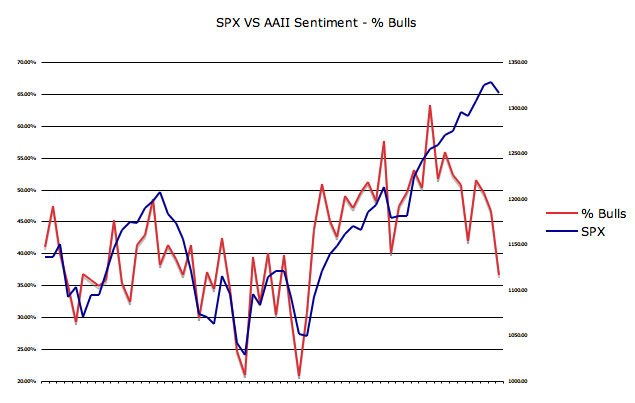

This week's Commitment Of Trader report has a few notable divergences but overall sends a somewhat mixed message on short term market direction.

Oil V Copper

The past few weeks copper has continued to show far greater strength than oil, setting new highs almost regularly. Oil appears to be rolling over and then another Middle East country erupts causing a spike, that is subsequently sold off. I present this chart below to simply show how the two have begun show a larger divergence than normal.

Copper V Commercial Net Positions

A few weeks back commercial net positions had become more net long indicating pending copper weakness, but that trend has changed. This chart would imply copper will continue to show more strength. The only note I would add is the chart of copper appears to be forming a top similar to April 2010. It is also notable that the net short position for commercial is reaching its prior highs.

Oil V Commercial Net Positions

A pretty large divergence is showing here. Oil is moving down while commercial net positions are increasingly net short. This is by far the highest net short position commercial traders have had in over a year. No real conclusion can be drawn from this chart.

SPX V Commercial Net Positions

Last week I pointed out the growing divergence between these two data points. It has continued to grow and based purely on the prior correlations would imply pending SPX weakness.

USD V Non Reporting Net Positions

Understanding USD direction has become almost impossible. In the face of geopolitical tension, the fear trade has not resulted in USD strength as in prior times. The only notable comment to draw from this chart is it appears non reporting positions are ahead of the price action in the USD. Since this group of traders is almost always wrong, continued USD weakness is quite possible. The USD is also setting up for another test of a multi year trend line.

30 Year Treasury V Commercial Net

Commercial net positions have continued their move towards net long implying further treasury weakness (higher yield) which would also support the technicals on the treasury price action of late.

Submitted by Ultra Trading. If you would like to read more, please visit - Ultra Trading