Note: This is not market analysis. This is a person writing words and inserting some funny pictures. It is a product of said person’s view of psychology and the modern market.

First off, my honest self-evaluation: I would be pleased to see the US stock market to go down again, not because I am positioned for it (I am not, yet, other than through fairly non-dramatic risk management like portfolio balancing, profit taking and keeping high cash levels as appropriate) but because I feel like the bull was cooked up by an evil man named Ben Bernanke.

When I write “the bull” I am not talking about the post-Christmas Eve rally. That had to happen and at the time I was buying the spiking fear and panic. I am talking about the post-2008 bull market.

Regarding Bernanke, evil is probably too strong a word but I consider the effects of his policy to have been purely evil, exponentially enriching the already rich and driving the middle class to the verge of… electing an American TV character who says the right things to those who want, no need to hear those right things after the Bernanke years of abuse (ironically, with the distribution to the rich taking place under a president thought of as a socialist redistributor… only in America).

I don’t just feel like the bull was cooked up, I know it. I was there in real time as the 2003-2008 inflation failed into the epic crash it deserved and the Bernanke Fed began to clean up what the Greenspan Fed had inflicted upon the system during the previous inflation cycle. That evil man was a purveyor but this evil man took monetary manipulation out from behind Greenspan’s curtain…

…and brought it right to the front page in a stroke of evil genius.

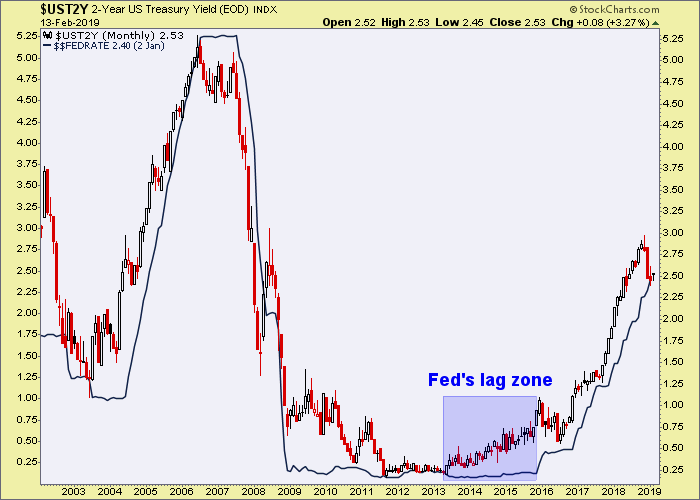

He jimmied the macro by artificially pinning the Fed Funds rate to zero for years, and then let it dwell more years (under Bernanke and Yellen) after the 2yr Treasury yield had given a signal that it was time to raise rates.

But no, the evil man (and woman) kept this pedal to the metal along with the ongoing benefits of QEs 1-3 and the crowning achievement, Operation Twist (which is the gift that keeps on giving to this very day as the 10yr-2yr yield curve remains in a flattening trend). Saving – an important aspect of a real economy – continued to be outlawed by decree of ZIRP for 2+ years after the 2 year yield turned up.

If you inspect the dynamics of Op/Twist a curve flattening was the implied goal. The racket was simple; the Fed sells short-term Treasury bonds (like the 2yr) and buys long-term Treasury bonds (like the 10yr), erasing what were at the time ramping inflation signals (recall the long-term Treasury yield spike and inflation blow out of Q1 2011). With an interruption in 2012 into 2013 the yield curve has been pummeled ever since.

Here is the Continuum of contained Treasury yields showing that 2011 event as just another failed breakout along the historical journey of a well managed bond market.

And here is the yield curve, declining (flattening) with the ongoing boom. Nothing to see here folks; move along, okay?

Much of what I’ve written above is emotional. It pisses me off that powerful people can manipulate markets (Greenspan, Bernanke) and others can attempt to manipulate markets (Trump, Mnuchin… and fellow TV star, Larry!).

Fat, dumb and happy investors following bullish instructions gladly accept the risk and get rewarded for it over and over again. It’s risk ‘on’ after all, isn’t it? Bernanke created this. One day, when it falls apart he will own it even if I am the last lunatic on earth drawing the correlation between he and future moral hazard. He will not be forgotten. I got time.

Again… emotion.

I keep writing that because I am the blogger (and letter writer) who bitches and moans when Twitter heroes rile up the mobs in justification of why they are not able to make money being bearish. I took a critique, processed it and have decided to just be me. I do by the way ask NFTRH subscribers for feedback every Sunday when the letter is delivered. The request is for general feedback, questions and especially for critiques and/or corrections. I can take it and I am not sure how many out there can as positions, reputations and especially egos seem to be well defended. It’s sort of a human default response, after all.

But to survive in an emotional war zone, which the continually manipulated stock and bond markets can be, the oh so human conditions of sensitivity, morality and camaraderie (bears and gold bugs for example, seem to form clubs based on their morality) need to be subordinated. The bugs especially have this damn “go gold!”, “got gold?”, “Comrades in Golden Arms” (CIGA) and “Gold Anti-Trust Action Committee” (GATA) thing going on. The pressure to be on a team is immense. Go TEAM!

Sure, gold stands in opposition to the chicanery of a well manipulated system. Sure, honesty is righteous. The bears have this in spades. But you have chosen – whether directly or through your financial adviser or money manager – to participate in a casino where the house does not always win, but is always in there trying to slant the odds. Either go buy a farm, raise chickens and plant corn or manage your better self in service to the casino’s rules.

As I write this the US stock market is pushing the extreme limits we had set for it. How far away SPX 2600-2650 seemed when we first set that resistance target in December. Now it is the market’s first key support level. Sentiment has flipped 180° since Christmas Eve and it is annoying to watch. The bulls are like Charlie Sheen… “duh, winning”.

When you join a team the urge to dig up information to justify your team’s stance is palpable. You gain the favor of your teammates and you are supported by your logic and sense of right and wrong. Until they bust the pig over its final hurdle that is; and then you are left scratching your head or worse, angry.

All I am saying with this piece of non-analysis is that final resistance parameters are at hand. The stock market will either fail after pushing the limits to extremes (how often has this been the case over the last decade since Bernanke opened the liquidity floodgates?) or it will invalidate the case that I for one would like to see, which is for another decline that would take back the entire post-2016 rally (and potentially provide a real buying opportunity).

The reality will be seen in hindsight. Best to be prepared for either case so that in hindsight you are not collateral damage to either the bull or bear case. Your own psychology can be adjusted because the market sure is not going to adjust itself to your desires. With patience the picture will clear.