FORKS IN THE ROAD

It doesn't matter what you call it, the USA and global markets have arrived a period of time where we will see important actions and reactions that impact us all as investors. Sometimes you cannot see these crossroads coming, other times it is like you are coming up to a big flashing billboard notifying you of the gravity of the situation.

Central bankers will be quite busy over the next couple of weeks attempting to find solutions that don't involve changing the way banking and business is done in the world. (In other words, these guys will be attempting to extend and pretend just a while longer….again). My goal in this post is to highlight the areas of concern and give a few ideas regarding positioning of a portfolio for these issues. In a later post, I'll examine concrete actions and explore the most likely issues that will create dislocations in our economic system.

FEDERAL RESERVE

At the end of June the Fed has disclosed it will terminate its Quantitative Easing II program. The Fed promised to stop making purchases of US treasuries. Since last September, the Federal Reserve has used printed (new) money to purchase bonds from primary dealers in the open market. As the Fed exchanges treasuries with newly printed money, the net result is that these dollars become investment ammunition in the hands of banks and brokerages. Holding new dollars, these institutional investors seek to invest in all markets and find the currency finds its way to all kinds of speculative assets (commodities, stocks, corporate bonds, etc).

When the Fed warns that they are going to stop the flow of additional purchases, they are saying that they will stop the liquidity wave from growing larger. It is important to note that they have kept their options open to continue to keep levels the same. As bond issues in the Fed's portfolio matures, they can still reinvest the proceeds into other vehicles by purchasing other assets like MBS (mortgage backed securities), TIPS, or other treasury issues.

The termination of the additive effects of additional capital in the QEII program doesn't in itself signal that the stock market is going to drop significantly; it does mean that some of the propellant for incrementally higher prices may not be available now. Further, as investors anticipate these actions, we have seen savvy managers rotate out of treasuries and move into more defensive equity holdings in an economic cycle rotation play. These managers believe that the economy may be slowing in conjunction with the Fed's move and therefore have gone to relative safe haven positions in consumer staples, health care, defense industries, and utilities.

EUROPEAN DEBT PROBLEMS (AGAIN)

It seems as though we are in a significant place where the Eurozone countries are now in distress and major work must be done to avert a collapse of the EU infrastructure. Greece is once again in the cross hairs and it is obvious that despite many attempts to delay and defer, reality is coming home. Greek estimates for tax revenues and economic growth have completely missed and therefore have pressured any assumption that the tiny country can pay back the interest and debt that it owes. Additionally, civil unrest has brought any productive asset to a stop in the island nation and further weakened its position. We know that many of the countries there are insolvent, but that doesn't necessarily mean that we'll see a collapse in asset prices globally or even in the price of the Euro, it just means that more EU taxpayer money will be funneled off to bandage the wealthier banks in the Eurozone (Germans). We know that central bankers don't want to have another financial collapse, so we will see heroic measures to save the system, no matter what happens.

As I type this, we find that those heroic measures are clearly underway. This Bloomberg article highlights that the talks aim to force Greece to sell off many of its national assets and undergo further austerity measures. In return, they'll get more loans they won't be able to repay. GREEKS NEED $65 BILLION MORE. A follow up story to this was just also penned stating that German leaders are digging in their heels and demanding that investors in bonds step up to the plate and take haircuts in this second round of retooling. The ECB is rejecting this approach because the loss on investments is technically a default. GERMANS DIG IN THEIR HEELS.

Now, it is not clear what final measures will be taken to save the system, but there are some pretty obvious results we can look for. First, I assume that we'll actually see a deal get done this time for Greece. Ultimately though, we'll endure this threat many more times as each country on the periphery is forced to approach the IMF and ECB with hat in hand. At some point, a country like Greece, Spain, Portugal, or Italy, will simply tell the political and banking leaders that they won't make further concessions and we will witness a default event that will be a powerful event for the Euro.

As investors of sovereign bonds are forced to take write downs (losses on their investments), we will see a massive drop in value of the Euro relative to the USD. This shaking will also rattle the US stock market as well. Oddly enough, instead of sending all assets including commodities lower, we may see the value of gold and gold miners move higher even though the USD would move higher as well. To some extent, silver may participate, but I think that gold will outperform silver or any other commodity in this situation.

CHINA

First a word on the Euro issue in relation to China. China is deeply connected to Europe and this is why you may be starting to read more and more about China's involvement in buying sovereign debt of these problem PIIGS. If Europe collapses or goes into a significant recession, China will be hurting too. Europe is a huge consumer of Chinese products, and a draw down in consumption will only damage the Chinese export based economy more.

China desperately needs its workforce working and commodity pricing pressures coupled with a slowing Eurozone economy would only contribute to idling its immense labor force. Penniless, hungry, angry, and bored workers are one of the few things that Communist China fears. China will gladly lose a few billion Euros in order to buy time and keep its populace at work.

This civil unrest potential is absolutely too much for the central planners in China to risk, therefore it isn't difficult to see a coordinated global interdiction to interrupt a collapse in Europe with China as a major liquidity provider.

While the moves of China in Europe will be made at a central level to stabilize global economies, these moves will be handcuffed because inflation is also tugging at the emerging giant threatening the country in another direction toward overheating. To cool the economy the central bank in China is restricting loan liquidity, raising interest rates, and doing everything possible to reduce this risk. While China is still growing at an amazing pace, these moves will ultimately create a slowdown and that in turn could be very negative for all global economies and commodities.

Inflation is a significant concern in China because it impacts their ability to feed their nation and also to remain competitive in the global export market. As noted above, China's gateway to the global economy has been through its cheap labor pool and also low levels of environmental regulatory roadblocks. As inflation pushes up prices of raw materials and labor costs skyrocket to keep pace with price gains in food, Chinese manufacturers are increasingly more expensive than other 3rd world emerging competitors. Countries like Malaysia, Thailand, and Vietnam are all attempting to encroach on the Chinese dominance in manufacturing and global export. Until China develops its own domestic markets it must do anything and everything possible to fend off attacks from these competitors, and inflation is clearly making that fight more difficult.

Further, Chinese real estate has been under attack as the leadership has attempted to cool real estate speculation in the mainland. Interest rates have been increased many times yet investors continue to buy assets where there are no real buyers. Please view the report we highlighted on China's ghost towns - BIG TROUBLE IN BIG CHINA (REAL ESTATE MADNESS)

JAPAN

The mainstream media has tired of reporting on this disaster so it would be easy to forget that this issue continues to get worse and worse. What? You didn't realize that it still wasn't under control? You hadn't heard that of course. If you'd like to take a look at the most current IAEA slideshow from May 31st you'll see that while each of the reactors is classified as "subcritical" there have been almost no other important milestones reached. TECHNICAL BRIEFING. Now there are a host of issues that go beyond the human tragedy which has cost around 14,000 known lives along with another 14,000 Japanese that are missing.

This terrible event also has the ability to be far-reaching in other areas too. I've stated that one of the gravest concerns for market participants is that the Japanese begin selling their US Treasury positions to fund their own liquidity needs and to meet obligations related to the reconstruction of the devastated areas. Sales of US Treasuries will put pressure on our interest rate structure and could push them higher, something our Fed and Treasury have been fighting against for almost two years now. (Remember, QE II is a policy tool for reigning in interest costs on our massive deficit spending as well. By keeping rates artificially low we remain able to pay our interest expense).

We've seen other impacts as manufacturing plants have been offline and unable to produce component parts for cars and other complex machines. The outages related to the earthquake and tsunami has disrupted the entire global supply chain system of fulfillment. I urge you to continue to monitor the situation in Japan as we all know that there are major ramifications still to be felt as a result of the disaster at Fukushima. While we tend to think of the "fallout" as radioactive, major fallout out will rain in the spheres of energy policy, politics, and economics as well.

OIL

The Fed's action to create excess liquidity to buoy asset prices has impacted oil significantly. Yes, the fall of the value of the dollar has been the cause for some of the jump, but the moves have also been as a result of the creation of the tsunami of cash in the hands of "speculators". Those speculators come in the form of hedge funds, banks, and pension plans of course. Higher oil and gas prices have all sorts of nasty affects on everything else the world produces and consumers, so we are seeing these price shocks ripple throughout all markets.

The unrest in the Middle East which has been named the "Arab Spring" or "Jasmine Revolution" can be attributed greatly to our own Fed's work in commodity markets. It is quite scary to me to think that the Fed could do in a few months what many Presidential Administrations couldn't do in decades. While weather issues also have contributed, the Fed has been able to engineer a massive increase in food staples like corn, rice, wheat, and soybeans. These revolts started in Tunisia and have worked their way through Egypt, Saudi Arabia, Yemen, Libya, Jordan, Syria, and Iran.

As we noted above, hungry unemployed people take drastic action, and these people have risen up and demanded change in their countries. Interestingly, the very act of revolution in these countries has exacerbated the oil price issues in the rest of the world. This is not to say that these places were wonderful locations to live, that the leaders were not brutal and the situations not oppressive, it is merely that the actions of our central bank has resulted in the creation of the final straw that was broken to unleash a wave of discontent throughout the entire world. Why is any of this important to us?

- + First, unrest in the Middle East is destabilizing to the world economy because our economic fuel (our oil supply) becomes uncertain.

- + Next, the uncertainty of these fuel supplies forces other nations to take action. Have you thought for a moment what the US and NATO is doing attacking Libya? The nation produces about 200,000 barrels of oil a day despite having proven reserves of 46 billion barrels. Libya is not important to the US, but is extremely important to Italy and Germany.

- + Third, desperate leaders will do crazy things to stay in power. Think through the actions we've witnessed in the last several months. Egypt fell, Saudi Arabia's King essentially bribed his people, Syria, Iran, and Libya's leadership attacked its own people. In the case of Syria and Iran if there is a growing of the revolutions inside the countries is it far-fetched to believe that they might attack Israel as a distraction to turn the attention of the populace to other things?

- + Last, high oil prices often result in a slowing of economies. When it costs more to ship products or fly somewhere for a vacation, people tend to consume less and hold on to their money. Oddly, this is exactly the opposite of what our Fed is trying to accomplish.

West Texas Int Crude –

Gasoline – UGA

US MARKETS

The US housing and jobs markets continue to suffer and languish. With the threat of a removal of stimulus from the system by the Fed and a correction in stock markets underway, we need to continue to remain vigilant. I think the correction in commodities in the first part of May was a big warning to us and even though we've seen a rebound to fill some gaps we may see asset prices fail and fall lower.

Earlier this week Robert Shiller noted the same things he had been saying for the last year or so, that he expected US housing markets to drop another 15% to 20%. Oddly, someone actually paid attention to his statements. I think this comment coupled with the weak jobs data suddenly woke some folks up. There is a real concern that the economy is double dipping and signals from ECRI's LEI (Leading Economic Indicators) has shown that we've had several reports in a row that show slowing and weakness.

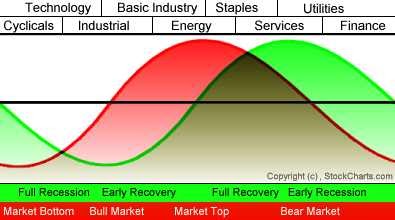

Beginning in early May we noted in this blog that sensible portfolio managers would be trying to get ahead of other participants anticipating a slowdown and a turn in the economic cycle. (Thanks to Stockcharts.com for the wonderful graphic that is a representation of the cycles and notes what equity sectors do well in that period. The model is based on work done by Sam Stovall with Standard and Poors.)

As we look forward, I think we are at the tail end of the industrial/ energy / commodity cycle and we'll be entering a more defensive period where consumer staples (think soup!), defense, and health care will be the places that portfolio managers look to invest. They will do this for safety and pre-recession posturing, but also for the dividends. A Consumer Staples ETF is XLP, Healthcare is XLV, and Defense is PPA. Now you can see that I'm not the only one seeing this rotation as all 3 of these are really ramping over the last month or so. XLU is also good target for consideration here for exposure to utilities. Given all the inflection points and issues I've noted above, I AM NOT saying that you need to buy these things, I am simply noting that this is what managers are doing right now.

BONDS

Overall, we must continue to watch bonds as a gauge for the most visible warning that one of these problem areas explodes into a full blown economic crisis. It seems that Pimco's Bill Gross' call around mid April to short treasuries was pretty much a bottom for US government bonds, what a tough business! Don't blame Bill though, as he will ultimately be proven correct. What is happening now is simply a fear based moved to "relative safety" as equity and commodity markets have declined and folks are fleeing the risk of the Euro. If the Eurozone does have trouble "fixing" Greece and the other PIIGS we'll see a continuation of the bond rally, but if some short term resolution is found, the Fed and Treasury might lose their cover of under priced risk premiums for treasuries. There is a huge supply of bonds and a dwindling amount of buyers, so we should see pressure on rates to move up. A significant move up or a jerky, sudden leap would be our signal that things are getting out of control.

50,000 FOOT VIEW

Let's take a step back though and look at what might be happening in the broader context to the markets. Is there a chance that all of these inflection points are just issues we'll face and overcome? Yes, absolutely. Investors must ask themselves if we haven't already endured several similar occasions like the concerns over a slowing economy, a poor housing market, sluggish job growth, and also a threat that the debt ceiling must be raised. Many of these concerns were faced last year in January and February 2010. Look at a chart of DIA and note that there was a significant correction from $105 down to $98. During that time Congress was faced with the burden of raising the debt ceiling and markets shook, but then ultimately moved higher until reality visited us again and the Fed stepped in with QEII in August of 2010.

THIS TIME IT'S DIFFERENT?

Is this time different? I tend to think not. We will once again see a lot of posturing and prattling on about the out of control debt and spending in Washington. We'll endure politician after politician emphatically sounding the alarm that the situation must be addressed, and we'll see them meekly vote to raise the limit just like all the times before.

The length of time Congress takes to act out their charade will determine exactly how long the stock market will stutter and hiccup. Unfortunately I am a bit jaded by the experience of seeing our elected representatives go through this process and I admit that I tend to view Wall Street as complicit in this absurd theater. I sense that investors exit stage left in order to add more drama and effect to the entire presentation. As if on cue, we see markets roll, invoking the threat of economic collapse if that debt ceiling isn't raised. (Recall TARP and that whole hostage negotiation!)

At the end of the day, this is what our leadership is hoping for, that all of these core issues can be overcome with more talk, more debt, and more printing. The sad truth about all of this is that once again the short term results may be that the stock markets move higher in response to an elevation of the debt ceiling and a resolution of the Greek debt problem (for now). While my last couple of paragraphs may convey the idea that I believe this is all going to be alright, I am most concerned if we actually face a "this time it's different" moment. If this time truly is different, we are all in trouble.

Over the next couple of days I will be working on the June Monthly Macro Report and a follow up post to this article where we look at actionable steps to take to prepare for a few of the likely scenarios we'll face. I had to put this post together to reset the issues in front of us in order to know what is driving market participants and economic leaders. The critical items we are facing demand action from central banks, politicians, and adept investors. The time for action is quickly approaching. Please check out the blog at www.goatmug.blogspot.com when you have a moment.