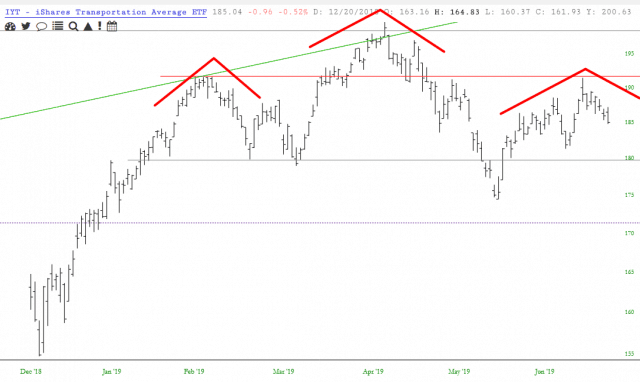

I have a couple of technical study sets called Max Sensitivity and Min Sensitivity. As you might guess, the “max” one tends to be very volatile. I was curious, however, since my belief is that banks are weakening, how the “min” study set looked with a couple of major financial funds. Here is XLF: