Volatility, Market Uncertainty, and the Case for an Iron Condor in Google

What Is an Iron Condor?

In today’s market, traders are constantly searching for an edge—something that thrives in uncertainty. The Iron Condor is exactly that kind of strategy. With implied volatility fluctuating, and mean reversion in play, is now an ideal time to deploy a high-probability, risk-defined options strategy like the Iron Condor in the tech-behemoth?

An Iron Condor is a market-neutral strategy that profits when a stock or ETF trades within a specific range. It consists of two credit spreads:

- Bear Call Spread: Selling a call option at a higher strike and buying another call option at an even higher strike.

- Bull Put Spread: Selling a put option at a lower strike and buying another put option at an even lower strike.

This creates a profit zone where the underlying stock can move up, down, or stay flat—as long as it remains within the defined range by expiration, traders collect the premium.

Step 1: Selecting GOOGL as the Ideal Underlying

Before placing any trade, ensure you are using a highly liquid stock with a strong options market. GOOGL is one of the most liquid names in the market, making it an excellent candidate for an Iron Condor.

✅ Why GOOGL?

- Tight bid-ask spreads for efficient trade execution.

- High daily volume and open interest in the options chain.

- Recent range-bound trading behavior, ideal for an Iron Condor setup.

Step 2: Assessing IV Rank & IV Percentile in GOOGL

One of the biggest advantages of an Iron Condor is its ability to capitalize on elevated implied volatility (IV). But how do we know when IV is high enough to make the trade worthwhile?

✅ IV Rank – Measures where the current implied volatility sits relative to its historical range. A high IV Rank (above 50) suggests IV is elevated, allowing traders to collect more premium.

✅ IV Percentile – Tells us how often IV has been lower than the current level over a set time frame. If IV Percentile is above 50%, options are more expensive relative to past levels.

Why This Matters for Iron Condors in GOOGL:

- When IV Rank and IV Percentile are high, option prices are inflated, meaning we can collect more premium for Iron Condors.

- As IV contracts, option prices drop, allowing us to buy back the position for a profit before expiration.

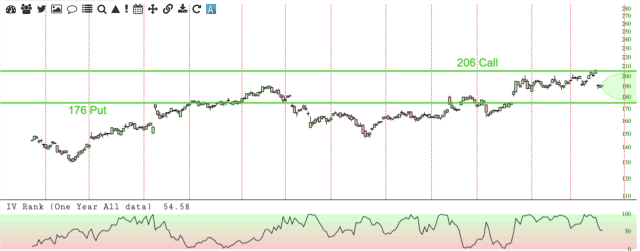

- Current Market Insight: GOOGL’s IV Rank is currently 54.5, and IV is slightly elevated making now a good time to sell premium with an Iron Condor.

Step 3: Understanding the Expected Move in GOOGL

With GOOGL closing at $190.95 today, the options market is pricing in an expected move of ±$15.00 over the next 43 days.

- This places the expected range between $206 and $176.

- We want to structure our Iron Condor outside this range to increase our probability of success.

Step 4: Structuring the GOOGL Iron Condor Trade

Bear Call Spread (Call Side of the Iron Condor)

- Sell the 210 call (just outside the expected range).

- Buy the 215 call to define risk.

- Probability of success: 85.29%

- Credit received for this leg: $0.48

Bull Put Spread (Put Side of the Iron Condor)

- Sell the 175 put (just outside the expected move).

- Buy the 170 put to define risk.

- Probability of success: 83.85%

- Credit received for this leg: $0.50

Total GOOGL Iron Condor Setup

- 📌 Total Credit Received: $0.98 per contract

- 📌 Max Risk: $4.02 per contract

- 📌 Probability of Success: ~84%

- 📌 Potential Return: 24.4%

By structuring the trade this way, GOOGL can move within a $15 range ($206–$176) without putting the trade at risk.

Step 5: Managing the Trade

Profit Target 🎯

- Close the trade at 50–75% of premium collected (i.e., buy back the condor at $0.45–$0.20 if initially sold for $0.98).

Risk Management Strategies:

- If GOOGL moves toward a short strike: Consider rolling the untested side to bring in more premium and reduce risk.

- Close the trade if losses reach 1–2x the original premium collected.

GOOGL Iron Condor: Quantitative Trade Breakdown

📈 Pros: Why This Trade Works

✅ Favorable IV Conditions: IV Rank (54.5) suggests inflated option prices, allowing for high premium collection.

✅ Defined Risk & High Probability (~84%): Capped loss at $4.02 vs. max profit $0.98, with a structure outside the expected move ($206–$176).

✅ Theta Decay Advantage: Time works in favor of the trade as long as GOOGL stays range-bound.

✅ Low Skew Risk: Balanced expected move reduces directional bias, making the setup ideal for non-trending conditions.

📉 Cons: Risks to Watch

⚠️ Poor Risk-Reward Ratio (~4:1): A single loss could erase 3–4 winning trades, requiring a consistently high win rate (~75%+).

⚠️ Directional Risk: A breakout beyond $206 or below $176 could lead to losses as short strikes go in the money.

⚠️ Vega (IV Expansion) Risk: If IV spikes instead of contracting, the position could temporarily lose value.

⚠️ Gamma Risk Near Expiration: If GOOGL nears a short strike close to expiry, P&L swings increase, making adjustments trickier.

📊 Verdict: A Solid Trade, But Needs Active Management

✅ Yes, if managed correctly.

- High probability and elevated IV provide a quantifiable edge.

- Risk-reward ratio is the main drawback, making tight risk control essential.

- Monitoring IV, delta, and gamma shifts is critical for mitigating potential losses.

🛠 Risk Management

🔹 Take profits early (50–75% of max premium).

🔹 Roll the untested side if GOOGL nears $206 or $176.

🔹 Watch IV trends—close early if IV Rank spikes beyond 60.

🔹 Adjust if delta of short strikes exceeds 0.35–0.40.

📩 Want More Options Trading Insights?

Subscribe to The Option Premium—your go-to free weekly newsletter for:

✅ Actionable trade strategies

✅ Step-by-step trade breakdowns

✅ Market insights for all conditions

🚀 Timing isn’t everything. Strategy is. Join now to trade smarter!