It’s been a while since I’ve posted here on The Slope. Life has a way of pulling you in different directions. But I always find my way back, and for good reason. To Tim: thank you, as always. Fifteen-plus years posting on The Slope, and I remain genuinely grateful for this community. There’s nothing quite like it. For those who don’t know, I’ve spent the past several years building The Option Premium, a site dedicated to real options education with no hype, no flashy promises, and absolutely none of the marketing nonsense that plagues this industry. Just straightforward, honest strategy. I’m proud of what I’ve built there, and I hope some of you find it useful.

Most options traders do one of two things first: they buy a call, hoping for a rally, or they sell a put to collect premium on a stock they’re willing to own. Both are bullish plays. Both assume prices are going higher. But what happens when you don’t like the setup? When the market feels stretched, momentum is fading, and you want to express a neutral-to-bearish opinion with defined risk? That’s where bear call spreads quietly become one of the most underutilized tools in a premium seller’s arsenal.

The best premium sellers don’t stop trading when conditions shift. They flip the direction.

The bear call spread is the mirror image of everything you already know about selling puts. Same mechanics, same probability math, same income objective. But instead of selling downside risk, you’re selling upside risk. In a market that’s struggling to make new highs, that distinction matters more than most traders realize.

Reading the Room: Where the Premium Lives Right Now

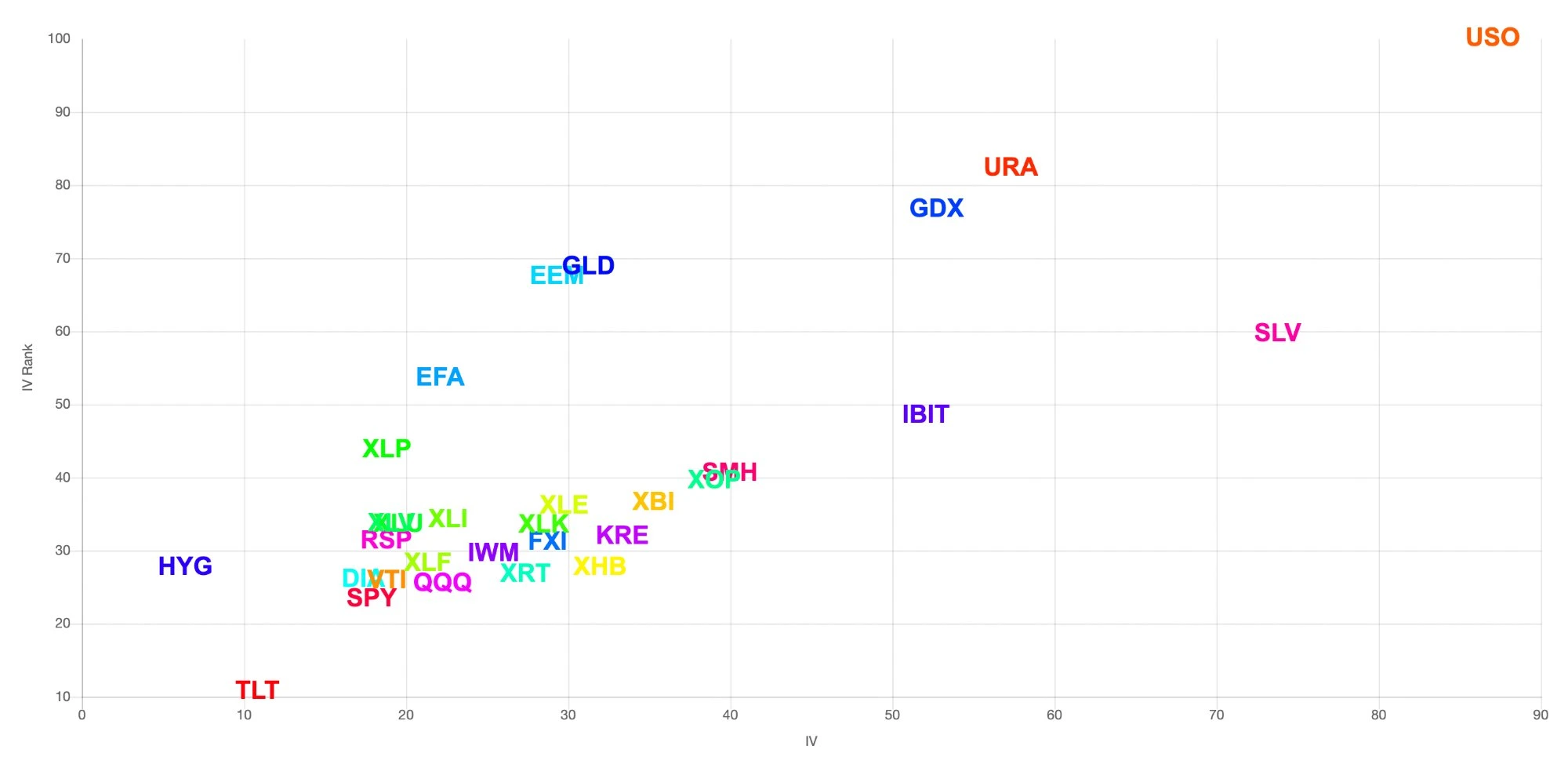

Before you build a trade, you need to know where the edge is. The scatter chart below maps implied volatility (IV) against IV Rank (IVR) across dozens of ETFs. IV tells you how expensive options are today. IVR tells you how expensive they are relative to their own 52-week history.

The upper-right quadrant is where premium is richest. When IV Rank is elevated, sellers collect more premium with the same structural edge.

Right now, volatility is elevated across a wide range of ETFs. That makes this an ideal environment to be selling premium rather than buying it. The strategy of choice when IV is high is straightforward: collect inflated premium, let time decay work in your favor, and let the market come to you.

The Structure Is Simpler Than You Think

A bear call spread involves two legs in the same expiration. You sell a call at a strike above the current price. You buy a call at a higher strike to cap your maximum loss. The difference between what you collect and what you pay is your net credit, and that credit is your maximum profit.

Nothing more moves. No shares change hands unless you let things get out of control. No margin calls from an unexpected gap higher. Just a clean, defined-risk position that wins when the underlying stays below your short strike at expiration.

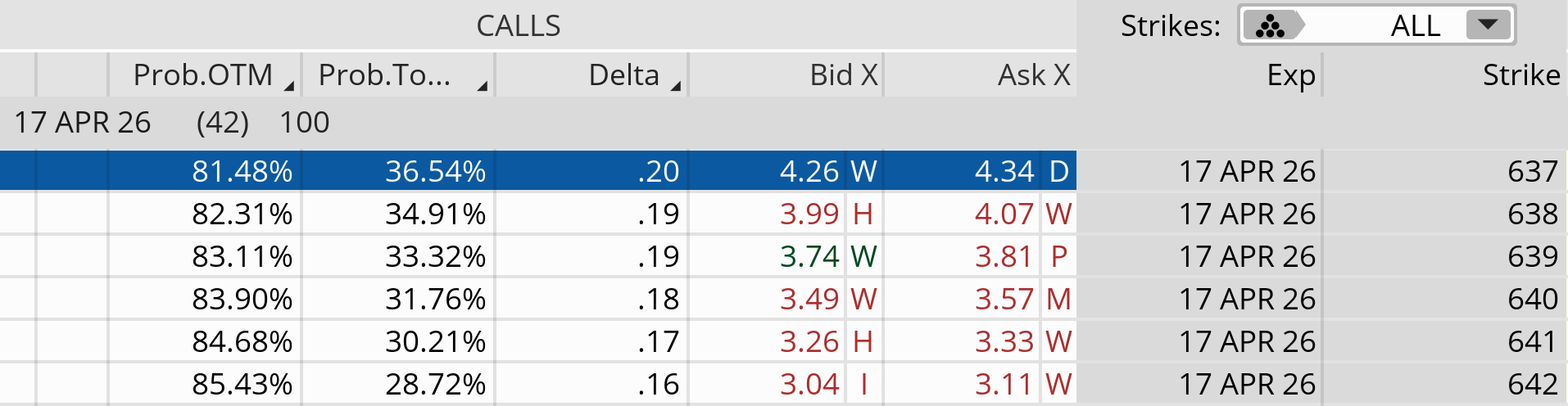

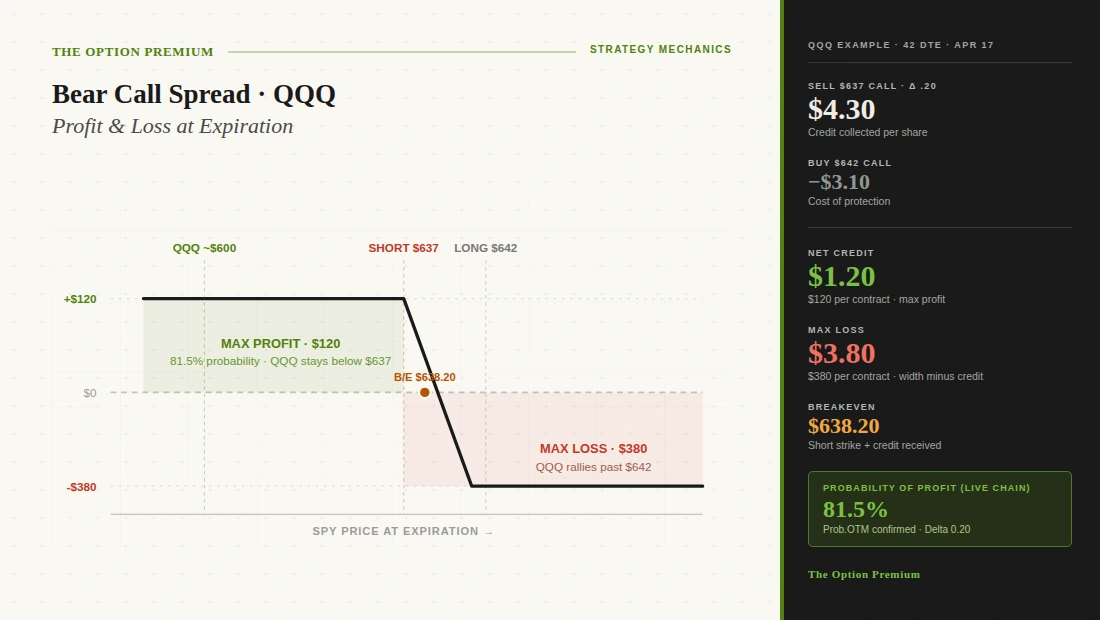

Here’s a live example using QQQ, currently trading near $600. Using the April 17th expiration (42 days out) and pulling directly from the options chain:

- Sell the QQQ $637 call (delta .20) for $4.30

- Buy the QQQ $642 call for $3.10

- Net credit received: $1.20, or $120 per contract

Your numbers: maximum gain is $120. Maximum loss is $380, which is the $5 spread width minus the $1.20 credit, times 100. Breakeven at expiration is $638.20. The $637 strike carries an 81.5% probability of expiring worthless, straight from the chain. QQQ has to rally more than 6% in 42 days just to threaten this trade.

The QQQ bear call spread: real numbers from the options chain, an 81.5% probability of profit, and a breakeven more than 6% above the current price.

QQQ doesn’t have to fall for this trade to work. It just has to stay below $637. The ETF can chop sideways, grind modestly higher, even make a small run, and you still keep the premium. That’s the edge in an elevated-IV environment: rich premium collected on day one, with the market needing to do something significant just to hurt you.

Strike Selection Is Where the Edge Is Built

The most common mistake with bear call spreads is placing the short strike too close to the current price in pursuit of more premium. You collect more, yes, but your probability of profit collapses. The trade stops behaving like an income strategy and starts behaving like a directional bet.

The disciplined approach targets a short strike in the 0.15 to 0.25 delta range. At these deltas, you’re placing your short call one to two standard deviations above the current price with a 75 to 85 percent statistical probability of expiring worthless. The QQQ $637 strike at delta .20 sits squarely in that range. The 81.5% probability of profit is confirmed by the chain, not estimated.

The 30 to 45-day expiration window completes the setup. This is where theta decay accelerates most meaningfully for sellers. Go shorter and gamma risk becomes a problem. Go longer and your capital sits idle without time working for you.

Managing the Trade: The 50% Rule

When a bear call spread reaches 50 to 75 percent of its maximum profit, close it. Don’t hold to expiration.

The last stretch of premium is the most expensive to earn. As expiration approaches, gamma accelerates. A single sharp move against you in the final week can turn a comfortable winner into a max loss. On this QQQ trade, that means closing when the position reaches roughly $60 to $78 in profit (per contract) rather than holding out for the full $120. Close early, lock in the gain, and redeploy the capital into a fresh position at better odds.

If the trade moves against you and the short strike is threatened with more than 10 days remaining, the plan is simple: roll the spread up and out for a credit, or close and move on. That exit plan gets made before you enter the trade. Not after.

The Bigger Picture

Bear call spreads pair naturally with bull put spreads to form iron condors. The best use of them is often as the second leg of a position, layering the call side on after the put side is in place once IV on the call side justifies the entry.

The scatter chart tells you where to look. Volatility is elevated. Premium is rich. The QQQ trade above is live: real strikes, real premiums, real probabilities pulled directly from the chain. Whether you take this exact trade or not, the framework is the same. Find elevated IV Rank, sell a call spread above the market, and let time and probability do the work.

Trade Smart. Trade Thoughtfully.

Andy Crowder, The Option Premium