The Tesla roadster Elon Musk launched into space (photo via Newsweek).

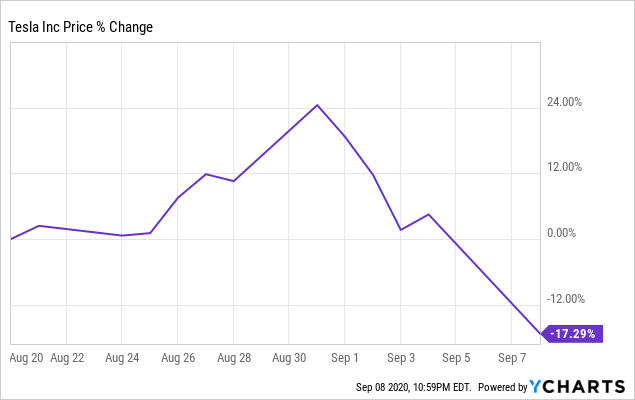

Softening The Blow On Tesla’s Worst-Ever Day

Peter Lynch once wrote that investors who make extraordinary gains from stocks usually have some emotional connection to the company that keeps them invested. Jason DeBolt appears to have that sort of emotional connection to Tesla (TSLA), which enabled him to hold on to his shares despite them sinking more than 20% on Tuesday.

For less emotionally invested Tesla longs, hedging came in handy this week. A couple of weeks ago, I wrote that it was time to hedge Tesla again. In that piece, I included this video, showing that, although Tesla was too expensive to hedge with puts over the next several months, it wasn’t too expensive to hedge over the same time frame with an optimal collar.

Shares of Tesla dropped more than 17% from the time I wrote that to Tuesday’s close.

Let’s look at how the hedge ameliorated that slide and briefly discuss courses of action for hedged Tesla longs now.

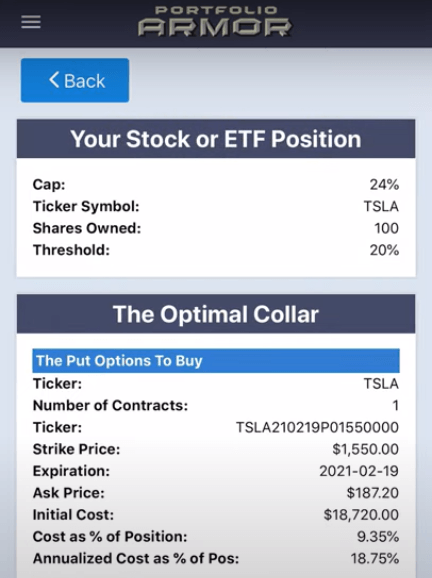

The August Optimal Collar Hedge

On August 20th, this was the optimal collar to protect against a >20% drop in TSLA by February 19th, 2021, while not capping your possible upside at less than 24% by then.

Screen capture via Portfolio Armor.

In this case, the net cost of the hedge was negative, meaning you would have collected a $5,330 net credit. That assumed, to be conservative, that you bought the puts and sold the calls at the worst ends of their respective spreads.

How That Optimal Collar Hedge Reacted

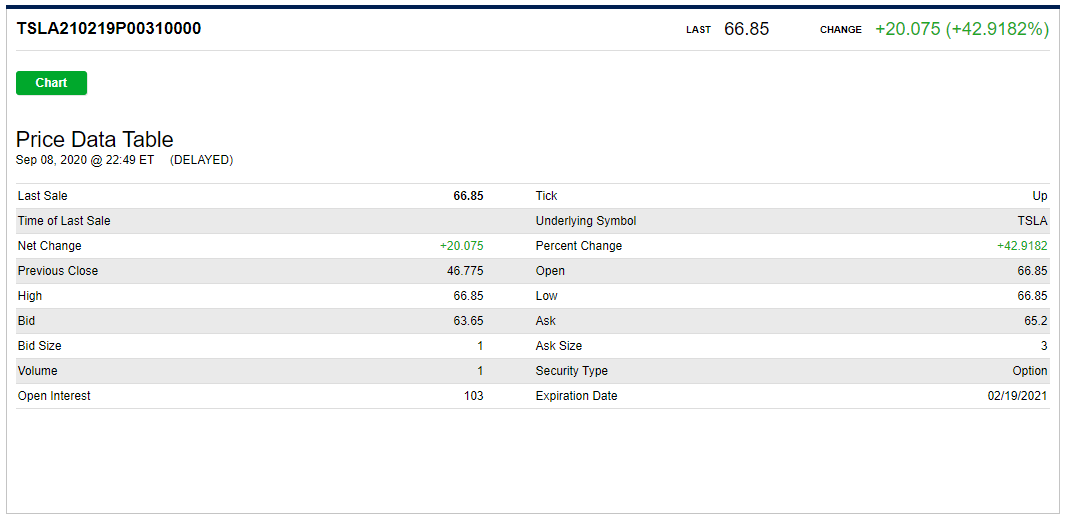

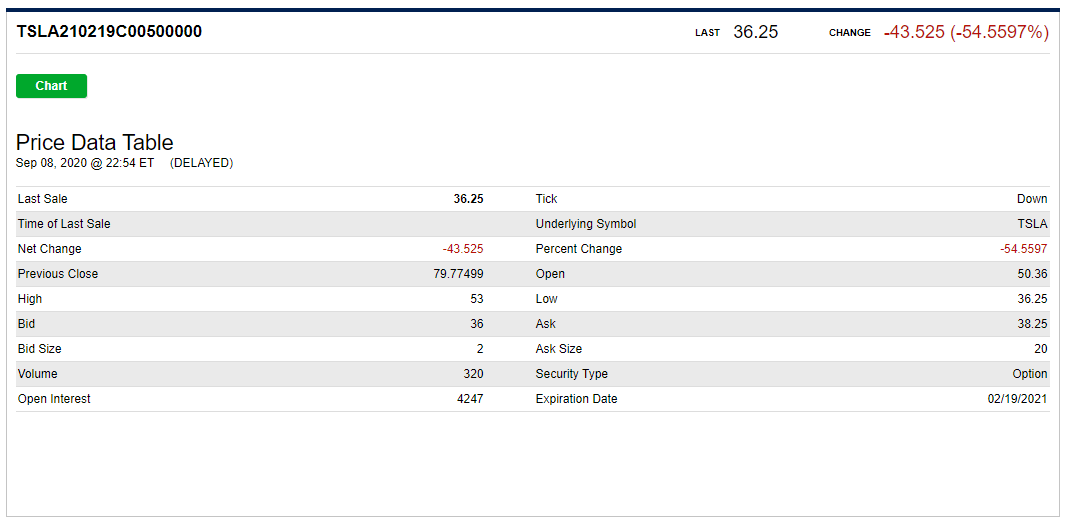

Recall that Tesla had a 5-for-1 split at the beginning of September. So if you hedged with the collar above, your one contract of $1,550 Tesla puts expiring in February would have converted to five contracts with a $310 strike, and your one contract of $2,500 strike short calls at the same expiration would have converted to five $500 strike calls. With that in mind, here’s a quote on the put leg of the collar as of Tuesday’s close.

And here’s an updated quote on the call leg:

How That Hedge Ameliorated Tesla’s Drop

Tesla closed at a split-adjusted $400.37 on August 20th. A shareholder who owned 500 split-adjusted shares of it and hedged with the collar above then had $200,185 in TSLA shares, $18,720 in puts, and if the investor wanted to buy-to-close the short call position, it would have cost him $24,050. So, the net position value on August 20th was ($200,185+ $18,720) – $24,050 = $194,855.

After TSLA closed at $330.21 on Tuesday, September 8th, the investor’s shares were worth $165,105, the put options were worth $32,212.50, and it would have cost $18,562.50 to buy-to-close his calls, using the midpoint of the spread in both cases. So: ($165,105 + $32,212.50) – $18,562.50 = $178,756 (rounding up that last 50 cents). $178,756 represents a 8.26% drop from $194,855.

More Protection Than Promised

Although Tesla had dropped by about 17.29% from August 20th to September 8th and the hedge was designed to protect against a >20% drop, the optimal collar hedged position was down 8.26%. The time value of the put options gave a bit more protection than promised since the hedge was structured to protect based on intrinsic value alone.

After Wednesday’s Partial Rebound: What Now?

That’s up to you, and it will depend in part about your view of Tesla’s prospects from here (my guess is Tesla will be trading at a higher price when this hedge expires). The nice thing about being hedged, though, is that it gives you options (no pun intended). You don’t have to worry so much about how much further Tesla might drop because your downside is strictly limited. So you can exit now, for a smaller loss; you can buy-to-close the call leg of your collar to remove your upside cap if you’re bullish; and if you’re even more bullish, you can sell your appreciated puts and buy more Tesla shares. In any case, you have breathing space to let the dust settle and decide on your best course of action, without the anxiety of an unhedged investor.