Hello, Slopers!

First I would like to thank you for your kind words, I was very happy to see you appreciate the previous content. Hopefully that will end up having a positive impact for some if not all of the community.

Now, after having seen that the FED is (most probably) at its most restrictive stance in decades (pressure index), not only on the interest rate front but also doing QT at a $90B per month pace making the case for the highest probability of a recession in a long time, three main questions are left:

- How bad is the recession going to be?

- How long before SHTF?

- How bad of a bear market can we expect?… if we ever get one! because YES believe it or not but some people are saying that even if we go into recession that doesn’t even imply risk assets to be dumped.

Regarding the first question I’m going to be brief, it’s anyone’s guess!

In my opinion this it’s gonna be bad but what do I know, I prefer not to argue on that subject.

The only thing I would say is that there are numerous things that would point to a bad to very bad outcome. Also that the last two recessions were not really soft if I recall correctly.

Ok, so how long before SHTF?

It’s commonly admitted that rising interest rates have a lag effect on the slowing of the economic tissue. The consensus is that the full effects of monetary policy is somewhere between 12 to 18 months.

Powell started to raise rates in March 2022 so today is right in the middle of that lag window.

Some may even argue that the full effect of the first rate hike is yet to be felt, if that’s the case may God help us for what’s coming toward us. Remember all of the 75bps hikes that followed?

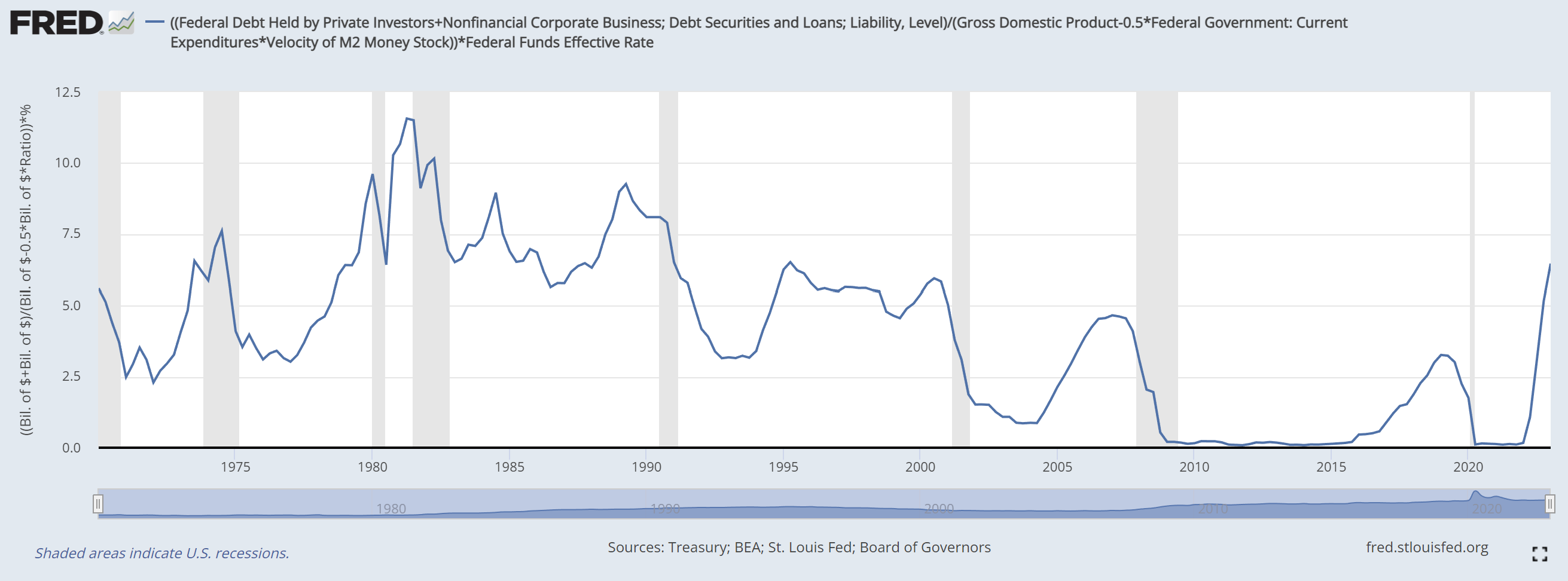

I’ve worked on another “Pressure index”:

This time I wanted to focus more on the parts that may send the SHTF so the formula is as follows.

[Federal debt held by private investors (the problematic part of the total gov debt) + non-financial corporate debt] / [GDP-0.5*gov expenditures*velocity of M2]

Subtracting half of gov exp because that’s about what the deficit ends up to be on average, in other words the gov spends twice as much as it earns… wouldn’t it be cool if we all could do that in perpetuity?

Then once again this serie can be combined with an interest rate (the FFR in that case)

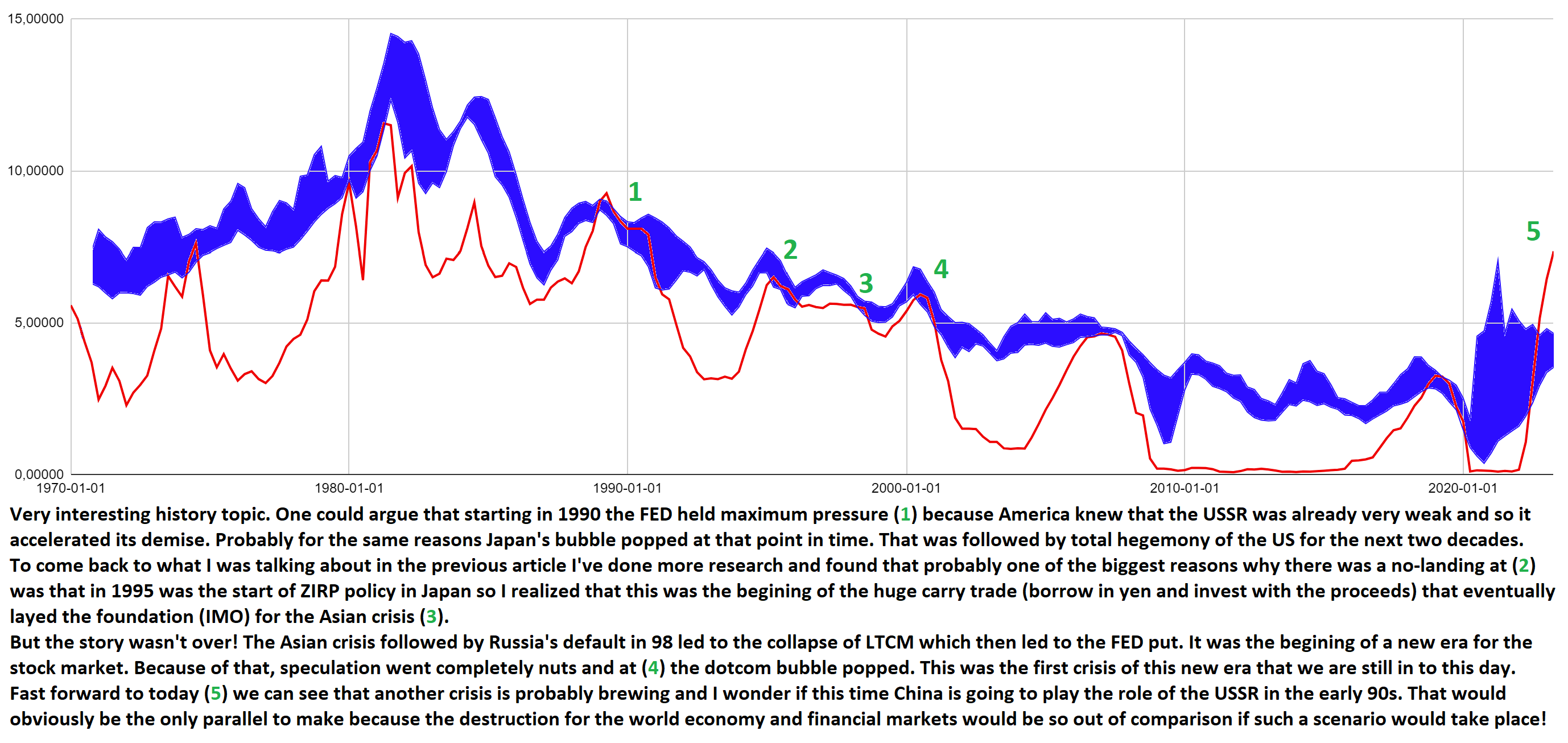

This chart stops in Q1 23 but I’ve made some calculations to add Q2 on the following one.

I then added some cool band (Minimum-Maximum) of GDP growth and 10Y yield (ask me for if you want the exact process) and I really like the end result:

So, looking at recent history it took something around 2 quarters to hit the fan once the pressure index hit the band, 3 to 4 in 2007 and 4 in 2019-20.

Today we are entering the 3rd quarter ABOVE the band. As you can see COVID created a lot of noise (very large band) but it looks like we are going back to something readable again and it seems to be somewhere below 5. If true, that shows once again how restrictive the FED is right now and I wouldn’t be surprised to see Powell continue to raise rates and for that to be regarded in the future as one of the biggest policy mistakes in FED’s history.

IMO the problem is that he knows that he has no choice: doomed if he does and (even more) doomed if he doesn’t. The FED is in the corner after having played with fire for so many years. In fact that’s one of the many reasons why I think this is going to be so bad. Time will tell.

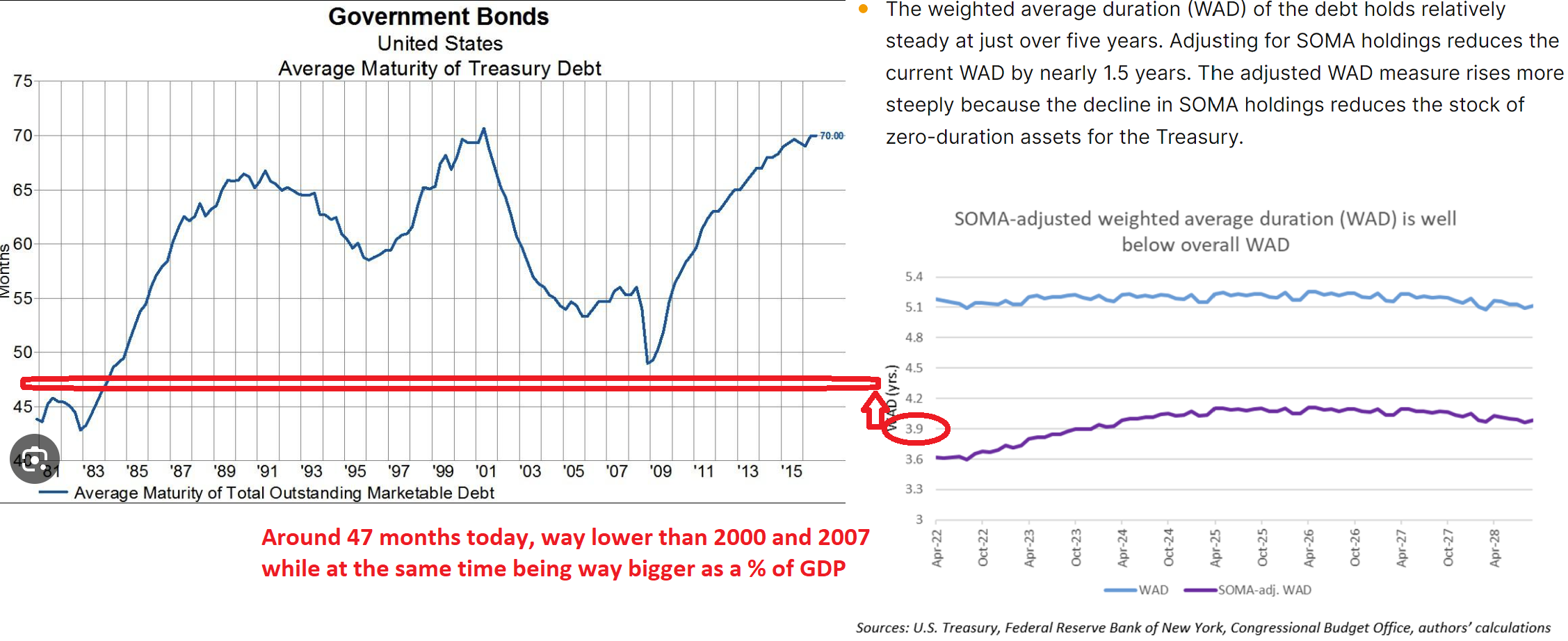

Now of course every recession is different, inside the huge pile of debt that I’ve used to construct my index not everything is impacted the same by the FFR, not everything is a bad unproductive debt. Duration is one of the biggest key to understand the “when what and how” when it comes to the consequences of this tightening cycle.

Concerning corporate debt I won’t comment on the subject as I’m certainly not qualified enough for that. Furthermore I would like to say that I’m not qualified for anything, I’m only a lone amateur doing its best and, the more I study, the more I try to get better, the more I realize that “All I know is that I know nothing” as Socrates would say!

On the other hand, concerning public debt I would say that we can expect things to become problematic way faster than in 07 because of several things:

- Operation twist which increased the average maturity of the debt held by the FED (the less problematic part of the public debt) therefore reducing the av maturity of the rest of the pile (the problematic one)

- More recently after the resolution of the debt ceiling, Yellen targeting the RRP funds in order to rebuild the TGA without having an impact on bank reserves. That can only be achieved by emitting on the shortest part of the curve, the one that is yielding more than RRP.

So if I had to guess I would say that time is running very short but again… what do I know!

That’s already a lot so I’m going to let you deal with that and we’ll see you next time.