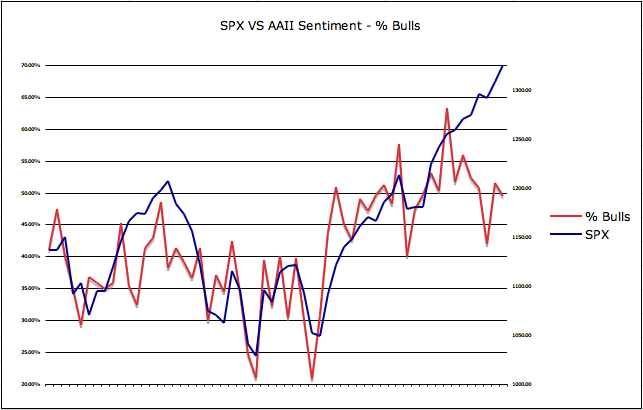

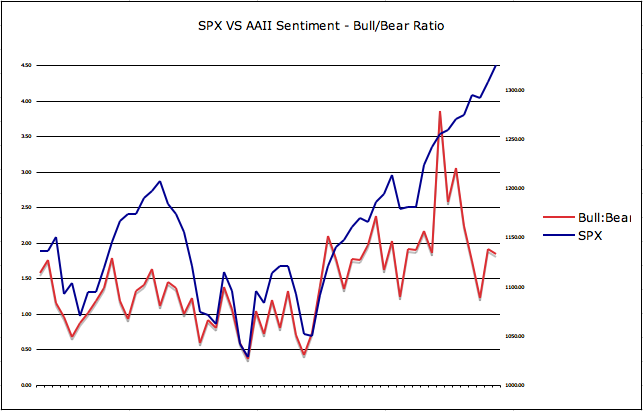

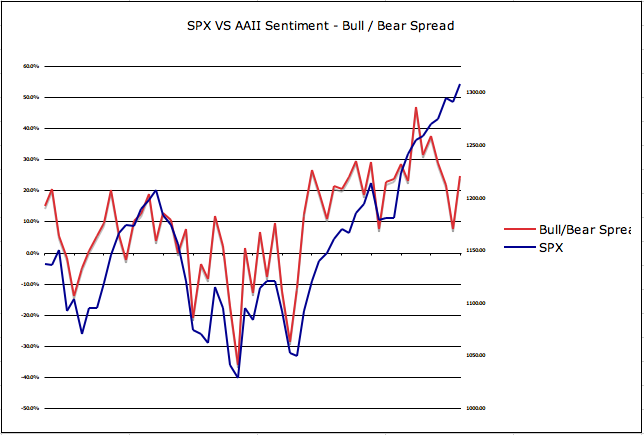

If you are a longer term trader and not a day trader then it is very important to stay focused on the issues facing the global economy. The issues are very real and have yet to be confronted in a serious manner, one that will achieve true resolution. In the day to day noise of ES futures or pundits that are all in and refuse to question their long trade it is very easy to get distracted and drawn into the power of group think. As investors we need to understand the environment in which we risk capital to determine how the risk and reward coexist. Sometimes this means missing powerful moves up as I personally have. Other times it means realizing that early to a trade is the same as being wrong, again as I personally have learned.

I continue to sit on hands until the following items are priced into this market for I feel these issues are very real and skew the risk reward equation far to the risk side.

EU Debt

Portugal 10 year yields are at 7.3% as of February 8 (7% is the threshold for the need for ECB / IMF support). Ireland has asked for an additional 40% in funding to support banks that are faced with an acceleration in deposit runs and reduction in credit quality. Italy is facing a leadership change as Berlusconi is now very likely to face charges for his sexual escapades. Recent reports have raised the question that Greece should default as their ability to repay their debt is growing impossible.

Global Unrest

Yesterday, Egypt saw its largest protest to date. Just when it appeared Egyptians were tiring, they were rejuvenated by the release and subsequent statement by a Google executive. Protests have spread to Saudi Arabia, Yemen, Syria, Jordan, Algeria and more. This movement is just getting started in my opinion.

QE

Bernanke is coming under greater pressure to cease QE2 in June and not commence QE3 thereafter. From rising bond yields, inflation concerns to growing internal dissent the case for QE3 is becoming more difficult.

China

This is a big question mark that should not be ignored. China has grown more hawkish in their monetary policy yet US markets have ignored this completely. China is trying to slow its real estate growth as its economy grows from one that is export driven to consumer driven.

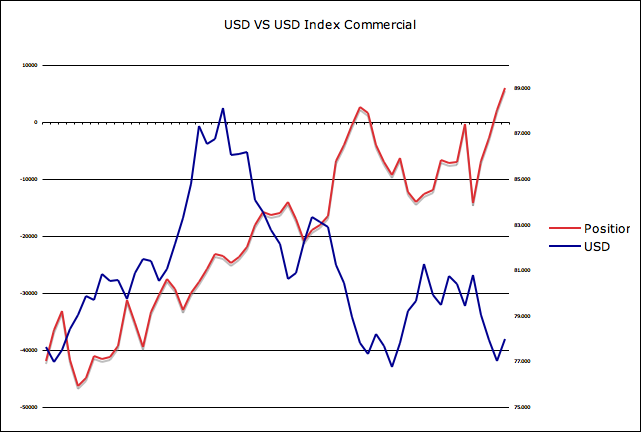

Currency

China, India, Russia and many others are increasing their precious metal reserves as they realize the day of the USD reserve status is diminishing and are now trading with non USD currencies. Charts of the USD look simply horrid and other than a two day bounce cannot reverse trend. Meanwhile with all the problems facing the EUR it has shown greater strength. So in the race to the bottom, the USD appears to be winning.

Asset Prices

Residential and commercial real estate have not bottomed as many pundits will lead us to believe. The levels of residential mortgage underwater are growing that will lead to further strategic defaults, thus higher levels of shadow inventory further pressuring home prices. A recent report from Fitch said that over 30% of commercial real estate that needs to be rolled in 2011 do not meet their standards. We have far more real estate than this economy and job market can support.

Unemployment

The job market is horrid. Regardless of the weather pattern behind a specific report the bottom line is the US has yet to create the minimum of 160,000 jobs needed each month to simply keep up with population growth. We have a structural problem in this country and it will not be solved by QE. 20% of income is in the form of a government transfer payment yet only 49% pay taxes. Meanwhile 1 in 7 Americans are on food stamps and this trend shows no sign of reversing.

I can go on with this list and more detail for each subject but the message is tiring. This market can stay elevated for another hour, another week, another few years. No one knows. Many have learned not to stand in front of this market but as investors its important to understand the issues that surround us aside from the noise. We must be ready to act when the market begins to price in the above items. It is human nature to ignore problems we are faced with. That is exactly what is occurring right now among our leaders. That will not cause them to go away but only grow.

Submitted by Ultra Trading. If you would like to read more, please visit - Ultra Trading