I spent the weekend going back to Q1 2007 through the most current quarter and pulled financial data from BAC financial statements (yeah, I know, I need a life). What I want to understand is very simple. Does BAC have the earning potential to absorb a further drop in home prices.

I'm sharing this data as part of a group think exercise and asking for any feedback that can help all of us. Before I show the two simple charts, let me shed some light on the terminology for those who actually did something more social this weekend versus study bank financials.

Total Net Revenue is broken into two groups:

1 – Net Interest Income (interest income minus interest expense)

2 – Non Interest Income

Combing the two gives you total revenue. That revenue then needs to cover three main expenses:

1 - Non Interest Expense (staff, legal, pretty much all operating expenses)

2 - Provisions for credit losses

3 – Income to shareholders.

The first chart I show is Total Net Revenue minus Non Interest Expense (in other words income left to cover provisions for credit losses and income to shareholders) VS Provisions for Credit Losses. This one is simple and not good looking. Since Q1 2009 income available to service provisions has dropped dramatically and shown no recovery. At the same time provisions have also dropped. Sure there is some tweaking of provisions to prevent / minimize losses but the question that needs to be answered is will the red line (provisions for credit losses) be forced to trend up again. To answer this question, I then looked at total loans and leases on the balance sheet and allowance for credit losses (the amount reserved for future credit losses).

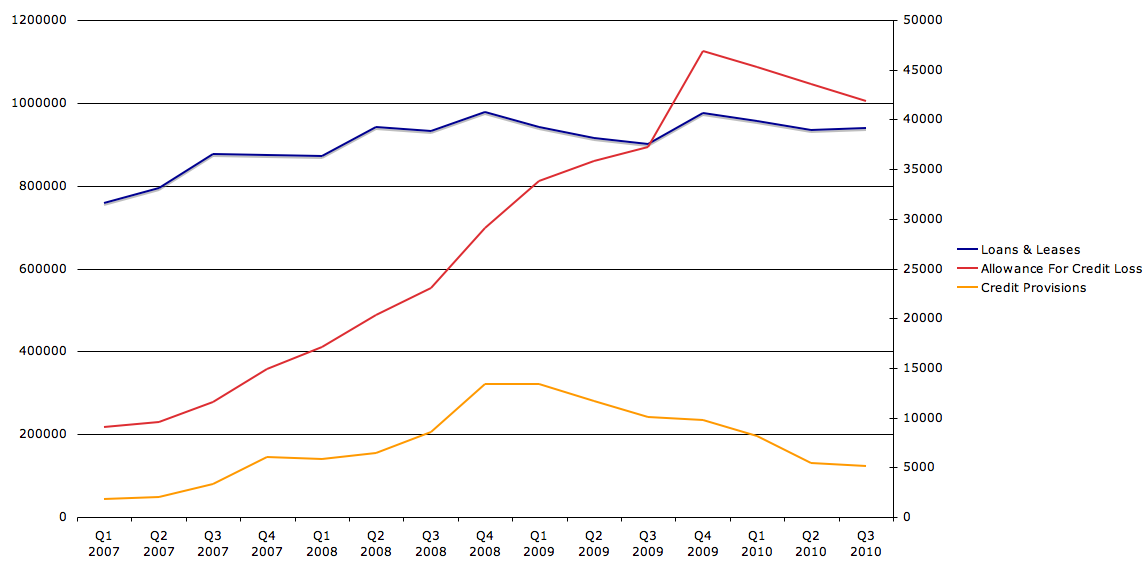

This chart shows Loans & Leases VS Allowance For Credit Losses VS Provisions for Credit Losses. Some observations, loans and leases for the most part have stayed flat and through Q4 2009 allowance for credit losses did move up rather significantly. Since that time they have begun moving back down. As of right now BAC has reserved for a 4.45% losses to total loans and leases. Assuming all loans and leases are held at par then in other words the balance sheet is priced at 95.55% of par.

The question I am struggling to understand is does this data alone and the realization that shadow inventory has grown the past year show that provisions (the orange line) will be forced to move up again regardless of the future of home prices. Provisions are made up of two components:

1 – Changes to allowance for credit losses (balance sheet adjustment)

2 – Actual loss incurred during a given quarter

Provisions have been moving down since Q4 2008, a year ahead of the move down in allowance for credit losses. In other words BAC through 2008 was realizing lower losses yet reserving at a higher rate. Why would you reserve for future losses unless you were all but certain of those losses. If anything you would reserve as little as possible in the face of diminishing earnings (chart 1 above).

Banks have reported a time line in excess of 14 months from default to REO so there is a lag time between the actual loss incurred and the balance sheet adjustment.

Submitted by Runedge. If you would like to visit my blog please go to - Ultra Trading