ISM’s Report on Business (RoB) blisters upward, but…

My former residence within the real economy was right here, in the manufacturing base. I don’t miss it even one little bit, but were I still involved we’d be booming and bitching. Business would be very good and prices and supply constraints very aggravating. The way things went in my segment – Medical Equipment, often pressured by Medicare constraints and general competition – I’d be getting hit over the head by customers about maintaining low prices while facing immovable obstacles in the form of supplier prices and extended deliveries. Now I write for a living. It’s a no-brainer I guess.

That digression aside, let’s look at the RoB. Here is the headline. You can click the graphic to grab the entire report (pdf).

New orders are growing rapidly. That is important. Production is growing rapidly, but that is the tail to the new orders dog. Not material as a forward indicator. Employment is great. It’s a boom. A boom created by…

…and his monetary magic. But a boom nonetheless. A boom on the heels of the crash a year ago, which itself came on the heels of an already in progress slowdown that was taking shape in 2019 (as manufacturing started to cycle down and gold bottomed).

Ah, but the Wizard. Ah, but inflation. Willfully printed by the Fed (monetary) and administered by the governments of both parties (fiscal). But the real tax and spenders are in there now and it is scary, especially if the Fed is forced by market constraints to cease or limit its inflationary actions while the spenders simply look to taxation as the primary funding mechanism.

Digression #2 aside, let’s move on. Supplier deliveries and inventories are relatively immaterial to the discussion. Backlogs of orders are good and import/export orders is the realm of Art Vandelay and not really important here.

What is important for we casino patrons trying to manage financial markets going forward?

Well, you know.

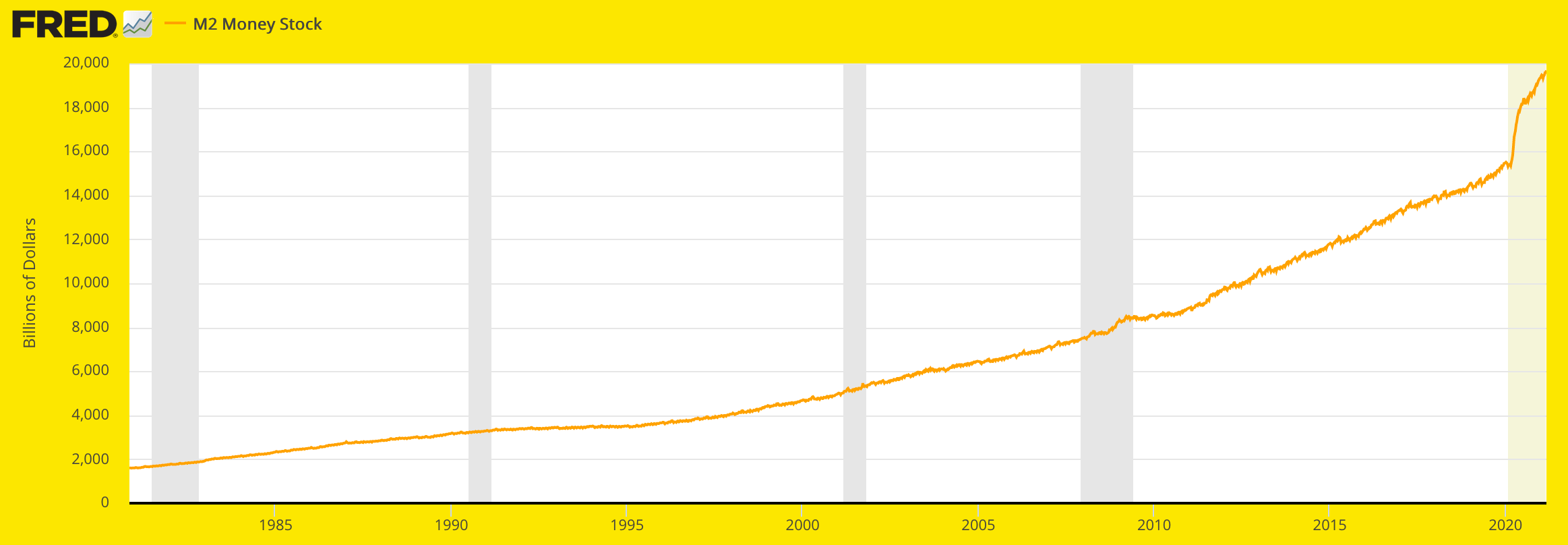

The Wizard has a lever he pulls behind his curtain. That lever is called inflation, one measure of which is approaching levels that saw a ruthless liquidation in Q4 2008 and the Fed’s cagey (and brilliant) inflation sanitizer, Operation Twist come about in 2011 to control the Yield Curve in a way that painted everything as a-okay. To paraphrase Steven King, nope, no inflation here.

The Fed creates inflation by manipulating bonds (debt) and printing (funny) munny into existence. Here is one measure of that munny. Look at the epic inflation they are trying to create out of the COVID-crash as compared to the recessions that preceded it. The 2008 disaster looks like but a blip in comparison.

You partisan types will need to try to be unbiased because both political parties will be seen as complicit when we look back at this mess in the future. The vertical ramp job came under Trump and it’s only getting worse under Biden. In fact, Trump was badgering Jerome Powell repeatedly to manipulate bonds and print long before the Corona effing virus came around.

So yay! American manufacturing is booming again. So are the prices manufacturers are paying. While I will continue to respect the possibilities for an ’08-like crash and deflationary liquidation of this developing mess, I will also respect the idea that we could be headed for a full frontal confrontation with Stagflation. The violence of the upward spike in money supplies and now prices paid that have been pushed into the economy, is something we have not seen in a long time. So how do you quantify the Stag if that is what is out ahead?

Personally, I’ll have indicators to gauge its arrival. But that does not mean I am sure how it will play out, other than it will eat away at the economy, including the manufacturing sector. Inflation is perceived as good, maybe even heroic at first. But that will not endure. Probably time to read up on ole’ Ludwig van, err von…

Here is a clip, but check out the link.

The Unrelenting Power to Inflate

If people expect a forthcoming, drastic increase [in] the money supply — but if they at the same time expect that such an increase will be limited (i.e., a one-off increase) — the central bank can actually orchestrate a debasing of money without causing its complete destruction. As long as government and its central bank succeed in making people believe that any future rise in the money supply will remain within an acceptable limit, from the viewpoint of the money holder, monetary policy is an effective and most perfidious instrument for expropriation and non-market-conforming income redistribution.

This may explain why Murray N. Rothbard, in his famous essay The Case for a 100 Percent Gold Dollar, wrote the following:

I am not saying that fiat money, once established on the ruins of gold, cannot then continue indefinitely on its own. Unfortunately … if fiat money could not continue indefinitely, I would not have to come here to plead for its abolition.

Rothbard saw the danger that the government-controlled fiat money could be held up and running indefinitely, that it would not necessarily drive itself into a fatal and final collapse. As long as people do not expect that a money supply increase will spin out of control, the central bank is in a position to debase the currency without completely destroying it.

So when stuff like this comes out, you can bet the Fed is paying attention.