I read a lengthy piece (on /wsb, of all places) damning the entire quantum computing sector as an insane pipe dream and declaring that the white-hot companies in that space would all get wiped out. I asked good old grok to lay out what it considered the main risks in this field, and this is what it said:

Investing in quantum computing companies carries significant risks due to the field's nascent stage and technical complexity. Here are the top three risks:

- Technological Uncertainty and Slow Progress: Quantum computing is still in its early stages, with many technical hurdles to overcome, such as error rates, qubit stability, and scaling. There’s no guarantee that current approaches (e.g., superconducting qubits or trapped ions) will lead to commercially viable systems. Delays or failures in achieving practical quantum advantage could lead to prolonged losses or company failures, as seen with some early quantum startups.

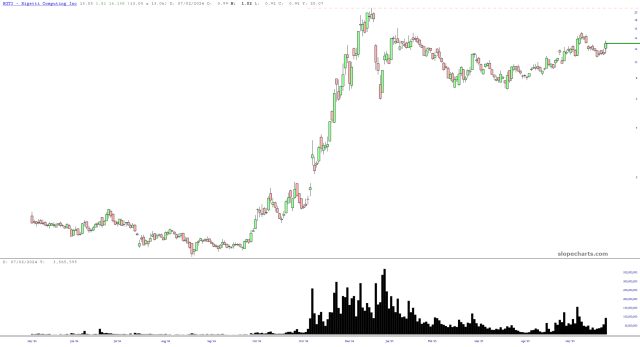

- High Capital Burn and Financial Instability: Developing quantum hardware and software requires massive investment in R&D, specialized facilities, and talent. Many companies, especially smaller startups, have high cash burn rates with limited revenue streams, as commercial applications remain years away. This increases the risk of insolvency or dilution of shareholder value through frequent fundraising, as evidenced by financial struggles of firms like Rigetti Computing.

- Market Competition and Consolidation: The quantum computing landscape is crowded with well-funded players, including tech giants (e.g., IBM, Google, Microsoft) and startups (e.g., IonQ, PsiQuantum). Intense competition could lead to a winner-takes-most scenario, where only a few companies dominate. Smaller or less differentiated firms risk being outpaced or acquired at unfavorable terms, reducing returns for investors.

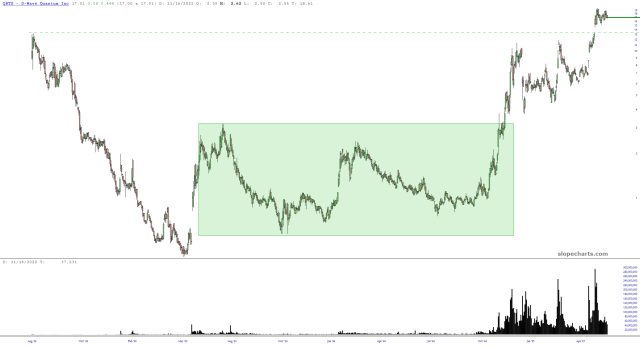

All the same, manias don’t care about facts, they can about buy orders, and at the moment, risks be damned, people are still tripping all over themselves to buy anything with the word “quantum” in it: