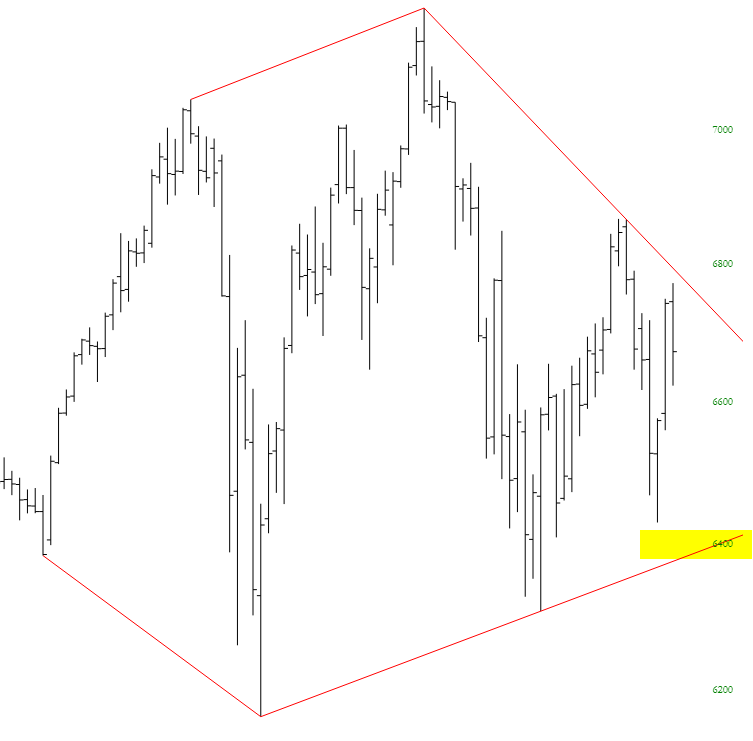

From Mike Paulenoff: In early March, 10-year yield was circling 2.87%. Now it is circling 3.00% for the first time in 4 years. The increase is probably shocking to many analysts and investors. Neither economic nor inflation data provide adequate justification for yield to be higher than it was two months ago. But there are times when the contradicting longer-term technical set-up should be heeded, even when the trend lacks strong support from lagging tabular data.

In scanning the past few months of U.S. economic data – such as Retail Sales, New Home Sales, Personal Spending, Consumer Prices, Non-farm Payrolls – what jumps out is the variability of the data. Most of these data series reflect a zig-zag pattern that belies a consistently strong directional economic impulse.

On April 27th, investors received their first look at the advance estimate of Q1, 2018 GDP, which came in at 2.3% compared with consensus estimates of 1.8% to 2.0%. More surprising, perhaps, was the subdued Q1 Price Index at 2.0% versus estimates of 2.4%, although the inflation gauge did remain at the Fed’s 2% target. (more…)