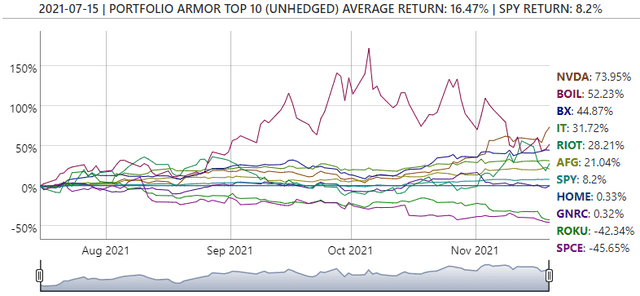

So far, it looks like we weren’t wrong about Nvidia. The stock hit an all time high on Thursday after posting record revenue in its third quarter, and then it hit another high on Friday. It’s now up nearly 74% since it hit our top names in mid-July.

A Top Name Again This Week

Nvidia was a top name of ours again on Thursday. As you can see in the chart above though, our top names don’t always do well. Both Roku (ROKU) and Virgin Galactic (SPCE) from our July 15th cohort are down more than 40% so far (though, on average, our top ten from July 15th are up 16.47% so far, more than double SPY’s 8.2% return over the same time frame). That’s why we continue to suggest hedging with our top names. Let’s look at a couple of ways of hedging Nvidia now if you’re long the stock or decide to buy it now.

Two Ways Of Hedging Nvidia

Uncapped Upside, Positive Cost

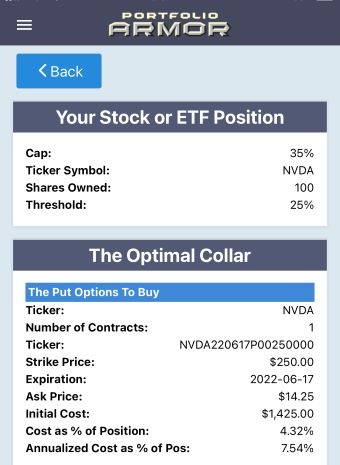

If you think Nvidia has a lot more upside over the next several months, you won’t want to cap its possible upside. As of Friday’s close, this was the optimal put option to protect against a greater-than-25% decline in Nvidia by mid-June, while not capping your possible upside at all.

This and the subsequent screen capture are via the Portfolio Armor iPhone app.

The cost of that protection was $1,945, or 5.9% of position value (calculated conservatively, at the ask; you could probably have paid a little less for this hedge by buying it at some price between the bid and ask).

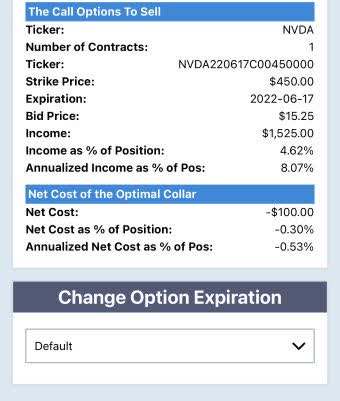

Capped Upside, Negative Cost

If you were willing to cap your possible upside at 35% over the next several months, this was the optimal collar to protect NVDA against a >25% decline over the same time frame.

Here, the cost was negative, meaning you would have collected a net credit of $100 when opening this hedge, assuming (to be conservative, again) that you placed both trades (buying the put and selling the call) at the worst ends of their respective spreads.