Those of you who use the real estate site zillow.com may know that you can “save” your real estate properties and track them over time. Our family has a number of apartment buildings, but those valuations are hard to pin down and thus not on Zillow. Our homes, however, are, and it’s interesting to see the changes that have taken place recently.

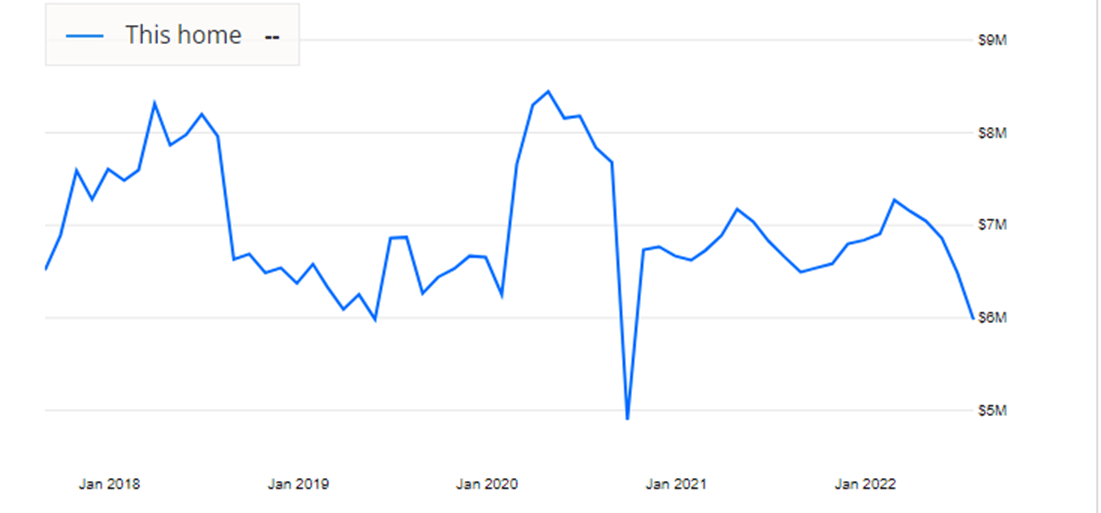

The most dramatic one is in my fair city of Palo Alto. Ostensibly, home sweet home has wildly swung between $6 million and $9 million, even over recent history. I personally find it hard to believe that the swings are anything this crazy, and maybe that’s why Zillow got totally torched with their own real estate portfolio, since the data is kind of spasmodic. Since we’ve lived here for over thirty years, and bought the place dirt cheap, I don’t really care, but those who bought at the top – – God help ’em.

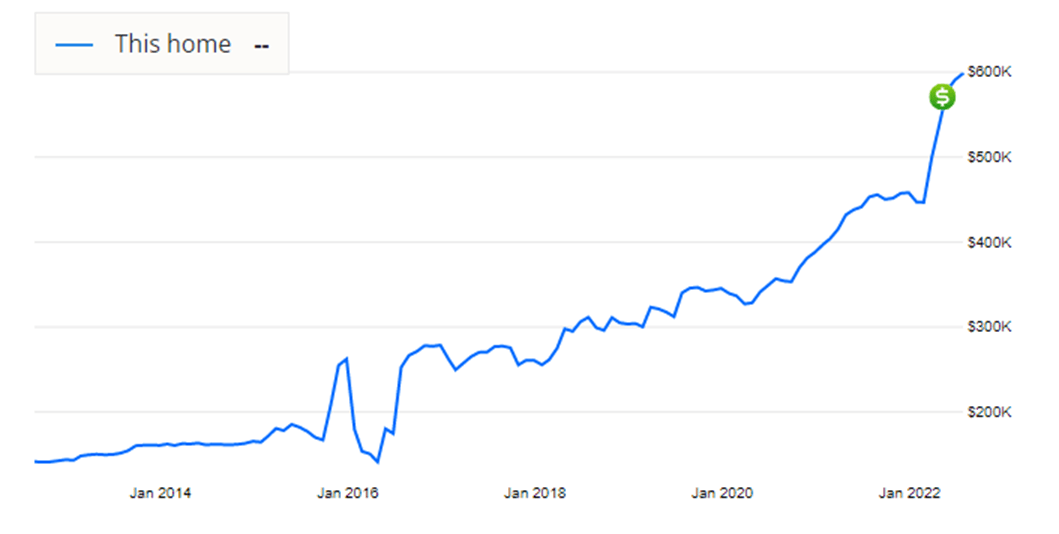

San Mateo, which is a very nice city but not as fancy-pants as Palo Alto, has a more “steady as she goes‘ kind of valuation. This is a rental home we have up there which, yes, has dripped recently, but at least hasn’t offered up a $3 million wipeout to the family balance sheet.

The most recent, and cheapest, property was purchased in North Carolina, which at the time I fully embraced we were overpaying for, since there was an absolutely mayhem of frantic buyers over the past year. Meh. It’ll all come out in the wash. This is where Bear Force One is going to take me on the 17th.

These valuations are, of course, largely dependent upon interest rates, because homes are nothing more than bonds where you are allowed to live. As you can see below, interest rates have had a very tiny uptick in recent months, if you look very closely, which is throwing kerosene on insane valuations like those that used to be in the Silicon Valley and, I suppose, are very prone to a hard fall.