The tone on Friday was largely set by the resignation of Jurgen Stark from the ECB, the second German to resign this year after Axel Weber, previously widely tipped to have been the next head of the ECB, resigned in February. Jurgen Stark's resignation was ostensibly 'for personal reasons' but it is widely assumed that the resignation of both germans was primarily due to disagreement with ECB policy, and Jurgen Stark's resignation in particular to be in protest at the ECB's recent decision to start buying Italian and Spanish bonds.

This matters a lot in Euroland, as without Germany, the Euro area is mainly composed of spendthrift socialist basket cases, with rigid economies and excessive taxation and spending. For anyone who feels I am being unduly harsh on socialist governments let us consider the case of (non-Euro) Britain, which was ranked the fifth most competitive country in the world on tax when the Labour Party came to power in 1997. A survey since they fell from power in 2010 now ranks the UK at 94th out of 142 countries, between Swaziland and Lesotho, and the greatly increased revenues from all those extra taxes are nowhere near enough to balance the budget, as spending increased even more massively than taxes during the 13 wasted years of Labour Party rule.

As Margaret Thatcher famously said, 'the trouble with socialism is that eventually you run out of other people's money'. Socialists describe themselves as progressive, but to my eye their main shared characteristics are that they are hostile to the markets that support every Western economy, tax and spend far too much with an underlying attitude that those with savings need to be punished, run public services for the benefit of their union paymasters rather than the service users, and encourage welfare dependency that corrodes the social fabric that they claim to care so much about. Not much progressive about that to my eye. (Editor's note: amen!)

The point for this morning though is that the cosy half-truths and understandings that underpin the Euro area are in real trouble, and the Germans are increasingly uncomfortable with the widely held idea that they will have to act as guarantor for the countries in the Euro area that are flirting with bankruptcy. EURUSD has not bounced at the obvious reversal area overnight and might be setting up to have another very bad week. That would be bearish for equities:

As for equities SPX held my rising channel on Friday, and if ES recovers sufficiently by the open, might well bounce from here:

ES has fallen overnight,but has now established the lower trendline of a rising channel there as well. Any lower than the overnight low would obviously be bearish but as long as that trendline holds then we might well see a strong bounce from here:

SPX and ES are therefore balanced at a major cusp today, but they're not alone. Vix has now established a strong declining resistance trendline from the early August high and we saw a fourth touch of that resistance trendline on Friday. A break above resistance would obviously be very bearish for equities:

Copper hasn't done much of interest over the last few weeks but it has finally hit the rising support trendline from late 2008 overnight and is sitting on that at the time of writing. If that trendline breaks that will look very bearish for both copper and equities:

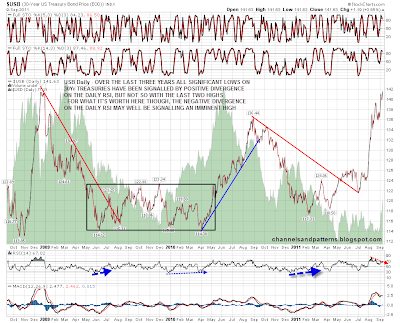

There is one thing that looks as though it might be bullish for equities this morning and that is the USB (30yr treasuries) daily chart. USB generally shows some positive RSI divergence at major lows, but there has been no negative RSI divergence at the last two highs. For what it's worth this time there is marked and growing negative RSI divergence on the daily chart at the moment, and this could be signalling a major high for treasuries. Historically that wouldn't generally mark a low on equities, but it would suggest that such a low might arrive soon:

Short term the key things to watch for equities are the channel support trendlines on SPX and ES and the declining resistance trendline on the Vix. If those trendlines break then I would expect the bear flag on the SPX daily chart that I posted on Friday to start playing out to an initial target in the 1040-50 SPX area, but ultimately towards the key 1000 support area.

One last comment to make is that I've been reading a lot about how cheap equities are in terms of corporate earnings. Corporate profits are very high but I think there is something to consider here in terms of why that might be. Obviously the world is still working its way through a massive debt crisis, and one main response to that crisis has been to cut interest rates to well below zero in real terms.

In effect that is a tax on savers of 100% or more of the interest that they would expect to earn in normal times, and the receipts of that tax are a subsidy to borrowers, who pay far less interest than they should normally expect to on their borrowings. One major section of borrowers is corporate borrowers and their subsidy from this confiscatory tax on savers shows up in increased corporate profits, which is one key reason why corporate profits have risen strongly in recent years even though US GDP has yet to recover to the 2007/8 highs.

How sustainable are those profits in that case? Not particularly, and at some point corporate profits, currently at a major high in relation to GDP, should revert back towards the (far lower) long term mean. Corporate earnings are therefore not currently an ideal way of weighing the cheapness of equities, and in any case even now P/E ratios are well above the lows seen at major secular market lows in the past.