Splitting shares fuels price-earnings ratio

The increase in the price-earnings ratio is amplified because many companies decide to split their shares during the acceleration phase of their existence. A stock split is required if the market value of a share has grown too large, rendering the marketability insufficient. A split increases the value of the shares because there are more potential investors when they are cheaper. Between 1920 – 1930 and 1990 – 2000 there have been huge amount of stock splits that impacted the price-earnings ratio positively.

| Date | Company | Split |

| December 31, 1927 | American Can | 6 for 1 |

| December 31, 1927 | General Electric | 4 for 1 |

| December 31, 1927 | Sears, Roebuck & Company | 4 for 1 |

| December 31, 1927 | American Car & Foundry | 2 for 1 |

| December 31, 1927 | American Tobacco | 2 for 1 |

| November 5, 1928 | Atlantic Refining | 4 for 1 |

| December 13, 1928 | General Motors | 2 1/2 for 1 |

| December 13, 1928 | International Harvester | 4 for 1 |

| January 8, 1929 | American Smelting | 3 for 1 |

| January 8, 1929 | Radio Corporation of America | 5 for 1 |

| May 1, 1929 | Wright-Aeronautical | 2 for 1 |

| May 20, 1929 | Union Carbide split | 3 for 1 |

| June 25, 1929 | Woolworth split | 2 1/2 for 1 |

Table 1: Share Splits before the stock market crash of 1929

| Date | Company | Split |

| January 22,1990 | DuPont | 3 for 1 |

| May 14,1990 | Coca-Cola Company | 2 for 1 |

| May 22, 1990 | Westinghouse Electric stock | 2 for 1 |

| June 1, 1990 | Woolworth Corporation | 2 for 1 |

| June 11, 1990 | Boeing Company | 3 for 2 |

| May 12, 1992 | Coca-Cola Company | 2 for 1 |

| May18, 1992 | Walt Disney Co | 4 for 1 |

| May 26, 1992 | Merck & Company | 3 for 1 |

| June 15, 1992 | Proctor & Gamble | 2 for 1 |

| May 5, 1993 | Goodyear Tire & Rubber Company | 2 for 1 |

| March 15, 1994 | AlliedSignal Incorporated | 2 for 1 |

| April 11, 1994 | Minnesota Mining & Manufacturing | 2 for 1 |

| May 16, 1994 | General Electric Company | 2 for 1 |

| June 13, 1994 | Chevron Corporation | 2 for 1 |

| June 27, 1994 | McDonald’s Corporation | 2 for 1 |

| September 6, 1994 | Caterpillar Incorporated | 2 for 1 |

| February 27, 1995 | Aluminum Company of America | 2 for 1 |

| September 18, 1995 | International Paper Company | 2 for 1 |

| May 13, 1996 | Coca-Cola Company | 2 for 1 |

| December 11, 1996 | United Technologies Corporation | 2 for 1 |

| April 11, 1997 | Exxon Corporation | 2 for 1 |

| April 14, 1997 | Philip Morris Companies | 3 for 1 |

| May 12, 1997 | General Electric Company | 2 for 1 |

| May 28, 1997 | International Business Machine | 2 for 1 |

| June 9, 1997 | Boeing Company | 2 for 1 |

| June 13, 1997 | DuPont Company | 2 for 1 |

| July 14, 1997 | Caterpillar Incorporated | 2 for 1 |

| September 16, 1997 | AlliedSignal | 2 for 1 |

| September 22, 1997 | Proctor & Gamble | 2 for 1 |

| November 20, 1997 | Travelers Group Incorporated | 3 for 2 |

| July 10, 1998 | Walt Disney Company | 3 for 1 |

| February 17, 1999 | Merck & Company | 2 for 1 |

| February 26, 1999 | Alcoa Incorporated | 2 for 1 |

| March 8, 1999 | McDonald’s Corporation | 2 for 1 |

| April 16, 1999 | AT&T Corporate | 2 for 1 |

| April 20, 1999 | Wal-Mart Incorporated | 2 for 1 |

| May 18, 1999 | United Technology Corporation | 2 for 1 |

| May 27, 1999 | International Business Machine | 2 for 1 |

| June 1, 1999 | Citigroup Incorporated | 3 for 2 |

| December 31, 1999 | Home Depot | 3 for 2 |

Table 2: Share Splits during the period 1990-2000

Share Splits keep letting the Dow Jones Index explode

The Dow Jones Index was first published on May 26, 1896. The index was calculated by dividing the sum of all the shares of 12 companies by 12:

Dow12_May_26_1896 = (S1 + S2 + ………. + S12) / 12

On October 4, 1916, the Dow was expanded to 20 companies; 4 companies were removed and 12 were added.

Dow20_Oct_4_1916 = (S1 + S2 + ………. + S20) / 20

On December 31, 1927, two years before the stock market crash in October 1929, for the first time a number of companies split their shares. With each change in the composition of the Dow Jones and with each share split, the formula to calculate the Dow Jones is adjusted. This happens because the index, the outcome of the two formulas of the two baskets, must stay the same at the moment of change, because there can not be a gap in the graph. At first a weighted average was calculated for the shares that were split on December 31, 1927.

The formula looks like this: (American Can, split 6 to 1 is multiplied by 6, General Electric, split 4 to 1 is multiplied by 4, etc.)

Dow20_dec_31_1927 = (6.AC + 4.GE+ ……….+S20) / 20

On October 1st, 1928, the Dow Jones grows to 30 companies.

Calculating the index had to be simplified at this point because all the calculations were still done by hand. The weighted average for the split shares is removed and the Dow Divisor is introduced. The index is now calculated by dividing the sum of the share values by the Dow Divisor. Because the index for October 1st, 1928, cannot suddenly change, the Dow Divisor is initially set to 16.67. After all, the index graph for the two time periods (before and after the Dow Divisor was introduced) should still look like a single continuous line. The calculation is now as follows:

Dow30_oct_1_1928 = (S1 + S2+ ……….+S30) / 16.67

In the fall of 1928 and the spring of 1929 (see Table 1) 8 more stock splits occur, causing the Dow Divisor to drop to 10.77.

Dow30_jun_25_1929 = (S1 + S2+ ……….+S30) / 10.77

From October 1st, 1928 onward an increase in value of the 30 shares means the index value almost doubles. From June 25th, 1929 onward it almost triples compared to a similar increase before stock splitting was introduced. Using the old formula the sum of the 30 shares would simply be divided by 30.

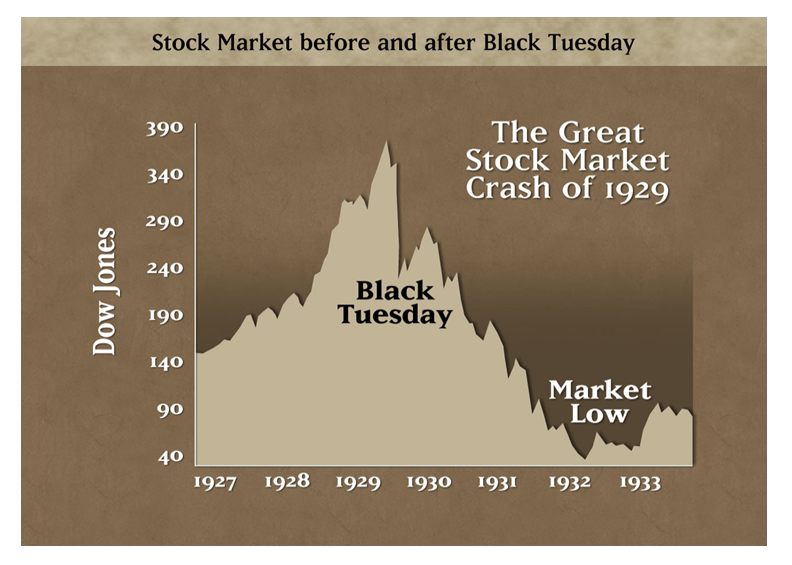

Figure: Dow Jones Index before and after Black Tuesday

The extreme rise in the Dow Jones in the period 1920 – 1929 and especially between 1927 – 1929, was primarily caused because the expected value of the shares of companies that are in the acceleration phase of their existence, was increasing enormously. The value of the shares is strengthened further by stock splits and as icing on the cake this value of the shares was enlarged again in the Dow Jones Index, because behind the scenes the formula of the Dow Jones was adjusted due to stock splits.

During the acceleration phase of the third industrial revolution, 1990 – 2000, history has repeated itself. In this period there have again been many stock splits, particularly in the years 1997 and 1999.

| Year | DJIA | Sum 30

Shares in $ |

Dow

Divisor |

Share

Splits |

| 1990 | 2810 | 1643 | 0.586 | 5 |

| 1991 | 2610 | 1318 | 0,505 | 0 |

| 1992 | 3172 | 1782 | 0.559 | 4 |

| 1993 | 3301 | 1535 | 0.463 | 1 |

| 1994 | 3754 | 1675 | 0.447 | 6 |

| 1995 | 3834 | 1425 | 0.372 | 2 |

| 1996 | 5117 | 1770 | 0.346 | 2 |

| 1997 | 6448 | 2100 | 0.325 | 10 |

| 1998 | 7902 | 1985 | 0.251 | 1 |

| 1999 | 9181 | 2228 | 0.243 | 9 |

| 2000 | 11497 | 2317 | 0.201 |

Table 3: Summary DJIA, Dow Divisor and amount share splits between 1990-2000

The formula that was used on January 1, 1990 to calculate the Dow Jones:

Dow30_jan_1_1990 = (S1 + S2+ ……….+S30) / 0.586

The formula that was used on December 31, 1999 was to calculate the Dow Jones:

Dow30_dec_31_1999 = (S1 + S2+ ……….+S30) / 0.20145268

On December 31, 1999 on an increase of the 30 stocks again nearly three times as many index points, the same value increase on January 1, 1990.

The exciting conclusion will be published here tomorrow.