This is a multi-part series that looks at the derivatives market to help understand the systemic risk these products represent to the global economy. Unfortunately this problem was never resolved after the 2008 financial crisis. One day it will have to be addressed.

Wikipedia defines a derivative as:

"A financial instrument (or, more simply, an agreement between two parties) that has a value, based on the expected future price movements of the asset to which it is linked, called the underlying asset."

The most basic of derivatives would be the equity option such as a call. Using the definition above, the derivative, the call option, is an agreement between the buyer and seller of the option, whose value is based on the future price of the underlying asset in this case, equity. A 300 call option on AAPL is an agreement between a buyer and a seller and the value of the option is based on the price of the underlying asset, AAPL stock.

Although scary in name, such as an Interest Rate Derivative, the product itself is relatively straightforward as will be discussed in future posts. Derivatives are used for various reasons from speculation, increased leverage to arbitrage, but primarily as a hedge against risk. They serve an important role in the world of finance but like anything moderation is key.

Derivatives can be broken down into two categories:

OTC is where we will focus as this represents the greatest risk to the global economy. In the 2008 financial crisis, derivatives took center stage and became part of everyone's vocabulary. Unfortunately though, the 2008 financial crisis did very little to resolve inherent risks to the financial system. As you will see the size of this market is truly beyond comprehension.

Global GDP in 2008 was roughly $58 trillion USD.

The notional value of OTC derivatives is 12 times greater at $684 trillion USD

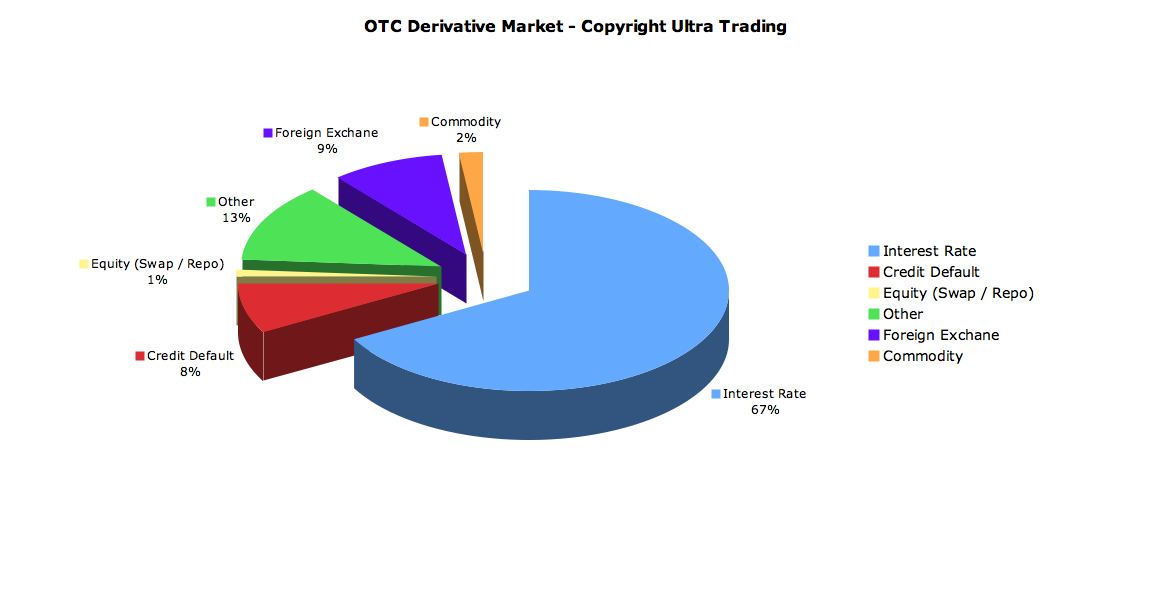

Interest Rate Derivatives are by far the largest of the OTC derivatives market

Imagine an unregulated product that is 12 times greater than the GDP of the world. Does that make any sense? Anyone who thinks we have moved past the problems of the 2008 financial meltdown is kidding themselves. This is a serious problem that must be understood, especially in a financial world where central banks have a heavy hand and whose actions often produce different results than intended.

In future posts we will discuss various derivative products in depth and the risk of each to the global economy.

Submitted by Ultra Trading. If you would like to read more, please visit - Ultra Trading

{kind=link}