There are a number of stocks out there which have lost MOST of their value and yet still represent good short positions. One of these, a current holding, is Owl Capital (OWL), which continues to sink below a massive topping pattern.

Slope initially began as a blog, so this is where most of the website’s content resides. Here we have tens of thousands of posts dating back over a decade. These are listed in reverse chronological order. Click on any category icon below to see posts tagged with that particular subject, or click on a word in the category cloud on the right side of the screen for more specific choices.

There are a number of stocks out there which have lost MOST of their value and yet still represent good short positions. One of these, a current holding, is Owl Capital (OWL), which continues to sink below a massive topping pattern.

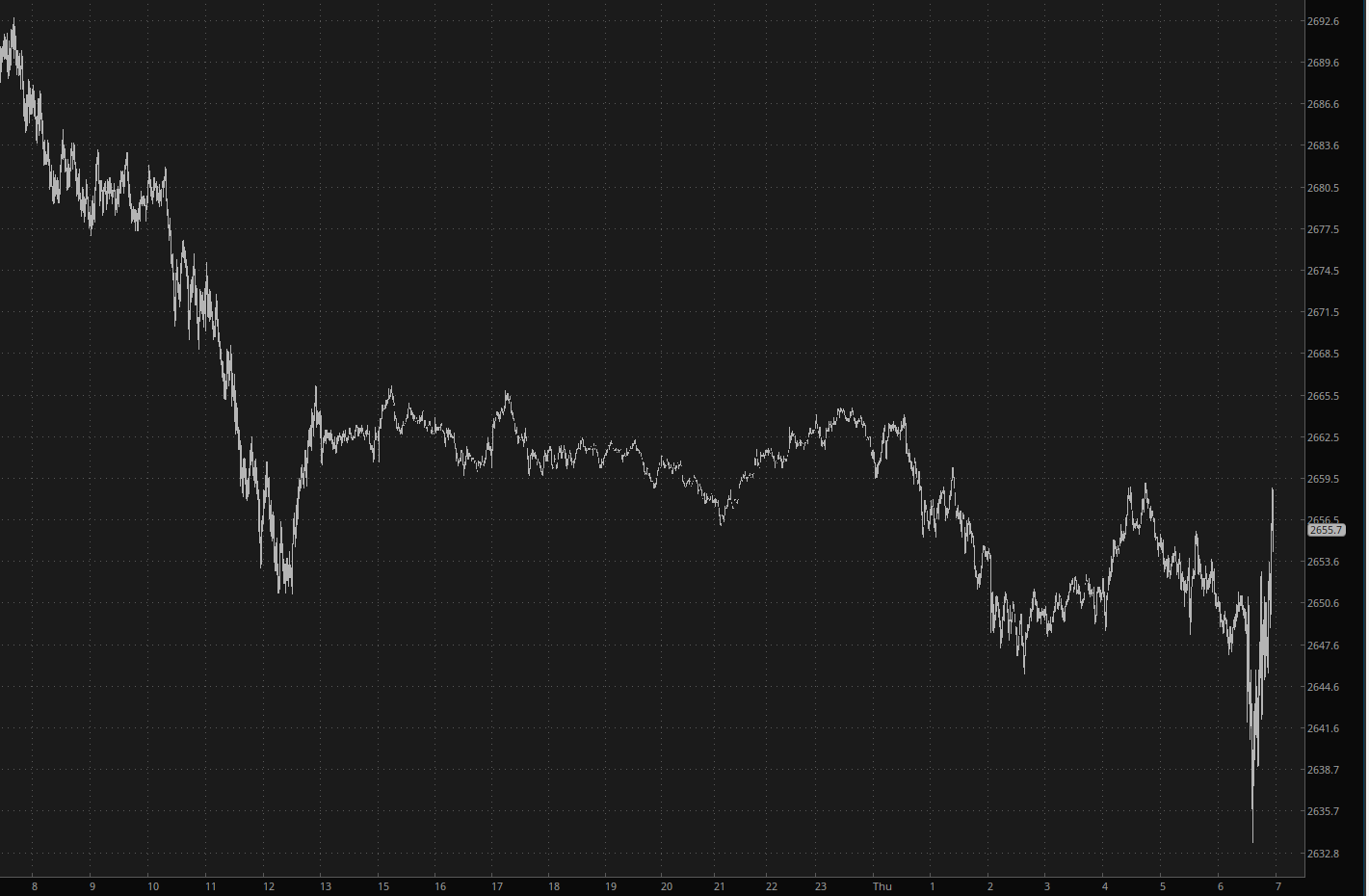

The bulls aren’t going to let their 17 yearlong always-go-up market go without a ferocious battle. Even on a minute-by-minute basis, we can see the counterattacks, such as the /RTY, below, which was slipping away nicely until it started getting gobbled up. As of this composition, all the big equity futures are still down, but by embarrassingly small amounts.

With the wipeout of Carvana taking place after hours, it got me to thinking about what other tradeable instruments exist because of a convicted felon’s efforts.