The markets have lost much of their glossy sparkle during the past one-year period, both globally and in the U.S, and are in need of a major "touchup."

Further to my last weekly market update, this week's update will take a look at global and domestic markets to assess strength vs. weakness in each group during the past one-year period, as well as the past week.

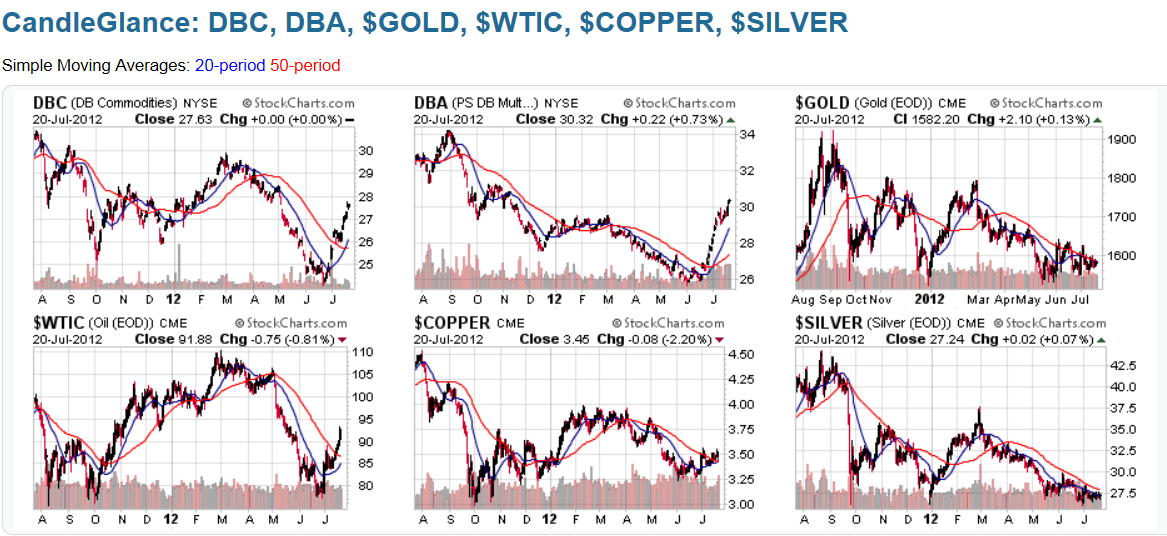

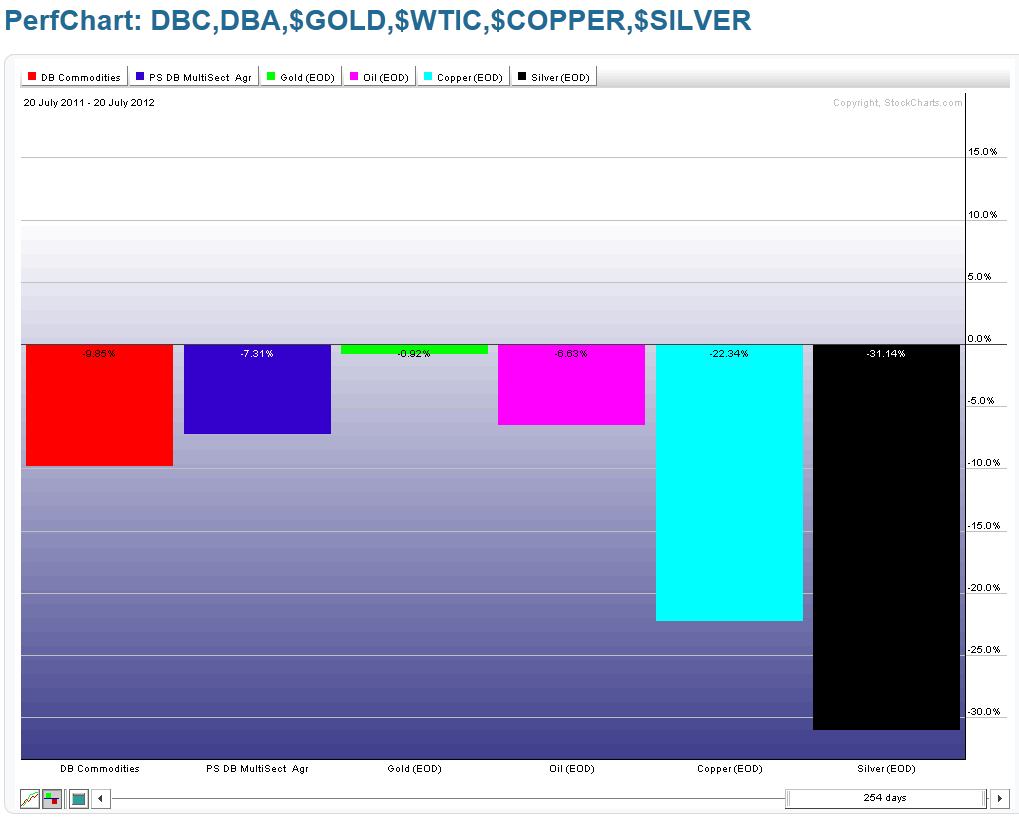

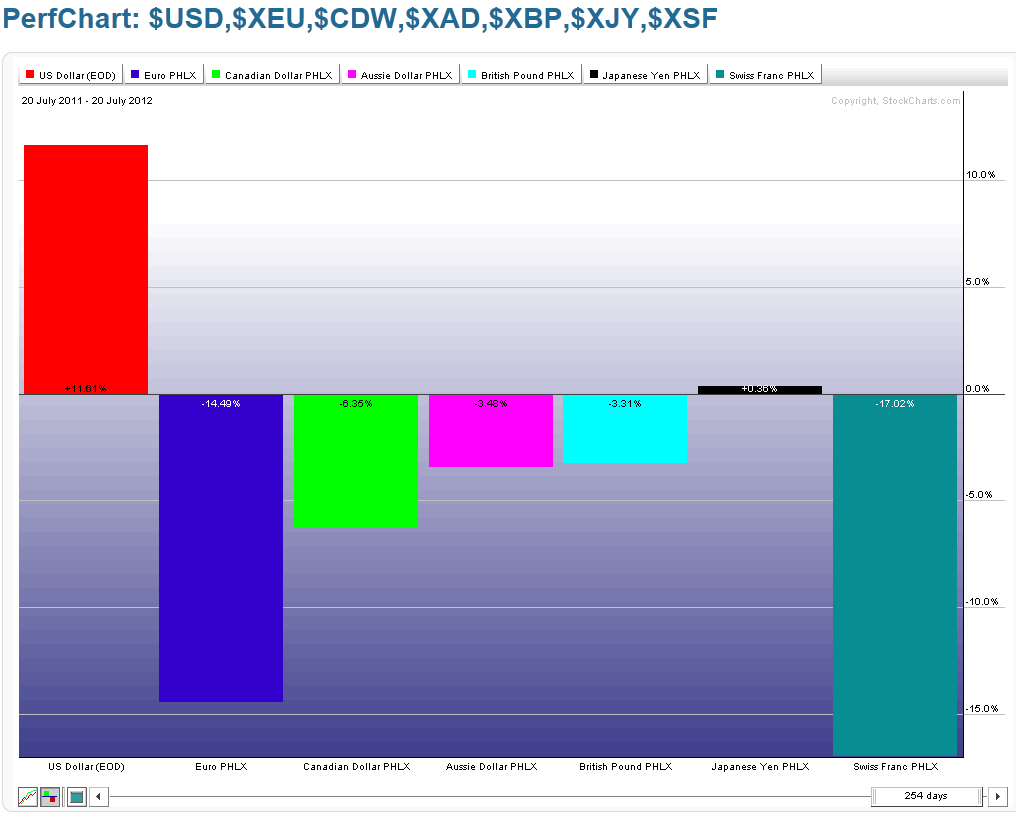

Below are a series of one-year Daily charts, graphs depicting money flow for a one-year period, as well as graphs depicting money flow for the past week, together with general commentary on each grouping.

Group 1 features the U.S. Major Indices. You can see from the chart and the first graph that the Utilities Index is leading in strength for the one-year period, while the Nasdaq 100 Index took over the lead during this past week. The laggards for the year, and for the past week, are the Russell 2000 and Dow Transports Indices.

Group 2 features the 9 U.S. Major Sectors. The overall Sector leaders for the one-year period are Utilities, Consumer Staples, and Health Care (the defensive sectors), while Energy, Materials, and Technology gained the most during the past week. The laggards for the year are Financials, Energy, Materials, and Industrials…and for the week are Financials and Consumer Staples.

Group 3 features Germany and France, as well as the PIIGS countries (Portugal, Italy, Ireland, Greece, and Spain). The only country to have gained during the one-year period is Ireland, while there were some minor gains in Greece, Germany, Ireland, and France during the past week. The biggest loser during the past year is Greece, followed by Spain, Italy, Portugal, France, and Germany…and during the past week is Spain, followed by Italy, and Portugal.

Group 4 features the Emerging Markets Sector (EEM) and the BRIC countries (Brazil, Russia, India, and China). None of the countries nor EEM have made any gains during the one-year period, while Russia and EEM made some gains during the past week. The biggest loser for the year is Russia, followed by China, EEM, Brazil, and India…and for the past week is China, followed by India, and Brazil.

Group 5 features the Canadian ($TSX), Japanese ($NIKK), and World Indices. All of these three are lower than they were one year ago, while gains were made in the World Index and Canada during the past week. The biggest loser during the past year is the World Index, followed by Japan, and Canada…and for the past week is Japan.

In summary, the markets have been playing defensively over the past one-year period, with the majority of the money flowing into the U.S. $, Utilities, Consumer Staples, Health Care, Nasdaq 100 Index, S&P 500 Index, and Dow 30 Index. Hardest hit during the past year have been Europe, the PIIGS, the BRIC countries and EEM, Silver, Copper, the Swiss Franc, the Euro, Japan, Canada, the Russell 2000 Index, and Dow Transports Index. As such, there has been more weakness, world-wide, than strength during the past year. The one-year leaders are the ones to watch to see if this relative strength continues, or if they begin to weaken.