Further to my last weekly market update, this week’s update will look at:

- 6 Major Indices

- 9 Major Sectors

- Advance/Decline Issues Index

- SPX/VIX Ratio

- 30-Year Bonds

- U.S. $

6 Major Indices

6 Major Indices

As shown on the Weekly charts and 1-Week percentage gained/lost graphs below, all but one Major Index closed higher on the week than the prior week. Once again, the Dow Transports Index gained the most (and made a new life-time high), while the Nasdaq 100 lost a minor amount (as AAPL continued to decline and weigh on the NDX, as I last wrote about here). The Russell 2000 Index also made a new life-time high.

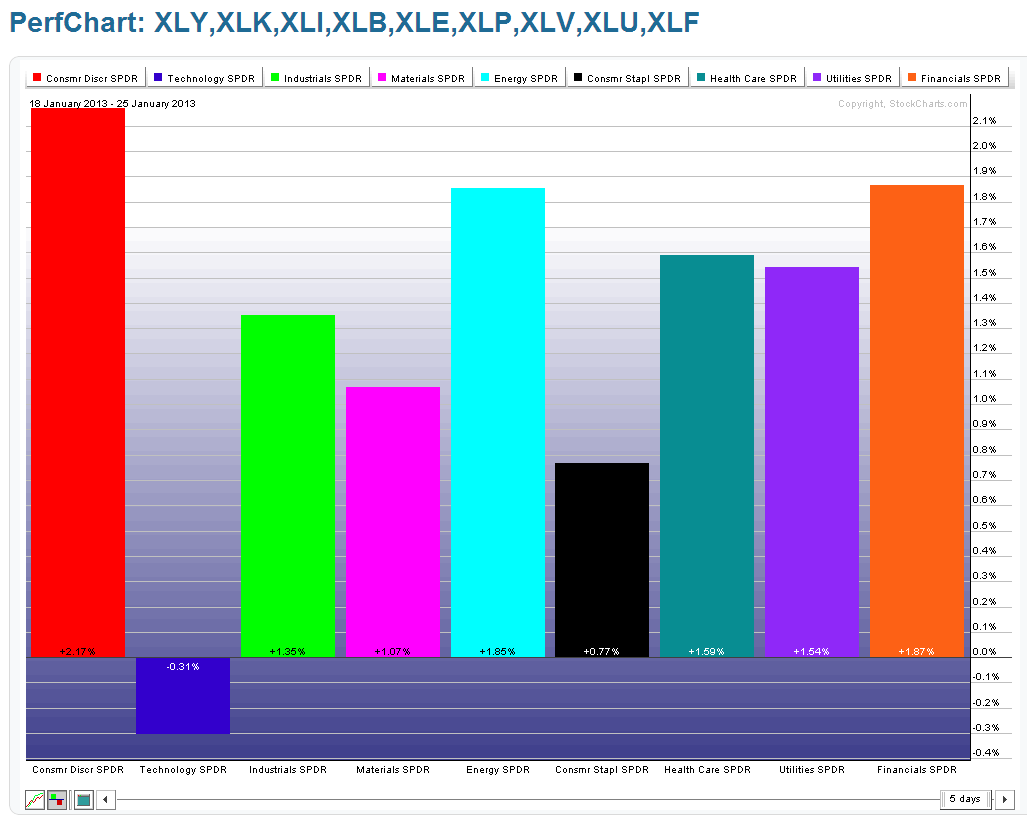

9 Major Sectors

As shown on the Weekly charts and 1-Week percentage gained/lost graphs below, all but one Major Sector closed higher on the week than the prior week. The Consumer Discretionary Sector gained the most and Consumer Staples gained the least, while Technology lost a minor amount. Consumer Discretionary, Consumer Staples, and Healthcare made new life-time highs, while other Sectors have quite a ways to go before claiming that title.

Advance/Decline Issues Index

The general stock market advance of the past week (and since 2009) can be seen on the first Weekly Advance/Decline Issues Index chart below, as it closed on Friday in positive territory above the zero level, but slightly below last week’s close.

The next Weekly Advance/Decline Issues Index chart below shows only the closes. You can see that, although most of the above Major Indices and Sectors gained on the week, they did so on slightly fewer issues than the prior week.

Since June of 2012, there have been more closes in the +1000 to +2000 zone than in the -1000 to -2000 zone, showing that more issues participated in the advances than in any of the declines seen during the past seven months.

Even though I mentioned in last week’s market summary that these Indices and Sectors were in extreme overbought Stochastics territory (on a Weekly timeframe) and that we may see an increase in volatility, you can see from this chart that they did not close at the extreme +2000 level.

Should the markets continue their push upwards over the next week(s), this chart may hold more of an indication as to when they may have reached a protracted and extreme overbought condition…particularly since there are still quite a few Major Sectors that still have quite a ways to go before making new life-time highs, and four of the six Major Indices also have yet to make that claim.

In any event, it would seem that any closes above the -1000 level represent general buying opportunities…if we start seeing more Weekly closes below that level, it may be signifying that some serious selling has begun in equities…you can watch intraday timeframes for clues on short-term strength above either the zero level or -1000.

SPX/VIX Ratio

The 1-Year Daily ratio chart of the SPX:VIX shows that there was a slight increase in volatility in the SPX this week as the Momentum indicator lost some of its previous bullishness and closed just above the zero level. It’s one to watch going forward to next week, as we may see a pickup in volatility as we approach the FOMC meeting on Wednesday, as well as month-end and all of it’s associated activity. Near-term support for this ratio sits at 116.50…a break and hold below will send volatility (VIX) up.

30-Year Bonds

Price closed just below major support, as shown on the following 5-Year Weekly chart of 30-Year Bonds…one to watch for a lower close on increasing volumes next Friday as a possible confirming signal that money is finally leaving Bonds to be deployed in equities this year, (and/or commodities as I recently wrote about here).

U.S. $

As shown on the 5-Year Weekly chart below of the U.S. $, price closed just below the 80.00 major support level…one to watch next week in reaction to Wednesday’s FOMC announcement…there is no Fed Chairman press conference afterwards, so there may not be much in the way of any new policy emanating from this meeting.

Summary

In summary, we may see a general advance in equities for some time this year, punctuated by pullbacks, as buyers rotate into and out of various Sectors/Indices to relieve overbought scenarios and (for those that haven’t already) to, perhaps, reach new all-time highs.

Clues may be found in the Advance/Decline Issues Index, SPX:VIX ratio, 30-Year Bonds, and the U.S. $, as well as upcoming economic data releases, company earnings announcements, and, of course, domestic and global news releases. Some sectors in Commodities may also see some advancement, but, no doubt, the Fed will be keeping a close eye on inflation to keep things in check…their “transparency program,” forward guidance forecasts, and future press conferences should also provide clarification on where economic conditions and unemployment stand and are headed, for the benefit of market participants.

However, what may dampen the extent to which we may see an overall market rally this year is the latest Bank of Canada’s monetary policy report that was released earlier this week, as I wrote about here. Their report is forecasting a slightly weaker global economic outlook than was projected in October, although global tail risks have diminished.

~~~

Enjoy your weekend and good luck next week!