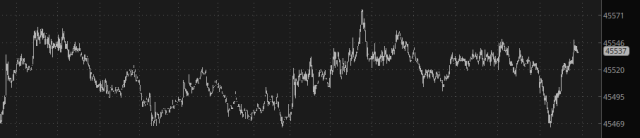

Good morning, and welcome to a new week. Nice as it would be to report something exciting, we remain in Meander Mode, with the /YM at this moment up 0.17%. it spent the entire night drifting around listlessly, doing next to nothing. Meh.

Longer-term, the year 2025 has been nothing but a gigantic “V”. This drop-then-surge actually ended way back in June, as the plunge and ascent mirrored each other almost perfectly. Since then, for months now, it’s been just a very-slowly-ascending grind fest.

Which, of course, has obliterated any dynamism or fear in the market.

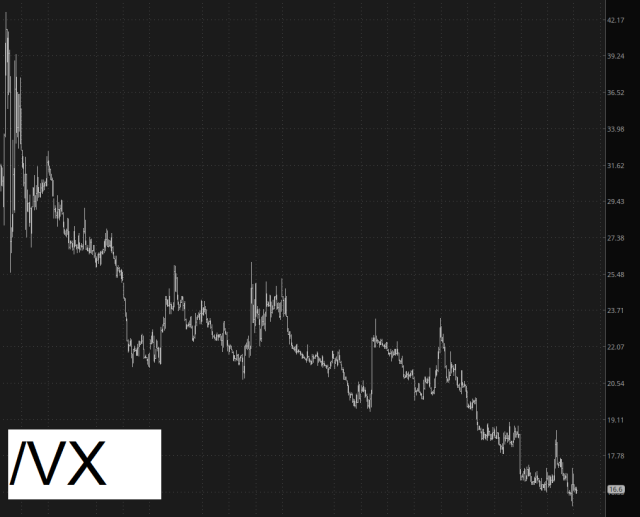

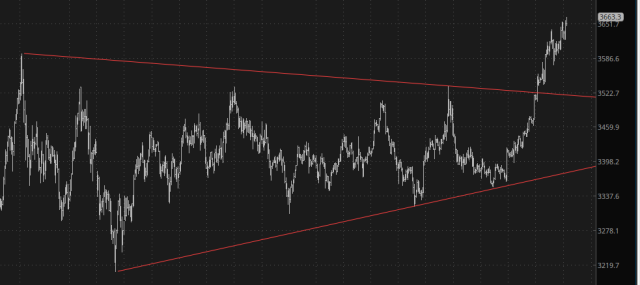

The overall theme of “bullish precious/bearish equities” continues to play out, at least on the numerator side of the equation, as gold continues to utterly outpace stocks, having completed this beautiful symmetric triangle formation.

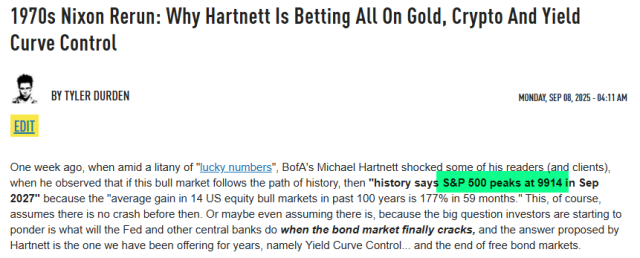

Speaking of which, I see the permabulls at Zerohedge are still permabulling. Months ago, they were trumpeting their favorite analyst (Hartnett from B of A) and his rather puzzling target of 6666 on the S&P since, honest to God, he felt it would make a nice bookend to the 666 bottom. Now that we’re only about 2% away from that target, he’s decided to sauce things up and change his target to 9914 (yes, this is the S&P 500 we’re talking about here) because that aligns with the average gains of past bull markets. Errrr, OK. I would counter that these are not “average” times we’re facing.

Setting that aside, the big event in this otherwise stultifyingly quiet week is the inflation data on Thursday morning. I’m not sure why the PPI and CPI seem to flip their order of reporting month to month, but irrespective of the reason, all eyes will be on the CPI in a few days.

I am entering the day medium-aggressive with no use of margin. Hopefully something will pop up this morning worth writing about!